Global| Jun 29 2015

Global| Jun 29 2015EMU and EU indices Drop in June

Summary

The EU and EMU indices of overall sentiment fell in June. The EU index fell to 105.5 from 106.4. The EMU index fell to 103.5 from 103.8 in May. Three of five EU indices are still giving net negative signals. Four of five indicators [...]

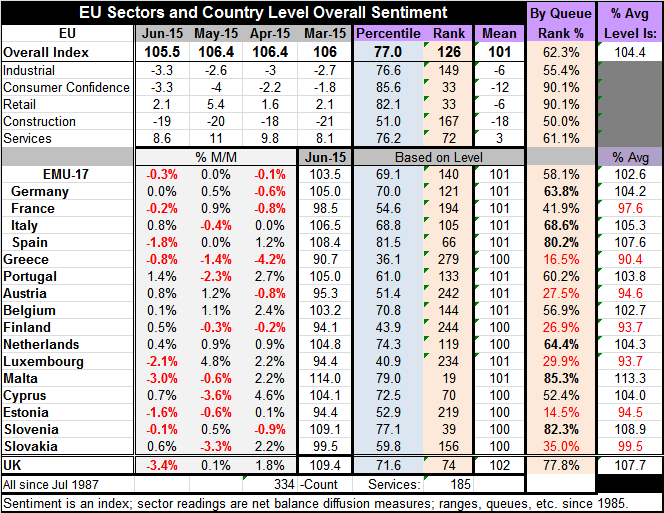

The EU and EMU indices of overall sentiment fell in June. The EU index fell to 105.5 from 106.4. The EMU index fell to 103.5 from 103.8 in May. Three of five EU indices are still giving net negative signals. Four of five indicators fell in June compared to May. The overall EU standing for sentiment is only in its 62nd queue percentile, implying that it is higher 38% of the time. The Industrial index stands only in its 55th percentile. The construction reading is in its 50th percentile. The services index stands in its 61st percentile. The two strong sectors are consumer confidence, which, oddly, against that background, stands in its 90th percentile. Retailing also stands in its 90th percentile.

The EU and EMU indices of overall sentiment fell in June. The EU index fell to 105.5 from 106.4. The EMU index fell to 103.5 from 103.8 in May. Three of five EU indices are still giving net negative signals. Four of five indicators fell in June compared to May. The overall EU standing for sentiment is only in its 62nd queue percentile, implying that it is higher 38% of the time. The Industrial index stands only in its 55th percentile. The construction reading is in its 50th percentile. The services index stands in its 61st percentile. The two strong sectors are consumer confidence, which, oddly, against that background, stands in its 90th percentile. Retailing also stands in its 90th percentile.

The lower part of the table looks at individual EMU members. The big-four economics have very moderate standings except for Spain. Germany has a 63rd percentile standing, France has a 41st percentile standing, Italy has a 68th percentile standing and Spain has an 80th percentile standing.

The bottom of the table chronicles in individual ECB member countries' sentiment standing.

Greece has seen its index slip for four straight months to a standing that is now in its 16th percentile and this, of course, is before the Greek market turmoil at end-June. Apart from Greece, only Malta and Estonia have back-to-back sentiment declines in May and June.

What Greece means

With trouble brewing in Greece, Italy, Spain and Portugal will be the EMU members to watch. Spain already has an active anti-austerity party, Podemos. And Spain is losing momentum. Its sentiment index fell by 1.8 % in June after coming up flat in May. Italy recovered in June, with sentiment rising by 0.8% after a drop of 0.4% in May and a flat April. Portugal looks a bit more solid, with a 2.7% rise in April, a 2.3% drop in May and a 1.4% rise in June. Still, there is not a lot of upward momentum in those countries and room for adverse developments to have a real impact.

At this point, no one knows what will happen in Greece, so addressing the fallout is impossible without a huge dollop of speculation. Here is what seems likely to me: Greece will miss its next debt payment and bankruptcy will be called. The Greek referendum will reject Syriza not the EMU membership. Once the Greek people vote for the deal and for staying in the EMU, Syriza will no longer be the right party for Greece. It can't expect to govern after urging people to reject the EU deal. Thus, a new government will be formed and the EU will bargain with that one and will approve a deal much like the one Tsipras rejected. Greece will stay in the folds of the EU and the EMU.

Of course, there have been a lot of irrational events in Greece. Who can say what will come next? But polls tell us people want to stay in the EMU and the EU and that they would have accepted the EU (Triad) offering. If those straw pools have been accurate, the events I outliner above should come to pass. In the meantime, markets will be under duress and trading will continue to be erratic.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief