Global| Aug 14 2014

Global| Aug 14 2014EMU GDP Edges Higher

Summary

GDP growth in the European Monetary Union (seasonally adjusted and working day adjusted) barely edged higher in Q2 2014, rising by 0.2%. The year-over-year figures show a deceleration in the growth rate to 0.7% in Q2 2014 from 0.9% in [...]

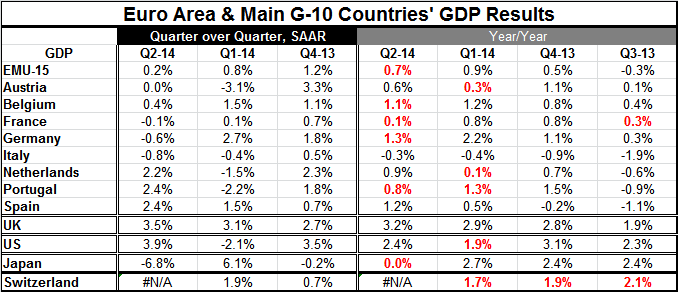

GDP growth in the European Monetary Union (seasonally adjusted and working day adjusted) barely edged higher in Q2 2014, rising by 0.2%. The year-over-year figures show a deceleration in the growth rate to 0.7% in Q2 2014 from 0.9% in the previous quarter. The EMU year-over-year GDP was last negative in Q3 2013.

GDP growth in the European Monetary Union (seasonally adjusted and working day adjusted) barely edged higher in Q2 2014, rising by 0.2%. The year-over-year figures show a deceleration in the growth rate to 0.7% in Q2 2014 from 0.9% in the previous quarter. The EMU year-over-year GDP was last negative in Q3 2013.

The three largest countries in the EMU posted quarter-to-quarter declines in GDP in Q2 2014. Germany's GDP fell by 0.6%, Italy's fell by 0.8% and France's fell by 0.1%. Year-over-year growth in Germany was cut to 1.3% in Q2, a deceleration from 2.2% in the previous quarter. France's year-over-year growth rate dropped to a very thin gain of 0.1%, a sharp deceleration from the 0.8% rate in the first quarter. Italy has consecutive quarters of GDP declines while its year-over-year rate at -0.3% is slightly better than the -0.4% pace in the first quarter. But Italy's economy continues to contract. The slightly smaller year-over-year decline doesn't seem to be the real story for Italy.

We have eight of the original EMU members as early reporters of GDP in the second quarter. We have year-over-year decelerations reported by half of them. Those countries with decelerating GDP in the second quarter are Belgium, France, Germany, and Portugal. Countries with accelerating GDP are Austria, Italy, the Netherlands and Spain.

The U.K., an EU member but not an EMU member, posted a 3.5% gain in GDP in the second quarter compared to 3.1% in the first quarter, marking a quarter-to-quarter acceleration. Its year-over-year GDP also accelerated to 3.2% from 2.9%.

The U.K. has the strongest year-over-year GDP of any reporting countries in the table. The U.S. has the second strongest at 2.4%. The strongest year-over-year growth rate in the EMU comes in Germany at 1.3%, followed by Spain at 1.2% and Belgium at 1.1%.

The weak growth in the EMU is a matter concern partly because the sanctions from Russia are only beginning to have an effect on that economy. Today, in addition to the release of these preliminary GDP numbers, the inflation metric for the EMU, the HICP, showed to the lowest inflation rate in the euro area since 2009.

The German GDP report listed weak exports as one of the drains on GDP growth as imports grew at a faster rate than exports in the second quarter. Capital formation was a drain as well with construction activity coming in below the first quarter level. Germany's Federal Ministry for Economic Affairs and Energy had previously pointed out that uncertainties in Ukraine and the Middle East would negatively impact German economic growth in the second quarter. This underlines the notion that there's more braking in growth to come in the third quarter from events that are already in the pipeline, let alone any new events that might emerge.

France reacted to its poor GDP showing by disassociating itself from its debt targets for this year, putting it at odds with the agreement it had with the European Economic Commission. It's unclear what the Commission's reaction is going to be. In the early stages of the Monetary Union, it's widely believed that absolving France and Germany from strictures stemming from budgetary constraints that they missed led to a loss of control over other EMU members. For the budget and debt-to-GDP rules to make sense, they must bind for everybody. However, hopefully the European Commission learned that imposing tight constraints when economic growth is weak is counter-productive and leads to further missing of targets. France's unilateral action puts the European Commission at the tough spot.

Weakness in the EMU is widespread and generally these conditions are weaker than had been expected. However, conditions are only slightly weaker than expected and the biggest fallout from the shortfall in growth seems to be France's recalcitrance concerning its budget target. Its decision to jettison the target rather than to try to negotiate a change places the entire union in a difficult spot.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief