Global| Nov 06 2019

Global| Nov 06 2019EMU Area PMIs Quiver As German Orders Rebound But Still Shiver

Summary

Both German orders and the EU Commission's PMI gauges for the EMU show a modest upturn in their recent releases. Both fared slightly better than expected. Both are still significantly weak; the sense of overachievement will not merit [...]

Both German orders and the EU Commission's PMI gauges for the EMU show a modest upturn in their recent releases. Both fared slightly better than expected. Both are still significantly weak; the sense of overachievement will not merit a gold star on the forehead. The improvement in these reports is a very minor accomplishment.

Both German orders and the EU Commission's PMI gauges for the EMU show a modest upturn in their recent releases. Both fared slightly better than expected. Both are still significantly weak; the sense of overachievement will not merit a gold star on the forehead. The improvement in these reports is a very minor accomplishment.

Skip right to the 'chase' in the table and peruse the far right column where the rank or 'queue' standings are presented. These rankings position the current observation for each metric in its own queue of data back to January 2015, presenting the result as a percentile standing in that queue of data. The rank position is presented as a top (or 100 percentile) standing as a bottom (zero percentile) standing or as something in between. I am not spoiling the surprise by point out that the readings are uniformly weak. China manufacturing is the only exception (an exception of sorts – more on this later). Readings are uniformly below 50 which in ranking parlance is NOT a boom/bust line as it is for the underlying diffusion survey. Rankings designate the MEDIAN for each series as occurring at a standing of 50%. So every metric in the table, except China, is below its median result since January 2015 – a clear signal of widespread slowing and underperformance.

Spain's composite and manufacturing sectors are on their absolute lows for this period. Eighteen of the series' composite or sector reading or, in several cases both, reside in the lower 15 percentile of their respective queues of data (…or lower). There are 24 rankings in the final column. France has the only three readings at all close to a median reading. China has a reading in its top four percentile for manufacturing (strong enough to boost the composite to a 67th percentile standing despite the services sector's very low 6.9 percentile standing). And Italy has a composite reading just above its 15 percentile with a services ranking in its 39th percentile. China's exceptionally high standing illustrates the danger of using rankings to evaluate queue standings of diffusion data. China's exceptional manufacturing standing of 96.6% is on a diffusion reading of 51.7, the strongest manufacturing reading in the table but still quite modest. For the EMU, a manufacturing PMI of 60 to 61 would have to post to have such a high ranking; for the U.S. about the same. China garners a high standing not because its October reading is so high but because its legacy observations since January 2015 are so weak. The bottom line is that there is serious weakness or underperformance everywhere – that includes China if we step away from a mechanical interpretation of its results.

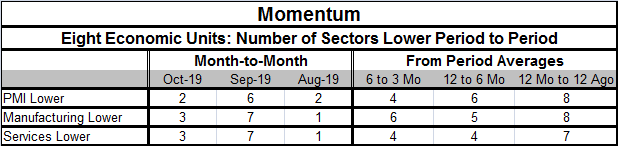

Next there is the issue of momentum...

Next there is the issue of momentum...

This table sums up the momentum situation by presenting summary readings by sector. For one thing monthly momentum is somewhat variable. I caution about using this month's lower count of deterioration by sector as an indication that the erosion is slowing. It may be, but there was also poor breadth of deterioration in August… then September 'happened' (see table). The 12-month average compared to 12-months ago situation shows a substantial weakness as all sectors are lower on that comparison. Broadly speaking, there is erosion everywhere in this sample. Over six months (compare to the 12-month average), there is weakness in the number of sectors that ranges from 4 (half) to six (two-thirds). Over three-months compared to the six-month average, there is the same degree of deterioration ranging from four to six depending on the sector (composite, manufacturing or services).

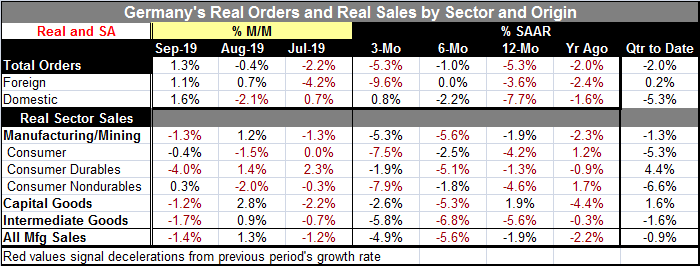

German manufacturing orders

Germany is the largest economy in the EMU; it is the manufacturing leader and it also is the European economy with the most international trade exposure. Having said that, I must also point out that much of its exposure is to trade that is 'international' but also occurs within the EMU under a single currency regime that has no direct currency consequences.

The table below contains data on German (real) orders and real sales trends. German domestic orders show ongoing improvement from 12-months to six-months to three-months, but international orders are not on that same page. German international orders deteriorate over 12 months compared to the year earlier then 'improve' by going flat over six months, but then they fall even faster over three months than they fall over 12 months (annualized, of course).

Monthly data are volatile but this month's readings show increases in total orders, foreign orders and domestic orders. Year-over year declines in real orders are still large ranging from -3.6% to -7.7% by sector. And while domestic orders are showing a three-month rise, that is the sector with the largest year-on-year drop. New orders from inside the euro area fell by 1.8% on the month as orders from outside the euro area rose by 3%.

Meanwhile, German real sales by sector are weak and falling in September with manufacturing sales dropping by 1.4% and declines in consumer goods sales, intermediate goods sales and in capital goods sales.

While the decline in overall orders was not quite as bad as had been expected, there is a great deal of weakness in orders and sales sprinkled across various categories. It is a 'good sign' that there are some sporadic monthly increases being posted and that over three and six months orders can be found to have stabilized or to have expanded. That is what will happen as the bottoming process unfolds and eventually leads to stability and ultimately to expansion. But we are still in the declining phase and these sorts of better-than-expected reports for now only signal that the state of the decline is uneven.

There are still a lot of global problems and every economist/journalists parrots the problem as uncertainty. There is the U.S. trade war with China. There is Brexit. There are still pending U.S. trade negotiation once the U.S. and China finish this round- which still has a ways to go even if phase-one is completed soon. While there is some hidden optimism, there is still a lot of work to do on a number of fronts before we will be able to become reasonably upbeat on growth and trade.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief