Global| Apr 30 2021

Global| Apr 30 2021EMU GDP Falls in Q1 2021

Summary

Despite some better performance on indicators such as the recent (and slightly timelier) EU Commission indexes, GDP across the euro area remains challenged, falling in Q1 2021. Because the EU Commission was not able to secure enough [...]

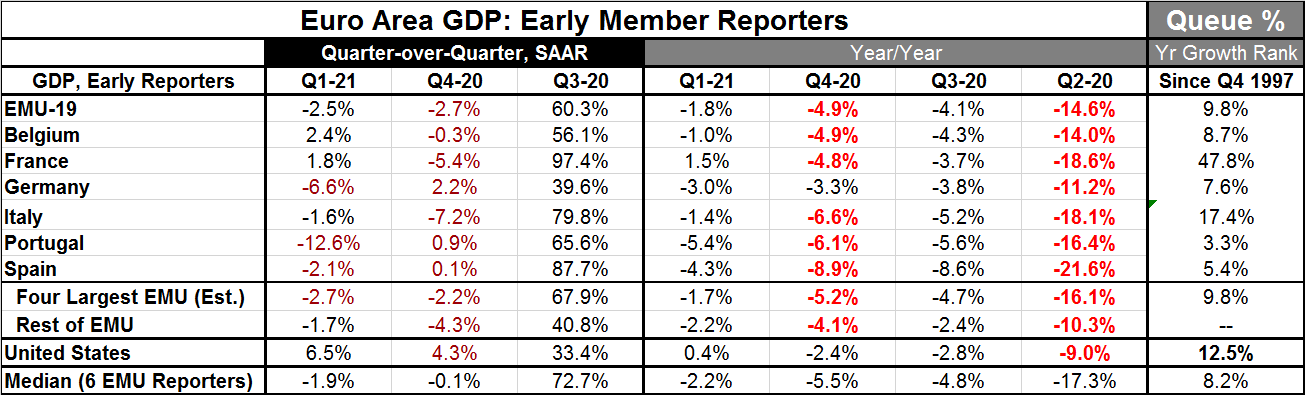

Despite some better performance on indicators such as the recent (and slightly timelier) EU Commission indexes, GDP across the euro area remains challenged, falling in Q1 2021. Because the EU Commission was not able to secure enough vaccine, the euro area has lagged behind the U.S. and U.K. efforts to vaccinate their respective populations. In Europe, a variety of outbreaks of the virus have continued to interrupt activity. And this shows in GDP results.

Despite some better performance on indicators such as the recent (and slightly timelier) EU Commission indexes, GDP across the euro area remains challenged, falling in Q1 2021. Because the EU Commission was not able to secure enough vaccine, the euro area has lagged behind the U.S. and U.K. efforts to vaccinate their respective populations. In Europe, a variety of outbreaks of the virus have continued to interrupt activity. And this shows in GDP results.

Quarterly growth rates assessed

In Q1 2021, the U.S. posted a large, 6.5%, (annualized rate) gain in GDP on the back of an improving vaccination effort and overlapping programs of mega-stimulus. In sharp contrast, EMU GDP is falling at a 2.5% annual rate in Q1. GDP in the four largest EMU economics (Germany, France, Italy, and Spain), when summed and growth calculated, finds aggregate demand falling at a 2.7% annualized rate. In the rest of the EMU, GDP growth is also easing but at a slightly softer -1.7% annual rate. Among the six early individual countries in the EMU reporting GDP, only Belgium and France have GDP gains in Q1. Germany in the quarter posted a GDP drop that is slightly faster than the U.S. Q1 GDP spurt. Portugal’s Q1 drop is at slightly better than twice the pace of the decline logged by Germany.

Clearly Europe has been facing challenges differently that the U.S.

Year-on-year growth

Year-on-year results shows EMU growth is falling by 1.8% in the first quarter. Of the six separately reporting countries, only France logs a year-on-year gain (+1.5%). The four largest EMU economics pooled together show GDP falling at a 1.7% annual rate in Q1 while the rest of the EMU logs a negative growth rate that is slightly worse at -2.2%. By comparison, U.S. GDP is up by 0.4% over four quarters after logging a knock-out strong growth rate in Q1 and with yet more stimulus in the pipeline.

How growth rates rank

The far-right hand column of the table ranks growth rates of GDP on a year-over-year basis against their historic record. The EMU pace is among the lowest 10% logged on the timeline back to Q4 1997. The U.S., despite its strong quarter, still reports a weak year-on-year result that is not far behind with its weak growth rate ranked among its lowest 12.5%. France alone logs a ‘respectable’ ranking at its 47.8 percentile. France’s 1.5% four-quarter growth rate lies just below its median pace for the period (the median occurs at a ranking of 50%). Apart from France and Italy, all individual EMU reporters plus the EMU as a whole have GDP lying in the lower 10th percentile of their historic queues of four-quarter growth rates.

The EMU area and most reporting members still see GDP declining year-over-year in Q1 2021.

The outlook

Looking to the future, it is still hard to make assessments. The recent EU Commission indicators (just reported yesterday) are coming out of the gate strong early in Q2. That is a hopeful signal. However, the virus is still an issue in Europe and Europe generally is less protected by vaccine. That makes pinning-down the outlook a slightly shakier proposition despite the strong start for Q1 2021. So far, the results on paper look good, but just when you think the results on paper are going to wrap up the virus, it morphs into scissors and cuts the paper progress to shreds. In truth, there is hoping, but there is no telling.

The virus is still going viral

The virus is doing unspeakable damage in India. Japan is still trying to contain it to launch the once-delayed Olympic games. We know what damage the virus is able to create. And we can see the progress that can be made - and is being made- in Israel, the U.S. and in the U.K. under the umbrella of a widening protection by inoculation. But Europe is not under that umbrella of protection yet. And there is still some debate about what it takes for that protection to really work. That concerns a concept called ‘herd immunity’ which has become a hot button issue to define.

Bellwethers vs. stand-alones

The U.S. is going to be a special case, not a bellwether, because no other country has dared to launch so much stimulus in so short a period of time. There is so much stimulus in train in the U.S. and plans for substantial layers of addition government spending of various sorts that markets are having pause and there are serious considerations about whether there is too much stimulus afoot or not. No other place in the world is under such scrutiny. However, there is optimism in Europe that an important corner has been turned and that growth, employment and progress can and will continue to mount at an accelerated pace. The EU Commission is still very concerned about its access to vaccine and it is trying to procure more even having taken steps to sue a vaccine maker for breach of contract. It is unclear how that effort will resolve itself. But that act is an indication that the EU is seriously pursing all options to get its vaccine program in gear to reap the benefits.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief