Global| Jan 21 2010

Global| Jan 21 2010EMU Flash PMIs Tell Mixed tale…Improvement Continues But Pace Slows In Services (Jobs) Sector

by:Tom Moeller

|in:Economy in Brief

Summary

As the ECB is holding policy steady and ECB president, Jean Claude Trichet, is telling us that the expansion will be moderate but uneven, the Markit PMI’s are giving us some really mixed news that makes The Trichet comments look [...]

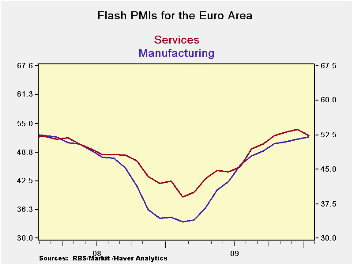

As

the ECB

is holding policy steady and ECB president, Jean Claude Trichet, is

telling us that the expansion will be moderate but uneven, the Markit

PMI’s are giving us some really mixed news that makes The Trichet

comments look positively upbeat. While both the services and the MFG

sectors are still expanding in the e-Zone only MFG was expanding faster

in January than it was in December. The services sector stepped back to

a pace that is the weakest we have seen in four months since services

made the cross-over into positive growth territory.

As

the ECB

is holding policy steady and ECB president, Jean Claude Trichet, is

telling us that the expansion will be moderate but uneven, the Markit

PMI’s are giving us some really mixed news that makes The Trichet

comments look positively upbeat. While both the services and the MFG

sectors are still expanding in the e-Zone only MFG was expanding faster

in January than it was in December. The services sector stepped back to

a pace that is the weakest we have seen in four months since services

made the cross-over into positive growth territory.

While manufacturing usually is the leading sector, what is disturbing about the services sector setback is that services is where the jobs are. MFG may be the normal leader, services is where the core of the jobs is located and is the sector households need to see improve for their fortunes to rise. Just a day ago several German officials were speaking about the economy, one, Chancellor Angela Merkel, the other, a Bundesbank Board member, with both of them saying the same thing: for Germany, domestic demand would have to do more of the work exports alone would not be enough to foster growth. For Europe the same is probably true. But if consumers do not go back to work - and that means, if the services sector does not get on solid footing - even Trichet’s luke-warm expectation for a moderate recovery may be at risk.

We know of the problems in Greece with debt and Spain with real estate. Germany is embroiled an argument over whether its budge deficit is cyclical or secular and that argument is really about how quickly it should addresses its deficit. Iceland is going to have a referendum on its financial responsibility. The UK is improving but posted a chilling inflation number. Italy has been a surprise with a recently surging MFG sector. France after looking more solid is now expecting less and is trailing other large EMU nations. The idea that the e-Zone recovery will be uneven is not hard to swallow. How strong or lasting it will be is something that will come under scrutiny especially if the service sector can’t get turned around soon. Because of the prodigious social welfare throughout the e-Zone, the service sector is not quite as critical as it is in the US. Still the Euro-backtracking on what we thought was recovery progress is a chilling and unexpected result on the day.

| FLASH READINGS | ||

|---|---|---|

| Markit PMIs for the Euro-Area | ||

| MFG | Services | |

| Jan-10 | 51.98 | 52.33 |

| Dec-09 | 51.59 | 53.63 |

| Nov-09 | 51.20 | 53.04 |

| Oct-09 | 50.73 | 52.58 |

| Segment Averages | ||

| 3-Mo | 51.17 | 53.07 |

| 6-Mo | 49.55 | 51.95 |

| 12-Mo | 43.28 | 47.38 |

| 136-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| %Range | 68.5% | 56.6% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief