Global| Sep 16 2015

Global| Sep 16 2015EMU HICP Flirts with Danger Again

Summary

Mario Draghi warned that the EMU could face another period in which its inflation gauge, the HICP, declined. In August the monthly HICP fell by 0.1%, its second drop in three months. Now the year-over-year HICP gain is just 0.1%. The [...]

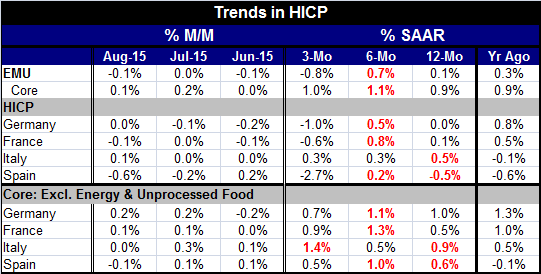

Mario Draghi warned that the EMU could face another period in which its inflation gauge, the HICP, declined. In August the monthly HICP fell by 0.1%, its second drop in three months. Now the year-over-year HICP gain is just 0.1%. The sequence of changes in the core HICP shows inflation at 0.9% over 12 months, at a pace of 1.1% over six months and at 1% over three months. The core remains relatively stable around the 1% mark. But headline inflation is losing its grip.

Mario Draghi warned that the EMU could face another period in which its inflation gauge, the HICP, declined. In August the monthly HICP fell by 0.1%, its second drop in three months. Now the year-over-year HICP gain is just 0.1%. The sequence of changes in the core HICP shows inflation at 0.9% over 12 months, at a pace of 1.1% over six months and at 1% over three months. The core remains relatively stable around the 1% mark. But headline inflation is losing its grip.

In August the big four EMU economies show a lot of price weakness. Prices fell in France and Spain; in Germany prices were flat. In Italy prices rose by 0.1%.

Over three months, Germany, France and Spain show declining prices. Spain's prices are falling at a 2.7% pace over three months. Year-over-year Spain's price level is falling while Germany's is flat. France's prices are up by just 0.1% while Italy's are up by 0.5% over 12 months. Deflation is a razor's edge away.

Core inflation shows weakness and stability everywhere except in Italy where over three months prices are up at a 1.4% annual rate. On balance, the EMU seems to be under a lot of downward price pressure.

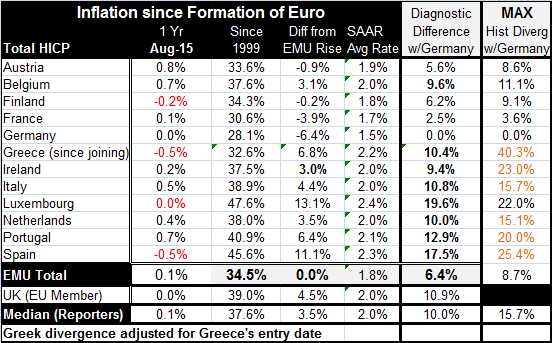

The table below allows competitiveness comparisons among the earliest euro area countries. The EMU total shows that since the formation of euro, EMU prices have risen at a pace of 1.8%, right in line with the ECB mandate of just under 2%. In Germany prices have averaged rising by 1.5%, the lowest gain in the region extending German competitiveness. The far hand column shows the maximum competiveness any country has lost vis-a-vis Germany since the EMU was formed. The second to the right columns show where each country stands vis-a-vis the German price level today.

We see that all of Greece's duress has paid dividends. Once a country that had lost 40% of its competitiveness to Germany since it joined the EMU, it now lags German competitiveness by only 10.4% placing in the middle of the EMU. Competitiveness simply looks at the difference in the percentage rise in the German HICP vs. the Greek HICP since Greece joined the EMU.

Ireland also has made substantial progress. It had lagged Germany by 23 percentage points and now it has whittled that down to a 9.4 percentage-point gap. Italy and the Netherlands each have made sizeable gains moving their competiveness vis-a-vis Germany up by about 5 percentage points. Portugal which once lagged Germany by 20 percentage points is down to lagging it by only 12.9 percentage points. Spain, which had a huge disadvantage vs. Germany, of as much as 25.4 percentage points, has made some progress but not enough. It still lags Germany by over 17 percentage points.

What we see is that austerity has not been for austerity's sake. It has resulted in slowing inflation in high inflation countries and moreover slowing it to a pace below Germany's pace so that actual competiveness gains were made. The EMU now has three tiers; Austria Finland and France trail German competiveness by small amounts. The next group of EMU members trails Germany by about 10 percentage points. Then there is Spain which still trails Germany by 17 percentage points.

On balance, inflation is still low and low enough to be disruptive in the EMU. With German inflation so low again, it will be hard for other countries to continue to make any competiveness gains on Germany's significant lead. Moreover, the macroeconomic implications are that Europe will continue to struggle. Its low inflation will probably improve its competitiveness for the euro area globally, but prices are also weak around the world so don't expect much there. Still, the economic weakness will keep rate hikes at bay whereas the Federal Reserve seems to be on the verge of a rate hike in the U.S. This will keep the dollar firm and the euro weak. Still, it has been like that for some time with EMU growth seeming to benefit very little from its improved competitiveness. Of course, Germany has done well and carries a massive current account surplus.

The OECD has cut its outlook for growth in the OECD area. We await Greek elections this weekend. Europe will continue to struggle with its migrant influx. Meanwhile, China is still a jumble and the Bank of Japan has downgraded its economy. It's still a tough environment to try to get growth going. That is one of the messages from this brand of low inflation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.