Global| Dec 04 2008

Global| Dec 04 2008EMU GDP Confirmed At -0.8% (Saar) In 2008-Q4

Summary

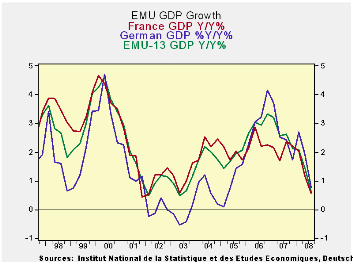

The details of EMU GDP show that the downfall to growth in the e-zone has been trade. GDP is falling at a 0.8% annual rate in Q3 as the trade gap widened by 10bln in Q3. Moreover, indicators for Q4 are still pointing to further [...]

The details of EMU GDP show that the downfall to growth in the e-zone has been trade. GDP is falling at a 0.8% annual rate in Q3 as the trade gap widened by €10bln in Q3. Moreover, indicators for Q4 are still pointing to further weakening. Private consumption is erratic but the Yr/Yr growth rates show it has slowed to a standstill. Public consumption continues to grow at a nearly 2.5% pace. Spending on capital formation has steadily decelerated and now runs at a Yr/Yr pace of less than 1%, just like GDP. Export and import growth both have moderated. But import growth is a bit faster than export growth, spurting in Q3, leading to an expansion in the trade deficit and a reduction in GDP growth.

The problem that confronts EMU is that domestic demand is faltering with its Yr/Yr rate of growth at 0.6% compared to 2.1% at the end of 2007. At the same time international sources of growth are tailing as exports are up at a 2.4% pace Yr/Yr compared to a five year average rate of growth of 5.9%. EMU is being pinched between weak domestic and weak foreign demand. The ECB, Bank of England and Bank of Sweden rate cuts will help to stimulate Europe in general. But the global slowdown is in gear and it will run its course. The ECB rate cuts and the slightly weaker Euro will help to cushion the blow. But both interest rates and foreign exchange rates take some time to have an impact. Moreover, with world demand low, no country is going to do very well with its export growth regardless of currency levels.

| Consumption | Capital | Trade Domestic | ||||||

| GDP | Private | Public | Formation | X-M:lbns E | Exports | Imports | Demand | |

| % change Q/Q (saar) ; X-M is Q/Q change in Blns of euros | ||||||||

| Q3-08 | -0.8% | 0.2% | 3.4% | 2.3% | -10.9 | 1.5% | 6.8% | 1.3% |

| Q2-08 | -0.7% | -0.8% | 3.2% | -6.0% | 2.5 | -0.4% | -1.6% | -1.2% |

| Q1-08 | 2.7% | -0.1% | 1.3% | 9.9% | 2.0 | 7.1% | 6.4% | 2.4% |

| Q4-07 | 1.3% | 0.7% | 1.3% | -2.4% | 6.4 | 1.7% | -1.2% | 0.1% |

| % change Yr/Yr; X-M is Yr/Yr change in Gap in Blns of euros | ||||||||

| Q3-08 | 0.6% | 0.0% | 2.3% | 0.8% | 0.0 | 2.4% | 2.5% | 0.6% |

| Q2-08 | 1.4% | 0.4% | 2.0% | 2.0% | 8.2 | 3.9% | 3.0% | 1.0% |

| Q1-08 | 2.1% | 1.2% | 1.4% | 2.9% | 9.6 | 5.3% | 4.3% | 1.6% |

| Q4-07 | 2.1% | 1.2% | 2.1% | 4.2% | 2.1 | 3.9% | 3.8% | 2.1% |

| 5-Yrs | 2.0% | 1.4% | 1.9% | 3.9% | 1.8 | 5.9% | 6.0% | 2.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief