Global| Jul 30 2013

Global| Jul 30 2013EMU/EU Indices Show a Real Rebound

Summary

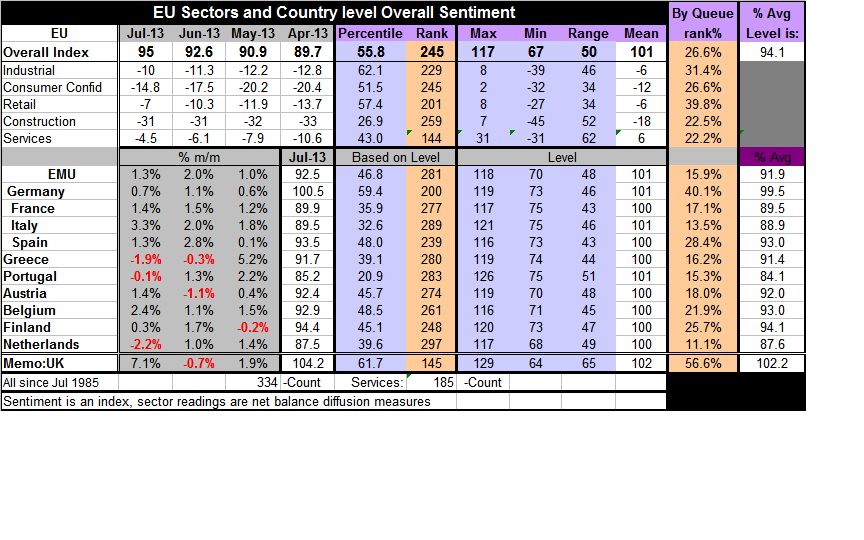

The EU index in July rose to 95 from 92.6, a relatively large jump the ranks 20th out of about the last 250 observations; that places it in the top 11% of all monthly changes over that period. Consumer confidence made a particular [...]

The EU index in July rose to 95 from 92.6, a relatively large jump the ranks 20th out of about the last 250 observations; that places it in the top 11% of all monthly changes over that period. Consumer confidence made a particular large increase in the month rising to -14.8 from -17.5, a spurt that ranks it as the 10th largest monthly rise among the last 250 observations. Retailing improved to -7 from -10.3 also a relatively substantial jump. The services sector improved to -4.5 from -6.1. The industrial sector improved to -10 from -11.3. Construction was flat on the month at -31.

The EU index in July rose to 95 from 92.6, a relatively large jump the ranks 20th out of about the last 250 observations; that places it in the top 11% of all monthly changes over that period. Consumer confidence made a particular large increase in the month rising to -14.8 from -17.5, a spurt that ranks it as the 10th largest monthly rise among the last 250 observations. Retailing improved to -7 from -10.3 also a relatively substantial jump. The services sector improved to -4.5 from -6.1. The industrial sector improved to -10 from -11.3. Construction was flat on the month at -31.

The country by country data show that we have three increases in a row for Germany, France, Italy, and Spain four largest countries in the euro-Zone. Belgium also has posted three consecutive monthly gains. Greece shows declines in its EU index for two consecutive months after a strong May. Portugal and the Netherlands have declines in the month of July. While the UK, an EU member country, shows an outsized gain of 7.1%, a gain that is the fourth-largest in the history of its monthly increases.

In the wake of these improved numbers for the UK two former Bank of England policymakers have said that the UK economy now has achieved escape velocity. We will see if they can keep this up. The monthly UK numbers are impressive.

The chart at the top shows the relatively mild improvements occurring among the larger EMU member countries. Below we see a somewhat more jagged response from what have been the more troubled EMU member countries. When we evaluate the indices for the 10 original EMU members (named in the table), along with the UK, we see Germany is doing the best among EMU members, followed by Spain and the UK in terms of getting its current reading back to its cycle peak. IN terms of the outright queue standing The UK has surpassed Germany this month. Germany's current index is approximately 84% of its cycle peak while Spain is at the 80.7th percentile. The UK is at the 80.8 percentile. The weakest country in terms of getting back to its past cycle peak is Portugal which is back to 67.8 percentile next is the Italy at the 74.3 percentile and the Netherlands at the 74.9th percentile.

This analysis instantly isolates Portugal as a country that is doing the relative worst even though Portugal is often cited as a country that has done the best job of trying to adhere to the austerity strictures have been placed on it. It's no wonder that austerity is getting a bad name and is being abandoned or at least substantially watered down across the euro-Zone when its best student is getting a failing grade.

When we evaluate these countries in a slightly different manner, taking their current index readings as a percentage of their cycle peak range relative to their cycle trough, results are only slightly different. The UK emerges as the strongest economy at the 62nd percentile of its high low range, Germany is a close second at the 59th percentile. But, coming in last once again is Portugal, at about the 21st percentile with Italy in the 32nd percentile quite a ways up the scale form the weakness been registered in Portugal.

The industry index for EMU places that sector in the 31st percentile of its historic queue led employment expectations (50th percentile), export orders (35th percentile), and production expectations (33rd percentile). Before sending up the fireworks note that order volumes (26th percentile) lag all other measures. Although export orders stand higher most of the 'optimism' is linked to expectations readings not to real order values improving.

The industry index for EMU places that sector in the 31st percentile of its historic queue led employment expectations (50th percentile), export orders (35th percentile), and production expectations (33rd percentile). Before sending up the fireworks note that order volumes (26th percentile) lag all other measures. Although export orders stand higher most of the 'optimism' is linked to expectations readings not to real order values improving.

The consumer confidence measure is still week for EMU lying in the 15th percentile of its historic queue of values. Consumers' assessment of the time being right to make major purchases is now improved on the month and is one of the stronger components residing in the 43rd percentile of its range. However, looking ahead to the next 12 months, that percentile reading falls to the 19th percentile for spending. Unemployment expectations are making important contributions to boosting this index as expectations for unemployment have fallen to 30 in July from 33 in June. The month before, in May, a value of 37 was posted; it stood at 38 in April. This is a relatively rapid progression to less unemployment fear.

The services sector improved to -8 from -10. Business climate improved to a reading of -12 from -15. Current demand improved, expected demand improved, while current employment made the largest shift upward to -4 from -7. While expected employment made a smaller positive move. Looking at the big-four countries in EMU Germany, Italy, and Spain each showed improvements in the services sector but France took a setback in July slipping to -16 from -15. France's services sector resides in the bottom 6% of its historic queue compared to the 30th percentile for Germany the 26th percentile for Spain and the 16th percentile for Italy.

Overview:

Conditions in the European Union as well as the monetary union felt relatively broad-based improvements. However the ranking of countries that are improving does not speak highly of the austerity strategy that's been used to stabilize Europe. Germany continues to outdistance all monetary union members while the UK is beginning to surpass even Germany in some measures.

The UK of course is a country that has employed austerity but is also had an independent monetary policy. The UK has seen its monetary growth boom and bust and it has allowed an overshoot with inflation persistently above target while it was running its austerity program. UK also used the tool of quantitative easing which has been unavailable in the monetary union.

While it certainly too early to make any final judgments, and while UK growth looks like it's beginning to turn the corner, a preliminary assessment would seem to score the UK policy mix as superior to the monetary union's policy mix. The availability of a flexible monetary tool and the way it was employed in the UK seems to have helped UK economic performance compared the EMU economic performance. Not only is the UK performing much better than any country in the monetary union that used the austerity approach, the UK is even, in terms of its rebound, improving faster than Germany the best-performing country in EMU.

No one should be surprised by this. The first thing it says is that the Bank of England knows what it's doing -- no surprise there. The second thing it says is that when a country has a monetary policy tool that can be used specifically to complement the other policies that are at work in its economy its performance can be superior to an economy running a generic monetary policy.

Monetary policy in EMU was neither tailored for the strength in Germany nor for the weakness in southern Europe. While the European central bank did what it could to try to address local circumstances the Germans largely tried to prevent it from engaging in too many regional policies arguing that they were outside of its mandate and not approved by The Treaty. Germany was concerned that too much localism could undermine the general thrust of monetary policy in the monetary union while it was the lack of localism the made the bite of austerity so much more severe in countries are forced to pursue it.

I believe one clear lesson for the monetary union is that it lacks the flexibility to address regional differences and that local fiscal autonomy is not enough. Right now the only local policy possible IS fiscal policy- but that has been dedicated to remedy long-standing excesses instead of to apply to cyclical needs. I would argue that to keep the need for regional flexibility from degenerating into a political argument among member countries, regions it should be drawn up that make economic sense but that do not conform to national borders. In that way regions can be established that might be eligible for different kinds of assistance without immediately raising concerns about nationalism.

The monetary union also needs to press ahead to remove any exceptions of local industries to EMU wide competitiveness rules. The existence or persistence of inflation differentials among EMU member countries should be taken as prima facie evidence that rigidities exist in those countries that are able to run persistently higher rates of inflation than the community as a whole. Such evidence should be followed up by investigations with the intent to implement policies to remove the rigidities that are creating or permitting the persistence of excessive inflation.

If the monetary union is going to move forward it is going to have to have some ability to deal with the kinds of local differences that have emerged and that austerity has not been able to deal with. While the run of austerity that was put in place may have gone part of the way toward the moving countries in the right direction, there are still vast differences in competitiveness within EMU. They are going to continue to create problems for true euro-Zone integration. We can take some solace in the fact that Europe seems to be on some sort of road to recovery. But we have no assurance it's going to stay on the road or that if it drifts off the road the consequences would be benign.

The last thing policymakers need to do is to assume that they have dodged a bullet and were now on the road to recovery and we simply need to manage a period of growth.

We do not need to continue to have sleepless nights. But we do need to remember the problems that got the international economy, US economy, the European economy, the Chinese economy, the Japanese economy, and the BRICs into trouble. We need to recall how disturbances of various sorts worked their way through the international connections in the international banking system. Most of the things that went wrong have not yet been fixed. There has been a great deal of attention to the international banking system but force-feeding banks capital and making sure that you can bury them if they die is not a cure-all.

The international exchange rate system continues to be a rogue system that does not rationalize itself to any concept of economic equilibrium. It's not a system it simply is...It's existential. It exists and permits transactions but it does not have an equilibrating role in the economic system. Too many countries run persistent balance of payments surpluses and too many others run persistent deficits while the exchange rate system does not help to equilibrate these imbalances. Meanwhile, these imbalances themselves pose systemic risks. Bankers attempt to make investments work in an environment where the flow of funds is irrational and continues to be a threat to the international monetary system.

There is an important and significant need to address and remedy the international monetary system, the rules for trade and for surplus and deficit countries to confront and solve the problems of imbalances. That need is at least as pressing as the need for the European Monetary Union to get its act together. These objectives will be pursued in an environment where China and Japan continue to try to repair the problems in their domestic economies and where new issues have arisen in the BRIC economies as their strategies of export led growth no longer will work. Things are not going to get any easier; they are going to get harder. By that I mean that despite some improved growth the rivalries among countries, each trying to get back to where it was in terms of past rates of growth, will make it difficult to secure international agreements when those agreements will require economies to restructure or obey rules that might further impede them form reacquiring their recent economic rates of growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.