Global| Sep 13 2013

Global| Sep 13 2013EMU Employment Losses Slow

Summary

Both the European Monetary Union and the European Union are seeing declines in the number of unemployed over the past two months. The pace of the decline slowed in July compared to June as both regions saw the number of unemployed [...]

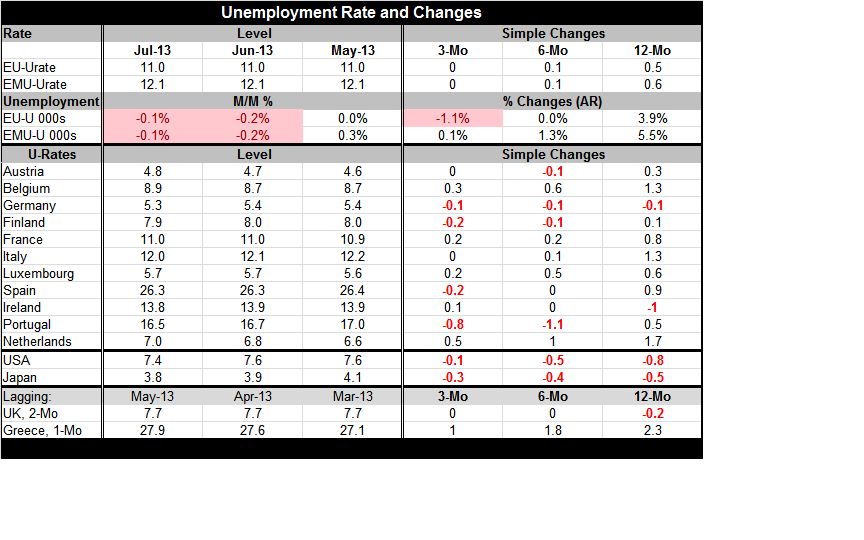

Both the European Monetary Union and the European Union are seeing declines in the number of unemployed over the past two months. The pace of the decline slowed in July compared to June as both regions saw the number of unemployed fall by 0.1% after they both had seen declines of 0.2% in June. The number of unemployed declined at a 1.1% annual rate over the last three months in the European Union while it rose by 0.1% in the European Monetary Union. Over 12 months the number of unemployed has risen by 5.5% in EMU compared with a 3.9% increase in the European Union and large.

Both the European Monetary Union and the European Union are seeing declines in the number of unemployed over the past two months. The pace of the decline slowed in July compared to June as both regions saw the number of unemployed fall by 0.1% after they both had seen declines of 0.2% in June. The number of unemployed declined at a 1.1% annual rate over the last three months in the European Union while it rose by 0.1% in the European Monetary Union. Over 12 months the number of unemployed has risen by 5.5% in EMU compared with a 3.9% increase in the European Union and large.

Countries continue to experience very different rates of unemployment and different patterns in terms of the improvement or deterioration of employment conditions. Over three months the unemployment rate fell in four of 11 of the EMU countries that reported July unemployment. The unemployment rate fell by a sharp 0.8% in Portugal, by 0.2% in Spain and in Finland, and by 0.1% in Germany.

In contrast the unemployment rate rose by 0.5% in the Netherlands, by 0.3% in Belgium, by 0.2% in Luxembourg and in France, while the rate remain unchanged in Italy and in Austria. Greece, whose data lag by one month, say its unemployment rate rise by a full percentage point over the last three months, for the period ending in June. The UK which is an EU member has unemployment data lag by two months saw, in its case the three-month period ending in May, an unemployment rate that was unchanged.

The levels of unemployment of course are going to continue to display tremendous differences over a long period of time. Unemployment is a wound that is slow to heal. Spain reports an unemployment rate of 26.3% in July; Greece's rate hit 27.9% in June. The next highest unemployment rate is in Portugal at 16.5%, followed by Italy at 12%, and France at 11%. After those we see Belgium at 8.9%, Finland at 7.9%, The Netherlands at 7%, and so on. The lowest rates of unemployment are in Austria at 4.8% followed by Germany at 5.3%.

It's not surprising that making monetary policy in this environment is extremely difficult. For now the ECB is trying to temper its policy. It has adopted a plan of forward guidance which is being used by the Bank of England and was pioneered by the Federal Reserve and United States. In England the plan is under attack. In the monetary union Jens Weidmann, head of the Bundesbank, has said that forward guidance would not keep the ECB from raising rates if monetary policy requires it. That sort of statement makes you wonder what forward guidance could possibly be worth. At this point central banks are scraping the bottom of the barrel for anything they can possibly do to try to improve sentiment and encourage growth.

In the European Monetary Union over the 12 months ended in July only Germany and Ireland have net lower rates of unemployment. With a one-month lag Greece, the country with the highest unemployment rate in the union has seen its rate rise by an additional 2.3 percentage points while Spain, the country with the second highest unemployment rate has seen its rate rise by 0.9 percentage points. If we set the case of Ireland aside, is a pretty clear case of the countries with the lowest rates of unemployment seeing the biggest declines in unemployment or smallest increases over 12 months, compared of the countries with the largest rates of unemployment that are seeing the biggest increases in unemployment over the last 12 months.

This is clearly a policy dilemma/an economic fiasco.

The ECB has nowhere to go with this problem. For the time being the IMF is trying to prod the Monetary Union into formalizing its banking union so that it can play some role in backstopping European banks that are clearly still in a difficult state following the financial crisis and the weak economic performance thereafter. But local fiscal policies are largely being straitjacketed by austerity agreements, while there remains no zone-wide fiscal mechanism with none really under consideration.

This is why despite the recent upswing in the various PMI indices for manufacturing and for services I remain off the bandwagon of European recovery. While according to some measures recovery is gaining pace there are important ingredients that are being left out of the recipe for sustained growth. Europe is not yet come to any agreement about whether the countries that have been under the yoke of austerity will gain any slack in an attempt to create Zone-wide growth. If they don't it's hard to see how growth will be able to take hold. What we see now is that the relatively less affected countries are able to make some progress and there is very little of that stimulus is being spread to other nations.

The employment losses that persist across the Zone are beginning to abate somewhat in the second quarter. However, the unemployment statistics continue to tell a story that is chilling from the standpoint of policymaking. Europe simply appears to have painted itself into the corner and the paint seems to refuse to dry.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief