Global| Nov 14 2013

Global| Nov 14 2013EMU GDP Is Advancing, but Not for All Members

Summary

I know it is cynical to write about the second quarterly EMU GDP rise after six consecutive quarters of declines and to feature a chart of the growth of some of the weakest EMU members. After seeing GDP broke out of its declining ways [...]

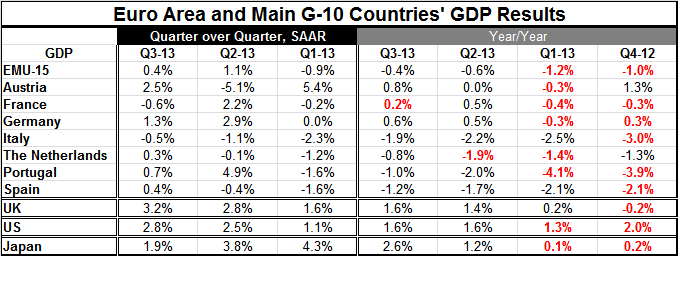

I know it is cynical to write about the second quarterly EMU GDP rise after six consecutive quarters of declines and to feature a chart of the growth of some of the weakest EMU members. After seeing GDP broke out of its declining ways one quarter ago, EMU still does not seem to have reached true escape velocity. With a 1.1% quarterly compounded GDP increase followed by a 0.4% quarterly compounded annual rate, euro GDP growth is not looking like a juggernaut. The forces that are pulling EMU GDP growth back toward recession are represented by the still very weak conditions of many of the EMU members - in addition to less than sustainable conditions in some of the countries that now are making progress. France, for example, grew by 0.5% year-over-year in Q2 but grew only by 0.2% on that same basis in Q3.

I know it is cynical to write about the second quarterly EMU GDP rise after six consecutive quarters of declines and to feature a chart of the growth of some of the weakest EMU members. After seeing GDP broke out of its declining ways one quarter ago, EMU still does not seem to have reached true escape velocity. With a 1.1% quarterly compounded GDP increase followed by a 0.4% quarterly compounded annual rate, euro GDP growth is not looking like a juggernaut. The forces that are pulling EMU GDP growth back toward recession are represented by the still very weak conditions of many of the EMU members - in addition to less than sustainable conditions in some of the countries that now are making progress. France, for example, grew by 0.5% year-over-year in Q2 but grew only by 0.2% on that same basis in Q3.

Portugal, Germany and France each showed weaker quarter-over-quarter GDP in Q3 compared to Q2. The euro-economy is not doling out growth in increasing dollops across all EMU members. The growth is weak and the progress in the Community itself is very uneven. Austria leads all growth rates in the table 2.5% (SAAR). Juggernaut-Germany's growth in the quarter is only 1.3% (SAAR).

This is less a time for EMU to rest on its laurels and to celebrate the crisis it has left behind than it is a time to redouble efforts to make sure that the euro area stays on the upside of growth.

Five of the seven countries whose growth rates we present in the table still have GDP declining year-over-year. That is not much to build upon. The good news is in the table showing the weaker EMU members. While their GDPs are still declining year-over-year, they are making progress in chopping down the size of those negative rates of growth. Portugal has been making a strong push. Greece is also making fairly rapid progress but from a very weak position. Italy and Spain are making solid progress in reducing their negative rates of growth.

There is progress in the euro-Community. And this is what it must keep in motion. It is as critically important to keep Spain, Italy, Portugal, and Greece growing as it is to keep Germany growing as well as France. The Community's hard times have brought home some truths that its members now need to address. This currency bloc is no land of milk and honey. It can, however, provide a region in which its members can prosper. But to do so it needs rules and principles that will benefit all members. The age of opportunism must be a thing of the past. Are these nations really ready to be Europeans? Actually we know the answer to that question: it is no. `The country' is still the principle unit of the eurozone. To become successful the eurozone will have to increasingly make polices that blur national borders. Harmonization will need to be about making as many aspects of the economy as possible similar across country lines, not just about reporting data on a uniform basis.

In its first round (pre-crisis), EMU showed what happens if each member stretched the rules to get the one thing it wanted from membership. Germany got a market in which its production was king. The Mediterranean countries got the low interest rates that allowed them to over borrow. The European Central Bank and EU Commission ignored the impact of persistent inflation differentials. No one worried about cross-border banking.

As Europe tries to pay attention to these known flaws, it will look to establish a set of rules that will be more common and less exploitable. Perhaps the EMU members will at some point recognize that they are all in the same area and that commerce is about mutually beneficial trade. The first test of this will be how the European Commission will deal with Germany and its excessive current account surpluses.

The fallacy of the Economic Community was that each country joined and then did not do much to change its ways to fit into the Community. Germany continued with export-led growth. The countries of southern Europe continued to run deficits and to finance them at low rates of interest. Without a fiscal transfer rule such things are not sustainable. Europe may not want to finance such persisting imbalances. But it does need to decide what it will do and won't do. So far we have groups of countries with different ideas about what the rules are. Such schisms can't last or be productive. Europe still needs to figure out what it wants to be as it grows up. And now the clock is ticking.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief