Global| Oct 23 2014

Global| Oct 23 2014EMU Flash PMIs Show Life But Not Much Pulse

Summary

European markets reacted positively overnight to the release of the PMI data by Markit. The table below summarizes the recent PMI data. The table is a mixture of flash and historic (revised-flash or finalized) data. Actually, the [...]

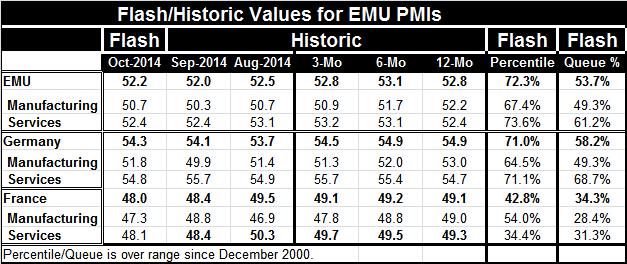

European markets reacted positively overnight to the release of the PMI data by Markit. The table below summarizes the recent PMI data. The table is a mixture of flash and historic (revised-flash or finalized) data. Actually, the flash reading for October is below the flash reading for September. But since the September flash reading was revised lower, the October flash is now higher than the finalized September reading. This is one of the reasons why we should be cautious about having too much optimism about the October numbers.

European markets reacted positively overnight to the release of the PMI data by Markit. The table below summarizes the recent PMI data. The table is a mixture of flash and historic (revised-flash or finalized) data. Actually, the flash reading for October is below the flash reading for September. But since the September flash reading was revised lower, the October flash is now higher than the finalized September reading. This is one of the reasons why we should be cautious about having too much optimism about the October numbers.

A second reason for caution is that the month-to-month increase is very small and that the current standing of the PMI values for October is still not very high. A third reason is that the momentum for the PMI gauges still has not been reversed to a positive gradient from a negative profile in any significant way.

Let's look first at the percentile standing. These are represented by the queue standings which place the current flash reading in its percentile queue among all previous flash readings. On this basis, the overall EMU (composite) standing is in the 53.7 percentile of its historic queue. That's barely above its historic median which lies at the 50th percentile. That's hardly very reassuring. The EMU manufacturing reading is in its 49.3 percentile, below its historic median. That, clearly, is a disappointment. The EMU services reading is in its 61.2 percentile. That is a more moderate reading, but it is still moderate and not strong or even firm.

It's true that the Markit indices did not continue to erode this month, but to take heart from that is to admit some grim expectations.

To evaluate the significance of the month's gains, let's look at the three-month, six-month and 12-month averages. For the EMU overall, they continue to slide. The current level in October is still below its three-month average. The same is true of EMU manufacturing. For services, there is the smallest of uptrends but the October reading is still below the three-month average reading. None of this is good momentum nor is it in the right direction, generally.

Germany and France both overall and in their components fail the momentum tests as well. German and French services sectors - the same as for EMU- show some slow crawl higher, but in both cases the October reading for services is below its relevant three-month average.

European investors are scared. They rallied on news that October was not worse than expected, but it was not very good. That means the rally is on very thin ice.

Geopolitical tensions remain. Today a Russian jet was intercepted over the Baltic Sea. The Swedes are still looking for a mystery Submarine that invaded its waters. Ukraine is poised for elections and is worried that they will be interrupted or interfered with.

The economics for Europe is still on shaky ground. The geopolitics is in worse shape than that. There was not much in this report for markets to cheer about. Granted the Chinese manufacturing index `improved' but that was thin gruel for good news as well. Be careful what you choose to call good news. The news today was not worse, but it falls far short of being reassuring.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief