Global| Aug 29 2019

Global| Aug 29 2019EMU Indexes and Their Momentum

Summary

The persistent pressure of declining economic activity let up a bit in August as the EU Commission's economic sentiment reading for the EMU rose. The index rose to 103.1 from July's 102.7, a monthly gain that still leaves the August [...]

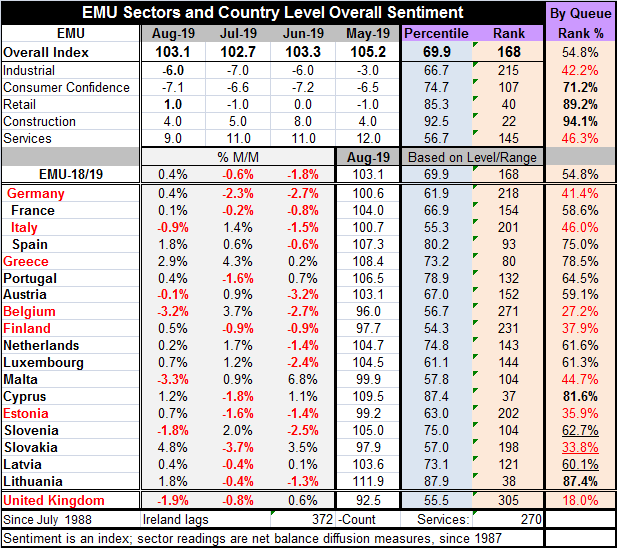

The persistent pressure of declining economic activity let up a bit in August as the EU Commission's economic sentiment reading for the EMU rose. The index rose to 103.1 from July's 102.7, a monthly gain that still leaves the August reading below its June level -a rise but an unimpressive one.

The persistent pressure of declining economic activity let up a bit in August as the EU Commission's economic sentiment reading for the EMU rose. The index rose to 103.1 from July's 102.7, a monthly gain that still leaves the August reading below its June level -a rise but an unimpressive one.

The August rebound is only the fourth month-to-month increase in the last 18 months. The EU commission's gauges show an economy in a protracted decline. Still, this month only five of 18 early reporting countries issued indexes showing monthly weakening, a big step down from the nine reporting declines last month. August showed more countries reporting gains month-to-month than in any other month since December 2017. Even though the slowing of the aggregate gauge month-to-month was moderate, the breadth of the gains and narrowing of the losses was marked and it breaks a trend or may mark a new phase.

If we look at three-month smoothed data, we can also make some historic comparisons with a bit more validity. The recessionary period in 2008 to early-2009 showed a greater breadth of countries with EU indexes declining month-to-month. There was a recovery then another slippage from 2011 to mid-2012. But the country declines in this episode that date from December 2017 show a greater breadth of decline on monthly data than anything except the period of the Great Recession itself.

Not only is there growth and ongoing decline in the national index falling (with the exception of this month), a great breadth in the country by country declines of the EU indexes (again, except for this month), but there is also a large collection of countries with below median country standings. This month seven of eighteen countries log below median level observations for their sentiment indexes and only two show rankings in their upper 20th percentile or better (the small countries of Lithuania and Cyprus).

By sector, the industrial sector and the services sector are both below their respective medians in August on data back to late-1988. The retail and construction sectors each have extremely high rankings in their respective 89th and 94th percentiles. Consumer confidence logs a more middling 71st percentile standing. None of these are weak enough to suggest recession, but the slippage is nonetheless clear. And yet there is also some real strength that has persisted in retail and in construction.

The graph offers another visual metric on the dynamics of the state of decline. 12-month changes show how the year-on-year increase reached a peaking speed in the second half of 2017 for the euro area and its largest four economies. Their sentiment gauges continued to rise but at a more or less continuously slowing pace though mid-2018. However, by the second half of 2018, all three countries and the EMU levels of confidence were declining at an accelerating pace. In early-2019, the pace of erosion stabilized for two of them plus the EMU. France fell more sharply than the rest of the pack from late-2017 through late-2018. Since then, France has been reducing its rate of decay but still showing declines on year-over-year comparisons. Germany, nevertheless, in the last two months, has stepped up its pace of decline. Italy ran at a pace close to the overall EU pace.

Evaluating these patterns, we see some clear evidence of slowing in the European unravel. But we also see some growing signs of weakness in the EMU region's premier economy, Germany. As such, the evidence on changing speeds is decidedly mixed. Market data continue to show negative developments. The whole area continues to demand close scrutiny of developments and trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief