Global| Jan 19 2017

Global| Jan 19 2017EMU Current Account Surplus Trumps the Past...All of It

Summary

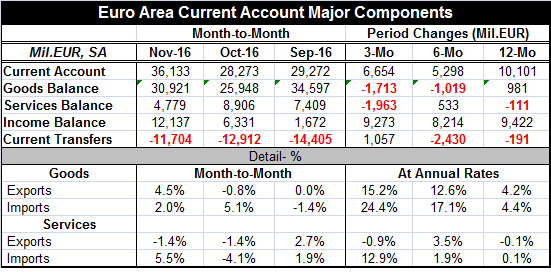

The euro area has set a new record high current account surplus at 36.1 billion euros in November. And while the ECB has just met and decided to kick the can down the road for a bit longer, international policy is showing itself to be [...]

The euro area has set a new record high current account surplus at 36.1 billion euros in November. And while the ECB has just met and decided to kick the can down the road for a bit longer, international policy is showing itself to be a major source of misalignment and of trouble making in the euro area and beyond.

The euro area has set a new record high current account surplus at 36.1 billion euros in November. And while the ECB has just met and decided to kick the can down the road for a bit longer, international policy is showing itself to be a major source of misalignment and of trouble making in the euro area and beyond.

Trade and foreign exchange policy are way out of whack and that is starting to get notice. The U.K. pulling out of the EU is an example. U.K. Price Minister Theresa May has in Davos repeated a well-known but oft ignored truism about trade. Global trade needs to benefit everyone. Reaping benefits from trade is not about mercantilism or exploitation. When we speak of international trade and its benefits, we speak of the characteristics that make it desirable like the exploitation of the principle of comparative advantage and the fact that in free trade the results are mutually beneficial. PM May has extoled leaders and countries to treat all companies the same for international taxation so that false incentives are not created for the purpose of exploiting the tax code. There have been recently backlashes over allowable tax loop-holes as the EU Commission has been on a witch-hunt to stop practices it views as excessive.

While Prime Minister May prepares the U.K. for a new world perhaps one quite disconnected from its former EU centric world, the rest of the world should take a moment to assess where it stands as well.

The EMU has a huge current account surplus by global standards, and the largest in its history. Germany is a big reason why. Germany is highly competitive economy with its exchange rate wrapped in the enigma of a weak currency zone and that is leading to trade distortions and a ramping up the EMU surplus. The cozy arrangement that Germany has engineered for itself is now creating tensions of various sorts although the Germans are prone to blame others. After all, they are only being prudent on the inflation front and fiscal front and so on. The exchange market is driving the euro lower increasing German competitiveness. The strong German trade position is heating up the German economy to a temperature that exceeds that of the rest of the euro area. Because Germany has such a large weight in EMU statistics, this could cause EMU-wide overheating to appear to be occurring event though much of the euro area would still be experiencing a chill.

The election of Donald Trump in the U.S., whose inauguration is January 20, is another example of politics brought to the fore on the back of trade policy issues. Trump is saber rattling about a more aggressive U.S. trade posture and he is getting a lot of 'bad press' from the traditional economic elite. Many are worried about Trump's aggressive posture and his apparent rejection of free trade. But free trade is the last thing that Trump is rejecting. What he is trying to combat are these cozy back door baked-in-the-cake arrangements such as the one Germany has concocted in Europe.

Countries around the world along ago rejected obeying the 'rules of the game' that economists recognized would make a system of fluctuating exchange rates stable and self-policing. Since countries have chosen to manage exchange rates instead of letting the system manage itself and since they have mismanaged it, they have created a system that has produced intractable imbalances instead of one in which balances would eradicate themselves. Many Asian countries have jumped on the bandwagon of the managed exchange rate system and treat its manipulation as a 'right.' After Japan used it so successfully to develop and then was caught by U.S. demands for a stronger currency, the benefits of currency pegging and the dangers of currency appreciation have colored everyone's perception of how the foreign exchange market should work.

Yen strength ultimately hurt the Japanese economy and spurred development in the Asian region as Japanese firms refused to let their dollar prices rise as the yen rose and instead sought a cheap place to produce in Asia to preserve their market share. Japan's experience with currency appreciation left China with no taste for it at all. But without currency flexibility, the current account surpluses and deficits can and will become entrenched as they have. Surplus countries (current account surplus) should see their currencies rise to diminish their surplus. Deficit country currencies should fall to diminish their deficits. These are the basic rules of the game that have not been followed and have led us the brink of a trade war. I hardly think it's appropriate to blame Donald Trump for recognizing that the deck has been stacked against the U.S. and for taking steps to end the exploitation of the U.S. economy because of a tricked-out financial system.

It should be obvious that without market-determined exchange rates you do not get free trade or its many benefits. Since exchange rates have been set to fluctuate, the U.S. current account has been in surplus only 16% of the time. Less developed economics see the U.S. market as the bullseye in their target for export-led growth. But as we are finding out, 'everyone' cannot have export-led growth. What a shock. And since there is no move toward currency reform to reinstate the automatic workings of the international financial system, Donald Trump is stepping outside of it to threaten to use commercial policy to bring leverage. Shame on any international economist that bashes Trump for undermining free trade in a world where such a thing does not exist! Since you can no more have international currency reform as one country than you can dance the tango with yourself, Trump is using the only tool at his disposal to try to correct the imbalances thrust on the U.S. by currency manipulation in most of the rest of the world/ yes, that is in 'most of the rest of the world.' Yes, and you can wipe that 'Who me? Smirk off your face too. This cheating game is over.

Unfortunately you cannot run time in reverse. China is now saying that it can work with the U.S. on trade. Well can it really? Certainly the chances of the yuan being part of a currency system where exchange rates are freely determined have been lost. China has fouled its own nest in more than one way. It continues with its information control policy and some relatively heavy handed policies that have empowered local resistance. Free trade and the free flow of goods and information all go hand in hand. At the same time, the poor economic development decision to have ramped up growth at the expense of the environment has alienated a lot of Chinese citizens. Not surprisingly, many Chinese are seeking to leave and want to move their wealth out of the country something that now puts never ending downward pressure on the yuan exchange rate. Purchasing power parity for the yuan is no longer a viable goal since capital flight has become a main objective of many Chinese citizens. China will need to operate with capital controls in place for some time because of this. This just one example of how opportunities can be lost forever.

Bad mouthing Trump is very popular among main stream economists and those who have served in Democrat Administrations. I do not defend his policies as optimal, but perhaps they are workable. Certainly 'business as usual' 'pretending' that we had free trade and letting the last charade play on and on as the U.S. would lose even more jobs as U.S. firms would have continued to place all their newest and best investment overseas, hardly seems like a better state of affairs than the one Trump is trying to engineer with a more balanced role for the U.S. economy. But then, some simply refuse to see it in that light. Yet looked at through the lens I suggest, there is actually hope that Trump's method/madness can orchestrate the changes that previous administrations could not and shine a bright light on the set of lies that have been told in recent years about free trade. Because if we are not honest with ourselves about what is going on, how are we ever going to understand it and or fix it? We do not now have free trade and since rates were set to fluctuate we have in many ways been moving farther away from a system that looks and operates like free trade. The commercial policy aspect (tariffs and other nontariff barriers) may have been reforming steadily. But there are still many institutional impediments as well as the vexing refusal of countries to let currencies speak with a free voice unimpeded by crass and persistent policy manipulation. China has trillions of dollars in foreign exchange reserves. And it is not alone in amassing such a war chest. You do not buy billions or trillions of dollars of anything (including dollars!) without affecting its value. Don't kid yourself.

Having said all of that, Donald Trump still has very tough row to hoe. Mike Pence on Fox News yesterday reinforced this idea of Trump wanting a weaker dollar. But Trump's pro-growth pro-business economic policies have been making the dollar stronger! Trump's criticisms of the Fed that it held rates down too low for too long will lead to a reversal and higher U.S. rates will underpin a stronger dollar not a weaker one. In the 'war of words', Trump and Pence made their weak dollar points but ultimately were themselves 'trumped' by Janet Yellen yesterday and her remarks about coming rate hikes in 2017. Right now the problem is that whatever structural needs the U.S. economy has cyclical forces are pushing the dollar higher. And that may mean that to reach his goal of using trade for job creation Trump will have to lean harder on commercial policy vehicles. No one said it would be easy or riskless. Economic policy is going to become much more interesting in 2017. It's the year of the rooster and we have yet to see who is going to crow.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief