Global| Nov 30 2017

Global| Nov 30 2017EMU HICP Rises in November But Core Inflation Remains Listless

Summary

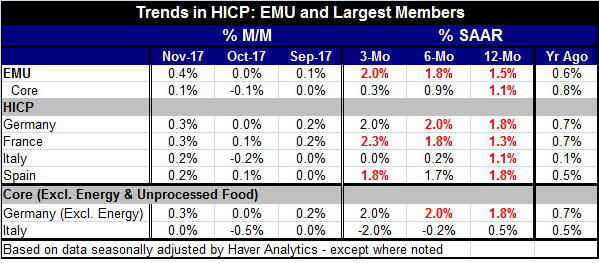

Conditions for greater conflict may be coming to a head as the overall EMU HICP gained 0.4% in November as Germany's own HICP rose by 0.3%. In the EMU, the HICP is only up by 1.5% over 12 months but the six-month (annualized) pace is [...]

Conditions for greater conflict may be coming to a head as the overall EMU HICP gained 0.4% in November as Germany's own HICP rose by 0.3%. In the EMU, the HICP is only up by 1.5% over 12 months but the six-month (annualized) pace is at 1.8% and the three-month pace is at 2%. For Germany, the 12-month pace is 1.8% while the six-month and three-month pace each are at 2%. So Germany itself is on the brink of 2% inflation with shorter horizon momentum already indicating a 2% rise, which would be a slight breach of ECB protocol were that the rate for the entire union. For the EMU, the year-on-year gain is still well short of 2% at 1.5%, but the shorter term momentum shows that a 2% pace is already prevailing.

Conditions for greater conflict may be coming to a head as the overall EMU HICP gained 0.4% in November as Germany's own HICP rose by 0.3%. In the EMU, the HICP is only up by 1.5% over 12 months but the six-month (annualized) pace is at 1.8% and the three-month pace is at 2%. For Germany, the 12-month pace is 1.8% while the six-month and three-month pace each are at 2%. So Germany itself is on the brink of 2% inflation with shorter horizon momentum already indicating a 2% rise, which would be a slight breach of ECB protocol were that the rate for the entire union. For the EMU, the year-on-year gain is still well short of 2% at 1.5%, but the shorter term momentum shows that a 2% pace is already prevailing.

Headline inflation makes its case

With an ECB mandate to keep inflation just below 2%, these metrics will make Germans and other inflation hawks uneasy at a time the ECB is still marking time on measured policy change.

Among the other three of the biggest four EMU economics, Spain has inflation rising by 1.8% over 12 months, France has it up by 1.3% over 12 months, and Italy has it up by 1.1% over 12 months. However, France also shows progressive acceleration for inflation while in Spain the 1.8% pace is consistent more or less over shorter horizons. Italy shows price deceleration with the price level actually flat over three months; the chart also shows its price weakness. We have another case brewing in which a one-size fits-all monetary policy will be too loose for some and too tight for others.

Inflation is not rotten to the core

However, setting aside these trends there is also the core HICP to asses and the ECB has been putting emphasis on this during this period when oil prices have been gyrating. The core rose by only 0.1% in November and is up at a weak 0.3% annualized rate over three months and at a 0.9% annualized rate over six months compared to a pace of 1.1% over 12 months. In short, the core rate is still decelerating- fully supporting a tactic to make few changes in monetary policy which remains accommodative.

Policy conflict and the German condition

The headline and core rates are giving conflicting signals and since the German economy actually is pushing the envelope on its growth we can see that for Germany at least the notion of price pressure is a real event. The presence of price pressure is supported by the German CPI ex-energy measure which is up by 1.8% over 12 months and at a pace of 2.0% over both three months and six months. Germany is on the razor's edge and if the Bundesbank were controlling interest rates they would not be so low now. But the ECB is headed by Mario Draghi and it is making policy for the entire euro area and on that basis what might be desired by Germans is not necessarily best for the whole of the euro area.

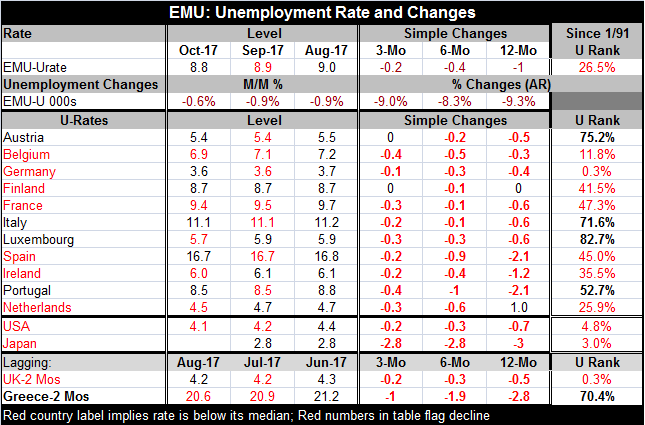

However, EMU growth is in gear: Unemployment trends in EMU New unemployment data show that among the original EMU members, five of the 11 saw a drop in the rate of unemployment in October. But 9 of 11 show drops over the last three months. And 11 of 11 show drops over six months and 10 of 11 show drops over 12 months. The momentum both longer terms and very near term shows that growth continues to be of such a magnitude that the unemployment rate is being reduced on a consistent basis -EVERYWHERE!

Among the 11 EMU countries in the table, however, four still have unemployment rates that remain stubborn and are above their respective median values since the EMU was formed. Austria, Italy, Luxembourg and Portugal have rates that reside above their medians since January 1991.

Germany is staring at an historic low rate of unemployment, the lowest in fact since German reunification as well as the lowest rate in all of the EMU in October. Belgium has a rate that has been lower less than 12% of the time. But after that, the next relative low rate is from the Netherlands where the rate has been lower less than one-quarter of the time. In Ireland, the rate has been lower about 35% of the time. Finland, France and Spain have unemployment rates that have been lower from 41% to 47% of the time. These are a far cry for overheating and for many EMU countries stopping an easy monetary policy now or reversing it would be like stopping your race car at the threshold of the finish-line. Germany really stands alone as the country that has made the most economic progress, has the lowest unemployment rate and may have little additional scope for inflation free growth. But that is Germany's situation and is not characteristic of the euro area. Germany is the odd-man out.

Germany's confrontations with more inflation pressure here is text book. But with the rest of the EMU so much farther back in terms of cyclical progress, it hardly seems like the right thing to do, to hike rates because Germany may encounter some inflation pressures. The ECB makes policy for all of the EMU.

Note that I have made this point by looking at each country's unemployment rate ranking, not at its level. The counter argument that is sometimes made is that other countries (countries other than Germany) have structurally high unemployment rates and they need to make structural economic changes rather than try to solve structural problems with cyclically inappropriate (too strong) growth. But this argument is not relevant here since we have made the point by comparing each country's actual rate of unemployment with its own history. I have used a relative standard to assess unemployment not an absolute one. And in relative terms, unemployment is still mostly high across the EMU.

On balance, the EMU has a policy dilemma on its hands. We can expect Mario Draghi to stay the course and to make adjustments for less stimulus and higher rates only gradually and only as EMU-wide conditions warrant. Germany's needs alone are not enough to move EMU policy or to prod it to shift faster.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief