Global| Jul 24 2014

Global| Jul 24 2014EMU Flash PMI Rises amid Sector Divergence; Mind the Gap!

Summary

The European Monetary Union's flash total private sector PMI rose to a level of 54 in July from 52.8 in June. That's the highest flash reading since April. The averages for 12 months, six months and three months show that progress has [...]

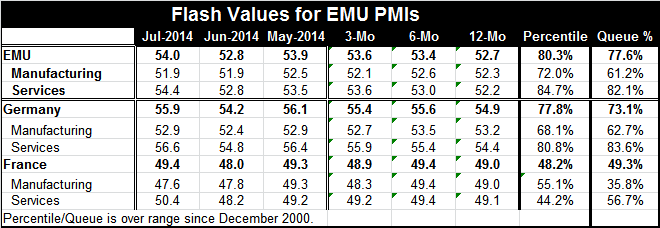

The European Monetary Union's flash total private sector PMI rose to a level of 54 in July from 52.8 in June. That's the highest flash reading since April. The averages for 12 months, six months and three months show that progress has been slow in the recent three months as that average has only slightly exceeded the average for six months. The queue standing of the overall PMI is in its 77th percentile, a reasonably strong reading.

The European Monetary Union's flash total private sector PMI rose to a level of 54 in July from 52.8 in June. That's the highest flash reading since April. The averages for 12 months, six months and three months show that progress has been slow in the recent three months as that average has only slightly exceeded the average for six months. The queue standing of the overall PMI is in its 77th percentile, a reasonably strong reading.

The manufacturing metric for all of the EMU remains frozen at 51.9 in July. It was last lower in November of last year. The manufacturing metric shows that its averages have stopped rising as the three-month average at 52.1 is below the six-month average at 52.6. The manufacturing index sits in the 61st percentile of its historic queue, a relatively moderate standing.

The services sector expanded briskly in July with the PMI value of 54.4 compared to 52.8 in June. Its moving averages show some continued upward movement in three months compared to six months. The services PMI has a queue standing that is relatively strong in the 82nd percentile of its historic queue.

There are 21 percentile points of difference between the standing of the manufacturing and services PMIs. This is a large gap and it's clearly seen on the plot of the raw indices. The manufacturing and services sectors are moving at markedly different paces with manufacturing becoming a considerable drag.

On the release of the flash PMIs, we also get country details for Germany and France.

Germany's overall PMI rose smartly to 55.9 in July from 54.2 in June. However, the sequential averages for Germany show that while there is an increase in the six-month average from the 12 month average, there is a decline in the three-month average compared to the six-month average. This implies a slowdown of the German private sector over the recent three months. The current reading of the German total PMI in July is only 3/10 of one point higher than its average over six months. Thus, while the rebound in July looks to be relatively strong, it is not impressive compared to where it's been. The German private sector index sits in the 73rd percentile of its historic queue.

Germany's manufacturing index moved up to 52.9 in July from 52.4 in June. It sequential averages show a significant decline for manufacturing over three months compared to six months. The history shows only a small pickup of the six-month average compared to the 12-month average. The manufacturing index for Germany sits only in the 62nd percentile of its historic queue. It's a moderate reading and for Germany a weak reading for the sector that is supposed to lead its economy, but instead lags behind the services sector.

Germany's services PMI rose sharply to 56.6 in July from 54.8 in June. It's sequential averages show continued improvement. Germany's services sector sits in the 83rd percentile of its historic queue, a relatively strong reading. It's unusual that Germany would be led by its services sector, instead of its manufacturing sector.

France's overall private sector PMI improved to 49.4 in July from 48.0 in June. While there is a month-to-month improvement, the indicator continues to show contraction in the French private sector. The sequential averages for the overall PMI show continued upward movement at a moderate pace. France's overall PMI sits in the 49th percentile of its historic queue, just below its median.

France's manufacturing sector slid in July compared to June, falling to a level of 47.6 from 47.8. June itself represented slippage from May. The sequential averages show that the French manufacturing PMI has been below 50 on all horizons. While it did pick up slightly from 12 months to six months, it is falling sharply in the recent three months compared with six-month average. Its manufacturing sector sits in the 35th percentile of its historic queue, extremely weak reading. Its current reading is weaker than its weakest sequential period average.

France's services sector improved in July to 50.4 compared with a reading of 48.2 in June. This is relatively sharp month-to-month jump and it more than offsets the decline that the index saw from May to June. However, France's sequential averages show that the three-month average is still below its six-month average. And the three-month average is barely above its 12-month average. This shows an extensive legacy of contraction, but of moderate contraction. The French services sector sits in the 56th percentile of its historic queue and shows expansion in July for the first time since April.

The overall PMI reading for the European Monetary Union in July appears to be pretty healthy. At 54.0 the index is higher only 23% of the time, marking this is as a relatively strong reading. However, the devil is always in the details. It's quite unusual for the countries in the monetary union and for Germany, in particular, to be led by strength in the services sector. Germany is an economy that derives its strength from its industrial base. Some noise is being made that the EMU is improving in the wake of the ECB's new credit stimulus program. It strikes me that it's a little bit too soon to credit that program with this result. I would also wonder about the prospects for success, if the European economy is to rely on its services sector. The divergence in the manufacturing and services sectors is quite marked, unusual and almost certainly not sustainable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief