Global| Jun 20 2013

Global| Jun 20 2013EMU Down-Draft Abates

Summary

The flash readings for Markit's manufacturing and service sector PMIs both rose in June, indicating the least amount of contraction since March of 2012 for the service sector (compared to finalized data) and since February of 2012 for [...]

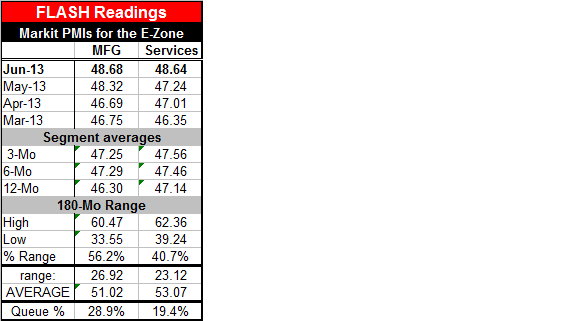

The flash readings for Markit's manufacturing and service sector PMIs both rose in June, indicating the least amount of contraction since March of 2012 for the service sector (compared to finalized data) and since February of 2012 for the manufacturing sector.

The flash readings for Markit's manufacturing and service sector PMIs both rose in June, indicating the least amount of contraction since March of 2012 for the service sector (compared to finalized data) and since February of 2012 for the manufacturing sector.

The downdraft in Europe seems to be slowly dissipating. The chart shows a relatively stronger and longer-lived rise for the manufacturing index compared to the services index. Indeed, the manufacturing PMI stands in the lower 29th percentile of its historic queue compared to a 19% standing for the services sector. Both of these are still extremely low readings. Viewed another way, the manufacturing index is at 95% of its historic average compared to services which is at the 91st percentile of its historic average.

Both indicators are below the mark of '50' indicating ongoing contraction; both of them are below their historic mean indicating weaker than normal activity. And both of them are on an improving trend of some sort.

The manufacturing index has been moving up relatively strongly since about August 2012. During that move, there was a decline in October 2012 and two recent declines in March and in April 2013. The increases in May and June 2013, however, have now brought manufacturing back up to a local cycle high reading, its best since February 2012.The services index shows a much flatter profile. It has now risen for three months in a row after falling for two months in a row in February and March; it has generally been increasing since October 2012.

Other Euro area data continue to be mixed. The economy in Europe is still not doing well, but the PMI data are speaking to the issue of the degree of decline and that is letting up. Europe has great internal differences in terms of the PMI values for individual country members. We will get more on that when the final figures are released. For now, we will note that France's PMI index for manufacturing jumped in June to 48.3 from 46.4 in May- even so that measures a decline in the French MFG sector. France's services PMI rose by more than two points on the month as well. In Germany the two sector PMI gauges translated into a net gain in its private sector in June for the second month in a row. Even so, the German MFG sector took a step back to 48.7 in June from 49.4 in May.

Conditions in the Zone remain somewhat unpredictable in spite of the month's overall improvement. The news today from China of a weakening in the MFG PMI there is an offsetting bit of disturbing global news. Early data in the US seem to be better than expected for housing and for a regional MFG report on manufacturing from the Philadelphia Fed region.

Still, markets are wary about the Fed down-shifting its support. Data have blown hot and cold. While Europe seems to have a trend improvement in train (less weakness) markets and central banks remain wary, The Fed, in its zeal to end QE, still is using language of a very hedged nature. Meanwhile, many inflation-sensitive indicators are very weak with silver looking especially weak in today's trading. The global economy is in flux if not in play. Many Fed watchers are trying to square the Fed's newest policy choice and bond market reactions with the ongoing weak -and weakening- inflation picture globally and in the US itself.

The picture is perplexing. The outlook while possibly better and stronger is also still with a good deal of risk even as the Fed says it sees less risk. The recent drop in inflation has caught some attention but not yet headlines and is the focus of at least one Fed member, St Louis Fed President, James Bullard. There are still a lot of interesting international twists and turns in the data that merit our full attention. We are not yet 'off to the races' despite what some of today's data might suggest.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief