Global| Feb 15 2019

Global| Feb 15 2019EMU-16 Trade Flows and Balance

Summary

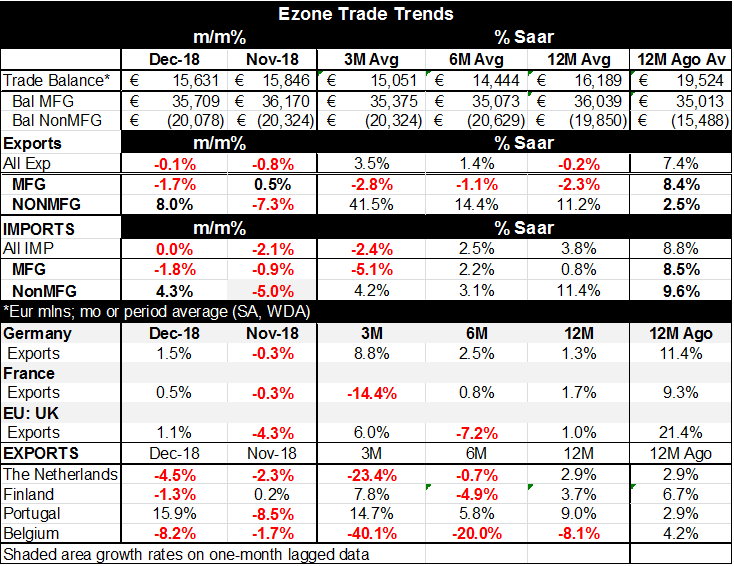

EMU-wide exports ticked lower in December as imports were flat. That combination reduced the trade surplus slightly. Still the surplus in December at €15.6b is now far from its 12-month average of €16.2b but is significantly lower [...]

EMU-wide exports ticked lower in December as imports were flat. That combination reduced the trade surplus slightly. Still the surplus in December at €15.6b is now far from its 12-month average of €16.2b but is significantly lower than its 12-month ago surplus of €22.4b (not shown).

EMU-wide exports ticked lower in December as imports were flat. That combination reduced the trade surplus slightly. Still the surplus in December at €15.6b is now far from its 12-month average of €16.2b but is significantly lower than its 12-month ago surplus of €22.4b (not shown).

Some different and interesting patterns emerge looking at manufacturing and nonmanufacturing trends separately. For trade in manufactures, exports decline over 3-months, 6-months and 12-months. Imports gain over 12-months and six months, then fall sharply over three-months. Judging from imports German domestic demand looks weak. The year-on-year import rise is less than 1% while the annualized 3-month drop is at a pace of -5.5%.

For non-manufactures exports and imports, growth rates are nearly identical over 12-months. But export flows are ramping up while import flows are slowing. Exports of non-manufactures are up at a 41.5% pace over three months annualized compared to 3.5% for non-manufactured imports. The cross trends for non-manufactures are hard to reconcile with the other trends. In particular the growing strength of non-manufactured exports is hard to explain.

The table also shows export trends for a number of EMU and EU members. For the most part exports are moderate to weak. Portugal is the only exception. Apart from Portugal, the strongest year-on-year rise in exports is the 3.7% gain for Finland; remember that these are nominal flows.

International flows are slowing and China is slowing. China’s Consumer inflation gauge went to a pace of 1.7%. In related data today US export and import price were weak with US nonpetroleum imports showing not just weakness but price declines. These declines can’t be signaling much strength in economic conditions abroad generally because prices are so weak.

The US trade negotiating deadline with China is coming up with March 1 as the final day to cut a deal and get in under the wire. But the President, only recently, has been sounding flexible about the date. All of a sudden he has been saying that talks are going well and that the deadline is not fixed. Meanwhile others seem to report that the two sides are still miles apart. It will take time to tell and we may only really know the facts when the deadline draws nearer or has to be extended or alternatively if tariffs are imposed.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief