Global| Jan 16 2015

Global| Jan 16 2015EMU Car Registrations Weaken in December but Mark Calendar Year Gain

Summary

EMU car registrations fell in December on the back of a decline in November. While that is not a strong ending to the year, 2014 was the first year since 2009 that calendar year car registrations rose in the EMU. Sales rose by 3.6% [...]

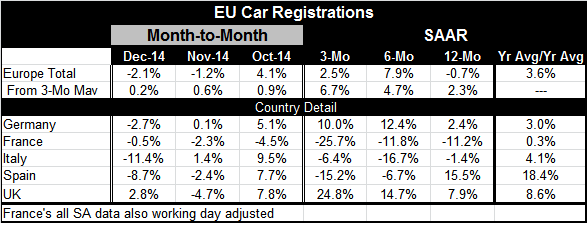

EMU car registrations fell in December on the back of a decline in November. While that is not a strong ending to the year, 2014 was the first year since 2009 that calendar year car registrations rose in the EMU. Sales rose by 3.6% for all of the EMU. They skyrocketed by 18.4% in Spain. Sales were up in the U.K. by 8.6% (not a single-currency member country). Sales rose by 4.1% in Italy and by 3% in Germany.

EMU car registrations fell in December on the back of a decline in November. While that is not a strong ending to the year, 2014 was the first year since 2009 that calendar year car registrations rose in the EMU. Sales rose by 3.6% for all of the EMU. They skyrocketed by 18.4% in Spain. Sales were up in the U.K. by 8.6% (not a single-currency member country). Sales rose by 4.1% in Italy and by 3% in Germany.

But yearend, momentum has been poor in the EMU. Over three months, sales are advancing only in Germany and the U.K.

Car registrations and retail sales volumes have generally been on the mend in the euro area. Since 2010, their recovery period profiles have been largely the same. While we see recoveries in both series from 2013 onward, both are substantially below the 2006-2008 levels.

What we see is a revival on track for consumer spending on autos and in retail sales in general. Consumers have responded to sales incentives to purchase vehicles when those have been put in place. But of course, that is not to deny that there is still a bifurcation of the economy. Some consumers are doing better than others. The unemployment rates in European nations still are generally high. The up-to-date PMI surveys have not painted a picture of an improving economy.

Instead, Europe still appears to be wallowing in weakness partly impacted by sanctions on Russia and because of lingering fiscal austerity. The more that deflation trends stick around, the more deleveraging consumers will do. The optimal amount debt to hold falls as inflation is lower. But coming to the rescue in 2015 will be a QE program by the ECB, the way for which the legal system has now cleared. Ongoing weakness in the euro exchange rate will boost the region's competitiveness even more aiding export-led growth. My view is that the weak euro will be the stronger force of the two. With interest rates so low in the EMU, I do not even think QE can be effective. Because of its nature, in fact, a QE program at this point is mostly set to inflict losses on the ECB as it carries out the operation.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief