Global| Jan 09 2017

Global| Jan 09 2017EMU: Fast Rising Inflation Meets Falling Unemployment Trend-Collison Course!

Summary

In the euro area, unemployment which was flat month-on-month in November is nonetheless moving lower on trend as the inflation rate has spiked up, boosted by oil. This combination of motions is surely going to put pressure on the ECB [...]

In the euro area, unemployment which was flat month-on-month in November is nonetheless moving lower on trend as the inflation rate has spiked up, boosted by oil. This combination of motions is surely going to put pressure on the ECB since European growth is still not stellar or even as good as the unemployment rate makes things seem. But the ECB's mission has only one pillar and that is to contain inflation. German financial publications and Jens Weidmann, head of the Bundesbank, already are laying the ground work and pressuring the ECB to heed the call of fast rising inflation. However, the core inflation measure remains much more subdued and inflation is clearly being boosted mostly by energy prices (not that the ECB charter 'cares' about that).

In the euro area, unemployment which was flat month-on-month in November is nonetheless moving lower on trend as the inflation rate has spiked up, boosted by oil. This combination of motions is surely going to put pressure on the ECB since European growth is still not stellar or even as good as the unemployment rate makes things seem. But the ECB's mission has only one pillar and that is to contain inflation. German financial publications and Jens Weidmann, head of the Bundesbank, already are laying the ground work and pressuring the ECB to heed the call of fast rising inflation. However, the core inflation measure remains much more subdued and inflation is clearly being boosted mostly by energy prices (not that the ECB charter 'cares' about that).

Unemployment is lower but still not low: Dispersion an issue

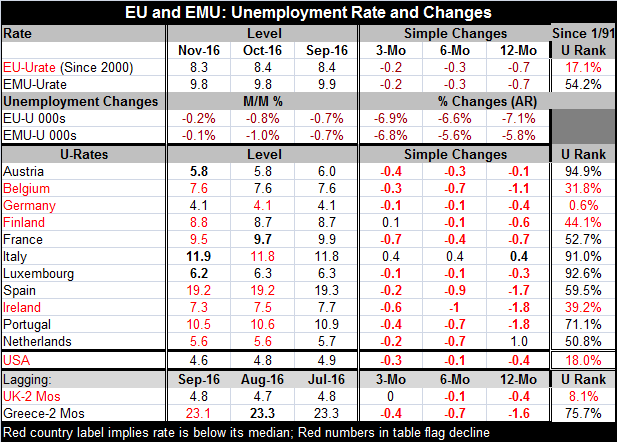

The unemployment picture revealed in the table above shows how varied the unemployment situation is in the EMU at the moment. Overall the unemployment rate in the EMU is in its 54th percentile since early 1991. The standard deviation among the unemployment rates of these up-to-date reporting original EMU members stands in the 58th percentile of its historic queue of such data. That means that the dispersion among members is still higher than normal and it also has stopped the trend to normalize (to eliminate divergences and to bring unemployment rates into closer alignment across member countries). The EMU-wide rate is above the 50 percentile mark in its queue standing; that is slightly above its period median. For the EMU the current rate at 9.8% is still above its median and average rate both of which are at 9.1%. So while inflation is moving up rapidly, the unemployment rate in the EMU is still significantly above its average and median. But a detailed look at the individual country circumstances finds even more distressing comparisons across national rates of unemployment.

Very different country issues

For the 11 original EMU members detailed in the table, only four have unemployment rates below their respective medians since 1991. Belgium's rate has been lower only about 31% of the time while Ireland's rate has been lower about 39% of the time and Finland's rate has been lower about 44% of the time. The downward pressure on the EMU unemployment rate comes mostly from its largest economy, Germany, where its rate has been this low or lower only 0.6% of the time. The German unemployment rate is on its reunification low. And its weight in the EMU area is responsible for making the EMU rate look even lower than it is for most members. Germany is in a situation with inflation rising (higher than in the EMU!) and with the lowest unemployment rate in the EMU. For Germany, a rate hike makes sense now. But for the rest of the EMU, that is not so. Austria, Italy and Luxembourg have unemployment rates that have been higher less than 10% of the time. Portugal's rate is higher less 30% of the time. France and the Netherlands have unemployment rates that are closer to their historic medians and means. Greece - that reports its unemployment rate with a lag - has a rate that has been higher less than 25% of the time. Greece's rate is about 20% and Spain's rate is close to 20%. Portugal and Italy have rates that still are in double-digits. These are a far cry from Germany's 4.1%.

Does EMU face inflation or a relative price bump up?

One concern is that hiking rates to fight what is mostly oil-generated inflation is aiming monetary policy at what is mostly a shift in relative prices not so much in inflation. A counter argument to hiking rates might be that there is enough slack in the EMU that inflation really does not stand much of chance of taking root and that the bump up of the headline to and beyond 2% would be temporary, induced by oil prices alone and not worth aiming policy at - especially after such a long run with inflation below it goal. Of course, the German's don't see things that way - ever. But will the ECB be willing to cast its eye on inflation in that way looking forward more the way the Fed does instead of looking backward at what inflation has been (will it emphasize inflation over the past 12 months, instead of over the next 12 months, for example).

But EMU is doing so well with unemployment broadly dropping

Moreover, unemployment is falling across the EMU with the lone exception of Italy. Over both 12 months and six months, Italy is the only country with an unemployment rate that is higher on balance- everywhere else unemployment rates have fallen (the lone exception is the Netherlands over 12 months) and that includes the lagging data from Greece as well as for EU member the U.K. Over three months unemployment rates are rising only in Italy and Finland- Finland by 0.1 percentage point.

The unemployment rate level conundrum

I include the U.S. in this table and it shows that the U.S. unemployment rate is low and falling, closer to mirroring the performance of Germany than any other country in the table. Falling unemployment rates in the U.S. and in Europe are the basis for a lot of the economic optimism. Yet, economies are not performing as well as the dropping unemployment rates suggests. And the percentile standings remain elevated since unemployment rates are still quite high. With the EMU rates at 9.8% and the last year's drop in that rate at 0.7 percentage points, it will take another 12 months before the EMU rate gets down to its historic mean and median readings. Yet, Germany is pressing already to remove stimulus. And the question is this: if stimulus is removed, will the rate continue to drop or will the drop in the unemployment rate give way to increases? With the unemployment rate in the EMU not yet down to its median or average by that logic, it is far too soon to begin to tighten policy and to stop or reverse the progress on the unemployment rate. However, the unemployment rate, of course, is not part of the ECB's mandate.

Change displaces the 'same old same old'

These issues will help to define the coming battle over policy in Europe. Not only does the ECB have its job cut out for it, but the U.K. too is still embroiled in the Brexit process. This weekend Prime Minister Theresa May made a comment about the U.K. and the prospect of a hard Brexit that hit the pound sterling hard. Policymakers in Europe still have a tough row to hoe and markets are still at risk to untimely statements let alone to eventual policy decisions that must be made. With the U.S. leading the way and launching its second rate hike in one year's time and an outlook for higher rates backed by a growing chorus of FOMC members, there is also a growing consensus globally that policy elsewhere will be changing too. Right or wrong it's a year to be on guard for policy change.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief