Global| Feb 23 2009

Global| Feb 23 2009Economists Forecast Moderate Rebound in Second Half

by:Tom Moeller

|in:Economy in Brief

Summary

A survey of 47 top economic forecasters released today indicates that the current U.S. recession should end in the second half of this year. The subsequent recovery would start quite slowly, compared to historic norms, then pick up [...]

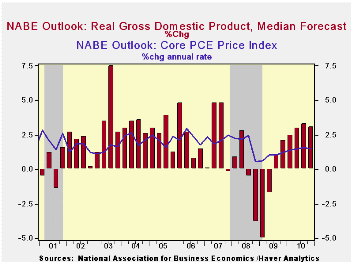

The National Association for Business Economics indicated in its latest survey that positive growth in U.S. GDP would resume in 3Q of this year at a 1.0% rate. For the second half of 2009 as a whole, the average forecasted rate of growth of 1.5% is on a par with the recoveries from the moderate recessions of 1990 and 2001. However, the recovery falls well short of growth after the more severe recessions, such as those in 1960, 1974 and 1982.

Improved (2.2%) growth in personal consumption expenditures and a recovery in residential building are expected to lead the economy from recession. The gains are expected to be moderate, however, compared to sharp rebounds typical of the postwar period. Business investment is expected to continue to decline sharply in 2010.

Corporate profits also are forecasted to rise in 2010 at a 7.3% rate, which would just reverse this year's decline. Again, that rebound is quite moderate compared to prior periods.

Inflation during the forecast period is expected to remain quite tame. Growth in the core PCE chained price index is expected to amount to roughly 1.0% for the rest of this year as the recession continues and the level of excess capacity remains high. The economic recovery next year as well as this year's significant injection of liquidity (money) by the Fed is forecasted to raise prices by 2010 at a quickened rate.

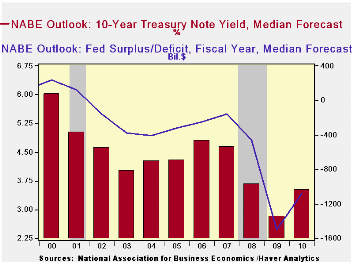

The bond market is forecasted to deteriorate next year with rates on the 10-year treasury rising to an average 3.8% from 3.1% this year. The catalysts for this deterioration are economic improvement as well as a significant rise in the federal budget deficit ($1.5 trillion this year and $1.1 billion in 2010) which could give rise to "crowding out" and higher inflation. In the foreign exchange market, the dollar's value is expected to remain roughly stable.

The forecast figures from the National Association of Business Economists are available in Haver's SURVEYS database.

| Nat'l Assn. of Business Economists | 1Q'09 | 2Q '09 | 3Q '09 | 4Q 09 | 2008 | 2009 | 2010 |

|---|---|---|---|---|---|---|---|

| Real GDP (%) | -5.0 | -1.7 | 1.0 | 2.1 | -0.2 | -0.9 | 3.0 |

| "Core" PCE Chained Price Index (%) | 0.6 | 1.0 | 1.0 | 1.2 | 1.8 | 0.9 | 1.5 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief