Global| Apr 29 2019

Global| Apr 29 2019EMU Indexes Show Deep and Broad Weakness: Is Winter Coming?

Summary

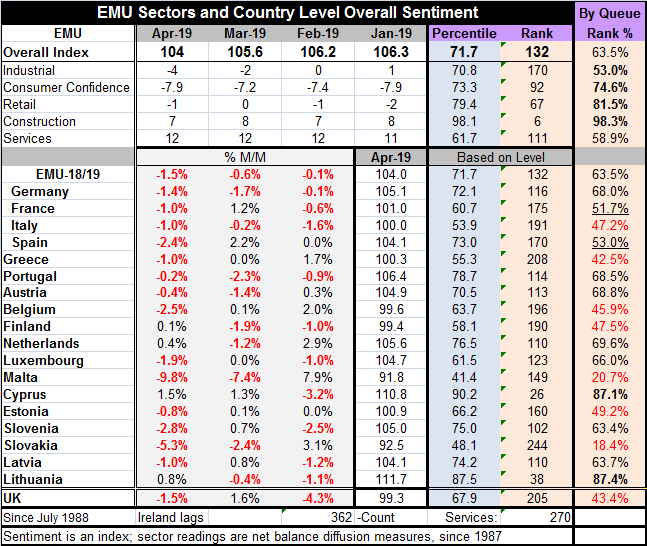

The EU Commission indexes fell relatively sharply in April, dropping 1.6 points month-to-month and shedding 7.3 point over 12 months. The 12-month drop is the largest of its kind since the index fell by 8.3 points in November 2012. [...]

The EU Commission indexes fell relatively sharply in April, dropping 1.6 points month-to-month and shedding 7.3 point over 12 months. The 12-month drop is the largest of its kind since the index fell by 8.3 points in November 2012. The EMU index began shedding value in January 2018. Over the past 15 months, the index has fallen monthly in 13 of those months. The largest monthly drop in this cycle came in December 2018 with a month-to-month drop of 2.1 points. This month’s 1.6 point drop is tied for the second largest monthly drop in this episode of weakness. On balance, there is no indication that the slowdown is losing any momentum as some other reports (like the ISMs) had suggested.

The EU Commission indexes fell relatively sharply in April, dropping 1.6 points month-to-month and shedding 7.3 point over 12 months. The 12-month drop is the largest of its kind since the index fell by 8.3 points in November 2012. The EMU index began shedding value in January 2018. Over the past 15 months, the index has fallen monthly in 13 of those months. The largest monthly drop in this cycle came in December 2018 with a month-to-month drop of 2.1 points. This month’s 1.6 point drop is tied for the second largest monthly drop in this episode of weakness. On balance, there is no indication that the slowdown is losing any momentum as some other reports (like the ISMs) had suggested.

Since the end of the great recession a period around April 2009, there have only been four occasions when there were fewer monthly declines among EMU members than there were this month. In April, only four countries show monthly increases in their EU sentiment readings; they are Finland, the Netherlands, Lithuania, and Cyprus. Of the 14 EMU countries showing monthly declines, only two have monthly declines less than 1%. Five have decline greater than 2%. Four have decline greater than 1% and less than 2%. The weakness is severe on top of being broad-based.

In addition the United Kingdom, still and EU member, shows a monthly drop of 1.5% in its index.

A great deal of weaknessSo how weak are these reporting countries? The overall EMU queue standing which included the breadth of all reporters weighted by their GDP importance shows a 63.5 percentile standing. On the percentile scale, the median result occurs at a 50% queue standing so these results are still ‘comfortably’ above their median but momentum is anything but comforting. Moreover, of the 18 reporting nations, seven have queue standings below the 50% mark putting them below their respective medians. Italy with a 47.2 percentile standing is the largest EMU country with a standing below its median. But France has a standing of just 51.7% and Spain is at 53.0%. There are no countries with standings in their 70th percentiles this month and the highest standing is from tiny Lithuania with a queue percentile of 87.4. Cyprus has an 87.1 percentile standing. There are eight members with standing in their respective 60th percentile decile (from 60% to 69.9%). There is not much real strength anywhere. Sectors show weakness but some show strength too

Evaluated by sectors, the euro area may seem a bit stronger. But that is only because there are no abjectly weak sectors and because a few small sectors score strong rankings. Still, the two most import sectors, manufacturing and services, each have queue percentile standings in their respective 50th percentile deciles- at relatively pedestrian levels. The small construction sector has a 98.3 percentile standing. Retailing, an important sector, has an 81.5 percentile standing and consumer confidence has just a 74.6 percentile standing. All sectors weakened on the month except services which remained locked at a 12 reading. Retail and construction are the two sectors with the lowest correlation with the overall EU Commission sentiment barometer, so their strength actually does not impact the overall barometer much.

On balance, we have to regard this as an exceptionally weak report and weak month of data. The headline drop is much weaker than expected and the details are about as far from reassuring as they can get.

By sector, only the industrial sector is weakening for three months in a row. But the EMU as a whole shows three declines in a row and so does its largest economy, Germany. Italy and Portugal also show three monthly declines in sentiment in a row. Every reporting country except for Estonia, Cyprus Greece and Spain has at least two declines in the last three months (Greece, Estonia and Spain each have a 0% mixed in with their ‘noncompliance’). The U.K. also has two declines in the last three months and has yet to sort out its Brexit endgame.

The money and credit story

The money and credit story

Separately, the ECB reported out monthly and credit growth. In March, money growth is accelerating and its growth rate has been stepping up from 12-month to six-month to three-month with its largest pop over three months. Nominal credit growth has been flat, however. In real terms, money supply continues to show acceleration while credit growth continues to look flat with 12-month growth at less than 1% real growth for credit to residents as well as for private credit. On the credit side, the economy continues to look very weak and not at all like it is making progress.

European stock markets are mixed but have generally moved higher in the wake of Spanish election in which socialists have taken a prominent position. Europe is getting anxious over the upcoming European EU elections and the prospects for France and Germany to see their influenced lessened as the Community is undergoing a severe change in values and has become resentful about what the way the elite have run things. There are more palpable concerns about the rising ratio of debt to GDP in Italy and the amount of Italian bonds held by Italian banks who apart from that do not have the strongest balance sheets. While the U.S. has spent the post-recession period repairing the position of its banks, Europe has not and even two of the largest German banks find themselves in weakened positions.

For these reasons, Europe is a less than healthy place to be. As today’s data show us, there is little in the way of monetary trends to like and even less in terms of economic growth indicators. Today’s EU Commission indicators are a prod with a sharp stick. Europe remains challenged and there is hardly hint that the worst is behind it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief