Global| Apr 27 2007

Global| Apr 27 2007ECI Wages Jump; Benefits Whimper

Summary

The Employment Cost Index or ECI is a major US inflation survey. The quarterly index came packaged with a surprise: This quarter benefit costs rose by a very thin 0.1% as wages surged ahead by 1.1%. As a result total compensation was [...]

The Employment Cost Index or ECI is a major US inflation survey. The quarterly index came packaged with a surprise: This quarter benefit costs rose by a very thin 0.1% as wages surged ahead by 1.1%. As a result total compensation was held to a gain of 0.8%, less than expected. But as surely as some are worried about that wage rise they are also curious about the small gain in benefits costs.

The story for benefits seems to be due to one particular technical issue related to pension contributions. Firms with defined benefit plans have fiduciary responsibility to keep their pensions funded according to some set rules. Since stocks were so strong, the BLS surmises that many firms simply took the run up in prices as their ‘contribution’ and did not inject new funds into the pension plans. This saving results in lower benefit costs to the firm but does not imply any reduction in benefits given to workers. In that sense it is bogus decline if we think in terms of labor costs. We have seen surging stock prices do this on other occasions in the past. On balance we can throw out the benefit number as a one anomaly.

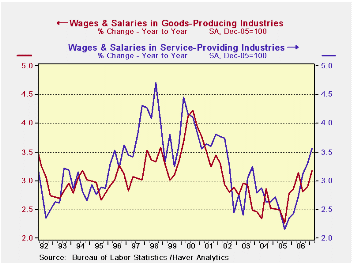

The problems in this report remain as the rise in wages. And despite the hiatus in benefit costs this quarter we expect the Fed to take the wage component as an authentic a signal of tightening labor markets. The chart above shows quite clearly that the pressures are escalating rapidly and that they are strong in both goods ands services, but strongest in services where international competition plays the smallest role.

Services wages are rising at an extremely rapid pace. There are still being outpaced by the employment reports average hourly earnings measure (a poorer index) but that only serves to show there is another, albeit less pure wage measure that is showing the same effect. The Fed has been getting the same feed back in its regional Beige Book canvas. How long can the Fed ignore these signals? On balance I think this report will be sort of chilling from the Fed’s perspective.

The Fed will not be happy over the low growth print for Q1 2007. But there is no denying that wages are rising rapidly and that consumer incomes are growing solidly and the consumer spending is strong and price pressures are still in play. Despite the weak Q1 GDP print I think the Friday reports ( GDP, ECI and U of M final (revised)) put the Fed a half step closer to a rate hike ( yes, HIKE). It will take more information to do it but the Fed must be increasingly nervous about inflation and not so worried about growth after seeing the composition of GDP. Wage pressures, remember, tend to be sticky and longer lasting. These pressures are indeed getting out hand.

Moreover, although hours worked (in the monthly employment report) only rose at a 1.5% pace in Q1 2007 weak GDP will not allow that to become good news for productivity. With GDP advancing by 1.3% there is not much room for productivity growth and that will put the Fed even more on edge about wage pressures becoming cost pressures and leading to price hikes.

| ECI Trends | 07:Q1 | 06:Q4 | 07:Q1 | 06:Q4 | 06:Q1 |

| Civilian | % Q/Q | % Yr/Yr | % Yr/Yr | ||

| Compensations | 0.8 | 0.9 | 3.5 | 3.3 | 2.8 |

| Benefits | 0.1 | 1.1 | 3.1 | 3.6 | 3.4 |

| Wages | 1.1 | 0.7 | 3.6 | 3.2 | 2.5 |

| Private | % Q/Q | % Yr/Yr | % Yr/Yr | ||

| Compensations | 0.6 | 0.8 | 3.1 | 3.2 | 2.6 |

| Benefits | -0.3 | 0.9 | 2.3 | 3.1 | 2.9 |

| Wages | 1.1 | 0.8 | 3.5 | 3.1 | 2.5 |

| Memo: | % Q/Q | % Yr/Yr | % Yr/Yr | ||

| Average Hourly Earnings | 0.9 | 1.0 | 4.1 | 4.1 | 3.5 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief