Global| Nov 04 2015

Global| Nov 04 2015EMU Final Total PMI Gauge Revised Lower; Growth Yes...Momentum No!

Summary

The PMI total indices add new observations on services to the revised manufacturing readings issued earlier this week. The new total private sector index is the result. We see a slight downward revision to the EMU overall gauge and to [...]

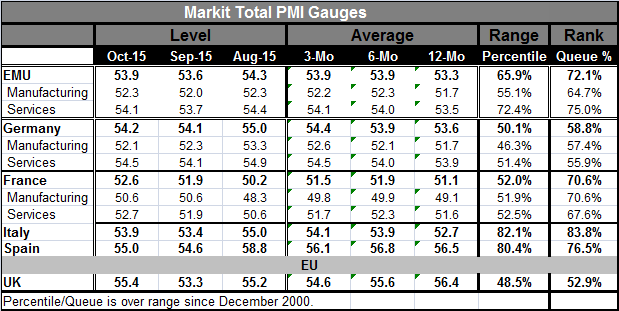

The PMI total indices add new observations on services to the revised manufacturing readings issued earlier this week. The new total private sector index is the result. We see a slight downward revision to the EMU overall gauge and to Germany's with an upward revision to France in October. The end result is that the EMU total index is higher in October and the indices for the four largest EMU economies are higher as well. That much is good news. However, compared to levels of three months ago, only France is higher. Three-month averages of the total PMIs are lower compared to six-month averages in France and Spain, but they are higher in Germany and Italy. The October total indices are higher than the 12-month averages everywhere except Spain. So there is for the most part evidence of some ongoing improvement, but it is still both erratic and limited.

The PMI total indices add new observations on services to the revised manufacturing readings issued earlier this week. The new total private sector index is the result. We see a slight downward revision to the EMU overall gauge and to Germany's with an upward revision to France in October. The end result is that the EMU total index is higher in October and the indices for the four largest EMU economies are higher as well. That much is good news. However, compared to levels of three months ago, only France is higher. Three-month averages of the total PMIs are lower compared to six-month averages in France and Spain, but they are higher in Germany and Italy. The October total indices are higher than the 12-month averages everywhere except Spain. So there is for the most part evidence of some ongoing improvement, but it is still both erratic and limited.

As for the level of these indices and signal for growth from these readings, the EMU standing is in its 72nd percentile, a relatively firm reading, but certainly not a strong one. Germany sits in its 58th percentile. Italy stands in its 83rd percentile and France in its 70th percentile. Spain is in its 76th percentile. Germany has the lowest relative standing on a percentile basis and yet has the second highest diffusion value among the four largest economies in October. Germany is well off by the standards of the three other lager EMU nations, but it is not doing well by the standards of its own history.

The services sector is driving growth (with a higher percentile standing than manufacturing) in the EMU and in France. In Germany, the manufacturing sector is stronger than services in terms of its percentile standing.

The U.K. is an EU member nation and not a single currency country. It saw its total PMI rise in October but only with percentile standing in its 52nd percentile. The U.K. has a persistent weakening in its PMI averages from 12-month, to six-month to three-month. Today the National Institute of Economic and Social Research (NIESR) cut its outlook for U.K. growth this year and next.

Despite the generally upbeat and rising trend nature of the PMI data, the percentile standings tell that Europe is not very strong. The sense of ongoing growth is that it is as easy and painless as pulling teeth. Today Mario Draghi beat the dead horse of expected ECB stimulus again and got a twitch out of it as markets reacted positively to the reference that the ECB would consider more stimulus. This is even though that same reference produced a down draft in the euro exchange rate on Monday after Draghi's weekend reference to the same thing.

Global Issues

Brazil has reported its weakest manufacturing index in 79 months. But China reports an uptick in its services index albeit from a 14-month low. Japan's services PMI also improved. Japanese consumer confidence improved in October, but it is a diffusion value with a headline still well below 50, indicating confidence is falling more slowly.

Every silver lining seems to have a cloud these days. While markets were seeing some upside today, little of it seems connected to the release of the day's data. There is still little to cheer about.

In broader perspective, the geopolitical news today was somewhat chilling. CEE and Baltic nations expressed worries in a joint statement they issued about Russian aggression. They back a sustainable NATO presence in their region. ASEAN countries met and -not surprisingly- had no agreement on a South China Sea statement. China and Taiwan announced a surprise historic meeting of their two leaders would take place, the first since 1949. This is the big geopolitical news of the day and the real question is what it will mean with China seeming to be flexing its expansionist muscle in the South China Sea region. That flexing has even encouraged North Korea to more vehemently assert its claim to larger portion of its own coastal waters.

As we ponder shaky economic improvements, we can't ignore even shakier geopolitical times. The U.S. now has boots on the ground in Syria, but not many of them. What happens if ISIS captures an American soldier there?

I do not see much on the economics side that is truly encouraging. The geopolitical environment is fraught with danger. The U.S. is going to keep sending ships through the South China Sea to deny China's claims there. The Chinese have warned how dangerous that is and that a small error could lead to dire consequences. Was that a statement of fact or a threat? What about Russia in the Baltics and in Syria? What about Iran and the new nuclear deal?

Does anyone really care if there is any more monetary stimulus anywhere? Is there any evidence that it is doing any good? How about the counterfactual? How much slower would things be without this stimulus? There are bigger fish to fry than worrying about central bank policy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief