Global| Feb 23 2021

Global| Feb 23 2021EMU HICP Makes First Year-on-Year Rise since July

Summary

The EMU headline rose by 0.8% in January, its first year-on-year gain in six months (July 2020). Inflation in the euro area is clearly accelerating with the 12-month pace at 0.8%, the six-month pace at 2% and the three-month pace up [...]

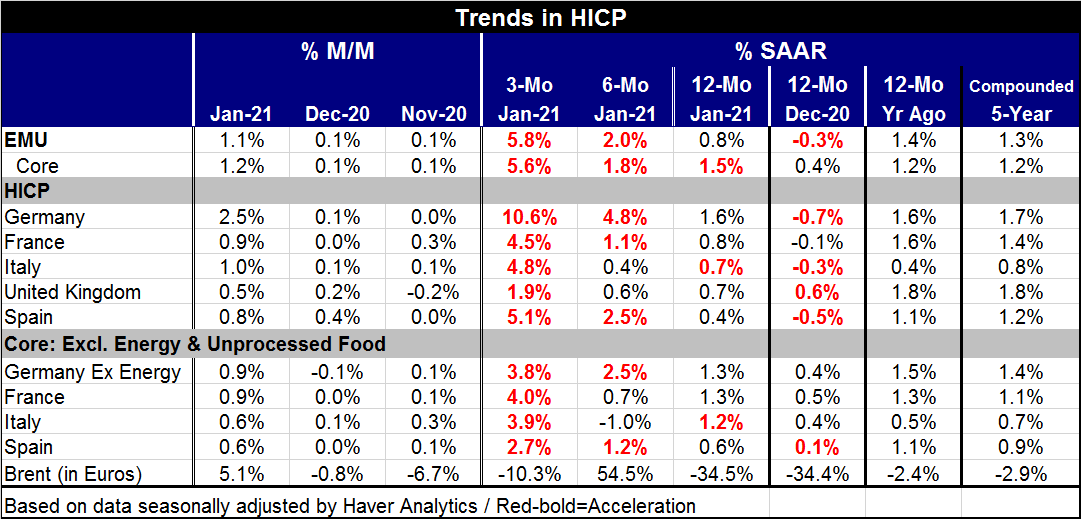

The EMU headline rose by 0.8% in January, its first year-on-year gain in six months (July 2020). Inflation in the euro area is clearly accelerating with the 12-month pace at 0.8%, the six-month pace at 2% and the three-month pace up to 5.8%. Similarly, the core measures show the same sequential acceleration, rising to a three-month (annualized) pace of 5.6%. These trends are echoed across the largest EMU (and U.K.) economies in the table. However, both the U.K. and Italy fail to show acceleration over six months compared to 12 months. And over three months, the U.K. inflation rate is only 1.9%. But elsewhere three-month inflation is more like 5.5% to 5% except for Germany where the three-month pace has hit double digits (!) at 10.6%.

The EMU headline rose by 0.8% in January, its first year-on-year gain in six months (July 2020). Inflation in the euro area is clearly accelerating with the 12-month pace at 0.8%, the six-month pace at 2% and the three-month pace up to 5.8%. Similarly, the core measures show the same sequential acceleration, rising to a three-month (annualized) pace of 5.6%. These trends are echoed across the largest EMU (and U.K.) economies in the table. However, both the U.K. and Italy fail to show acceleration over six months compared to 12 months. And over three months, the U.K. inflation rate is only 1.9%. But elsewhere three-month inflation is more like 5.5% to 5% except for Germany where the three-month pace has hit double digits (!) at 10.6%.

Core or ex-energy inflation also shows acceleration. This starts at the aggregate level where inflation’s pace rises from 1.5% over 12 months to 1.8% over six months to 5.6% over three months. Countries also show this acceleration with the exception that France and Italy show inflation breaking lower over six months compared to twelve months. Over three months, core (or ex-energy) inflation rates all rise compared to their six-month counterparts by country. The three-month pace ranges from a high at 4.0% in France to a low of 2.7% in Spain. Germany that has such a strong headline acceleration over three months has a three-month core pace of 3.8%.

Brent oil prices surge by 5.1% in January although over three months Brent prices are net lower falling at a 10.3% annual rate. Oil prices are up at a 54.5% rate over six months but still lower by 34.5% over 12 months.

Inflation is flaring. But some of this is because of supply chain disruptions and some of it is because of other sorts of strains placed on the various economies because of the Covid-19 responses. It is not because of classical economic over-heating or a labor shortage. We are talking about adjustment issues to this regime in which production has not yet been able to find a new or comfortable normal. But that adjustment is still in progress and will improve as we make more progress against the virus.

Inflation is finally getting back toward target; it is this month near the 1% mark, still well short of its goal but at least ‘moving in the right direction’ (compare 0.8% to an ECB target of just less than 2%). Over shorter horizons, the annualized inflation rate is flaring well beyond levels that the ECB would find tolerable. Yet, it is not clear that any of those excessive growth rates in prices are true harbingers of coming inflation (where we view inflation as an ongoing phenomenon- not a one-time spike in the price level). In any event, the EMU economy is so weak and impacted that even if inflation were to rise to or above 2% it would be hard for the central bank to take any action despite the fact that it is a one-pillar monetary policy central bank. The only true ECB mandate is to contain inflation; yet, with the virus circulating undermining growth and distorting all sorts of activity and prices, it is a hard time to operate as though times are normal. Times are not normal and the risks are asymmetric. With inflation flaring for the first time in nine years and with a substantial legacy of undershooting and very unusual times at hand, policymaking will become increasingly challenged to make the right decision, especially in Europe.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief