Global| Apr 30 2020

Global| Apr 30 2020EMU GDP Takes a Deep Dive; Everyone Holds Their Breath

Summary

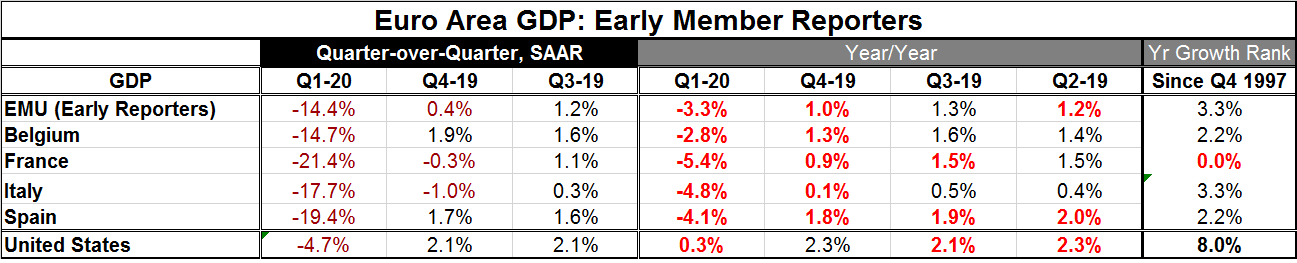

Europe was hit especially hard in Q1. The year-on-year growth rates for this cluster of reporters is at or near the lowest they have posted since end-1997. European economies generally were hit a bit earlier than the U.S. That is [...]

Europe was hit especially hard in Q1. The year-on-year growth rates for this cluster of reporters is at or near the lowest they have posted since end-1997.

Europe was hit especially hard in Q1. The year-on-year growth rates for this cluster of reporters is at or near the lowest they have posted since end-1997.

European economies generally were hit a bit earlier than the U.S. That is shown by the larger GDP declines they are posting in Q1.

However, this can be taken as a message today and the message is that is that EVERYONE is getting hit by this and that could serve to redouble the doubts about what growth can look like in the period ahead. The 'V' is out; the 'U' is in; the 'W' is lurking in the wings. All economies sank more or less together and all will recovery more or less together. But the economies will all have different sorts of wounds to deal with in recovery. And while the initial back-to-work recovery phase might look strong, it will run its course then devolve into a period of a much slower and more difficult slog upward. The U.S. trading day is showing stock market difficulties to add to the weakness seen in Europe. Are markets tiring of repeated positive reactions to developments concerning the virus?

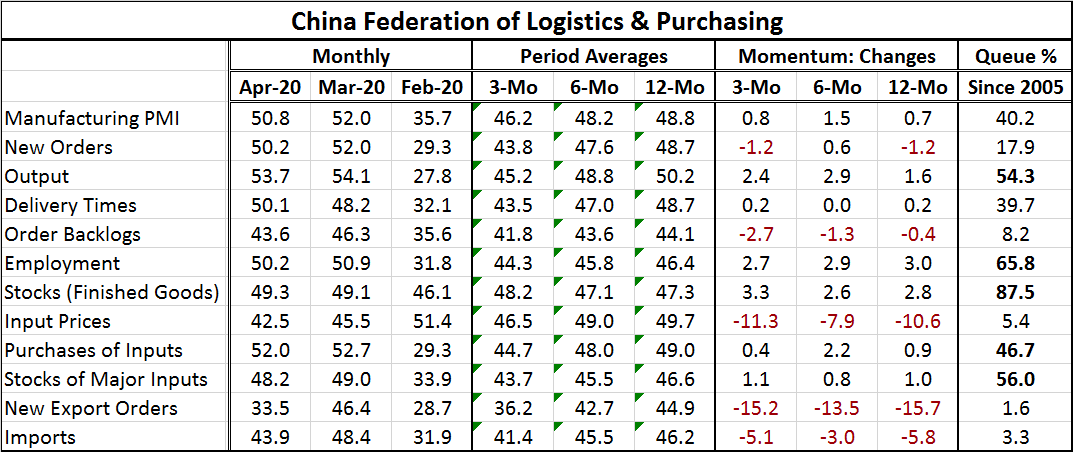

Stocks in Asia did not fare so badly partly because the Chinese PMI from the China Federation of Logistics & Purchasing (CFLP) fell to 50.8 in April from 52.0 in March, retaining a semblance of growth. China is weathering the storm relatively well and it is much farther along the recovery curve. Still, it is not clear that China is a barometer for the Western nations since the business rules of engagement are so different in China and there are lingering suspicions about what really happened in China to begin with. Other Asian data were generally much weaker than China's data today. Japan reported a plunge in its LEI, a new low for consumer confidence, the ninth month-to-month drop in housing starts and a decline in retail sales as well as a fall in industrial production. Asia is not out of the woods even if China thinks it is.

China is showing resilience, but no one is certain what that means or how long it lasts. Donald Trump is turning up pressure on China blaming its virus response saying that China does not want him to get reelected. So maybe his good friend Xi is not such a good friend anymore? We will want to watch to see if U.S.-Chinese relations are going to deteriorate in the wake of these comments.

The global, geopolitical, economic and pandemic plots are thickening. There are too many balls in the air to juggle them all effectively. Recessions are clicking into gear and central banks and governments are doing what they can to soften the blow from the virus and their response to it.

People everywhere are fed up with the lockdown as the lockdowns are starting to be lifted in various places. Many countries are planning or taking steps to normalize. In the U.S., steps are being taken in different states at different speeds.

It's 'risk on' for wave two. Will there be s second wave of infections? Or will there be enough 'herd immunity' in time to head it off? Meanwhile, stock markets are making surprisingly steady/strong recoveries. But have they gotten to the point where there is more risk there too? As global equity indexes rise, the actual evolution of recovery becomes more important to future valuations. The easy over-sold stock market rebound is all but over. The next phase for the stock market seems to be more demanding and possibly more treacherous.

Do investors have a solid hold on the timing, the speed and the extent of recovery? Probably not, but we will see. Do they have a good fix on the path of corporate earnings to benchmark valuations or are stocks still trading the coronavirus news day by day? At some point, stocks will have to benchmark value to some hard economic data. Stocks can recover from their crater for only so long before they need to get a firmer fix on the recovery path and destination. We seem to be getting closer to the time when those considerations are real. With some sign today that markets are reacting to the economic data, maybe equities are beginning to show their own vulnerabilities as well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief