Global| Mar 04 2010

Global| Mar 04 2010EMU GDP Stays Put – No Revision

Summary

EMU GDP rose by 0.5% Saar in 2009-Q4. Private consumption in the Zone fell at a -0.1% annual rate. Meanwhile exports and imports surged at growth rates of 6% and 7%, respectively. Public consumption also fell in Q4 at a -0.5% annual [...]

EMU GDP rose by 0.5% Saar in 2009-Q4. Private consumption in the Zone fell at a -0.1% annual rate. Meanwhile exports and imports surged at growth rates of 6% and 7%, respectively. Public consumption also fell in Q4 at a -0.5% annual rate. Capital formation after rising in Q3 retracted again in Q4. Domestic demand was a weak -0.8%.

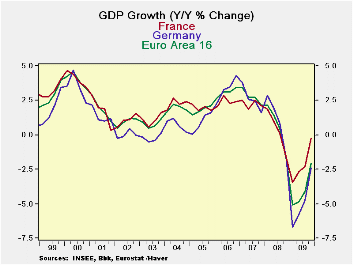

France is closing in on positive GDP growth and is closer than either Germany or EMU as of Q4. But Germany with a much deeper hole that its GDP fell into is rising faster from its extreme depths.

Portugal’s numbers still aren’t in for Q4. But among those countries we list in the table that have reported, Greece, Italy and Spain are the only ones with falling GDP in Q4. These are the countries with debt problems of various sorts in EMU. It is interesting that the indebtedness seems to hold them back from recovery at the same pace as fellow EU/EMU members.

| EMU GDP | |||||||

|---|---|---|---|---|---|---|---|

| Consumption | Capital Formation | Domestic Demand |

|||||

| GDP | Private | Public | Total | Exports | Imports | ||

| % Change Q/Q (saar) ; X-M is Q/Q change in Blns of euros | |||||||

| Q4-09 | 0.5% | -0.1% | -0.5% | -3.1% | 6.2 | 7.0% | -0.8% |

| Q3-09 | 1.7% | -0.7% | 3.1% | 7.1% | 0.7 | 11.9% | 1.6% |

| Q2-09 | -0.5% | 0.3% | 2.4% | -17.7% | 13.1 | -4.5% | -3.1% |

| Q1-09 | -9.6% | -1.9% | 2.2% | -33.1% | -6.2 | -29.3% | -8.7% |

| % Change Yr/Yr; X-M is Yr/Yr change in Gap in Blns of euros | |||||||

| Q4-09 | -2.1% | -0.6% | 1.8% | -13.1% | 13.8 | -5.2% | -2.8% |

| Q3-09 | -4.1% | -1.1% | 2.5% | -14.9% | -15.1 | -13.5% | -3.5% |

| Q2-09 | -4.9% | -1.0% | 2.2% | -16.2% | -27.1 | -17.0% | -3.7% |

| Q1-09 | -5.1% | -1.4% | 2.4% | -14.1% | -34.5 | -16.4% | -3.5% |

| 5-Yrs | 0.7% | 0.8% | 2.1% | -1.0% | 0.5 | 1.4% | 0.7% |

As of Q4 only Greece is seeing its Yr/Yr GDP growth continue to slip at a faster pace than in earlier quarters. The UK has a larger Yr/Yr drop in Q4 but it has improved its Yr/Yr growth rate from -5.3% in Q3 to -3.3% in Q4. Only the US has a positive Yr/Yr rate of growth in Q4; Switzerland is at zero.

The quarterly growth rates are already turning positive and have been doing so for two quarters in a row in most countries. Clearly recovery is afoot. But we are reminded that domestic demand is lagging in the Zone and that it is a sector that is very important to recovery. Every nation cannot recover with export-led growth; that defies the rules of GDP and balance of payments accounting. At some point the recovery has to become home-grown. With the US economy looking like its recovery may not shift into overdrive it is even more important than ever for each country to elevate its own domestic demand.

| Euro-Area Retail Sales | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Jan-10 | Dec-09 | Nov-09 | 3-Mo | 6-MO | 12-Mo | |

| Zone Total Value | 0.2% | 0.2% | 0.2% | 2.4% | 1.1% | -1.1% |

| Food,Bev Tobacco | -0.1% | -0.1% | -0.2% | -1.8% | -2.1% | -2.1% |

| Registrations: | ||||||

| Motor Vehicle Reg | -0.4% | -3.1% | 1.1% | -9.4% | -0.8% | 20.8% |

| NonFood Country detail: Volume | ||||||

| Germany Value | 0.0% | 0.9% | -1.2% | -1.2% | -0.6% | -0.2% |

| UK(EU) Volume | -1.8% | -0.3% | -0.4% | -9.3% | -3.4% | 0.8% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief