Global| Jul 12 2013

Global| Jul 12 2013E-Zone IP Dips in May

Summary

Eurozone manufacturing production in May fell by 0.4% after rising by 1% in April. The output of consumer durables fell sharply, by 2.3%, posting a second drop in a row, a drop of 1.9%. Capital goods output fell by 1.5% in May. That [...]

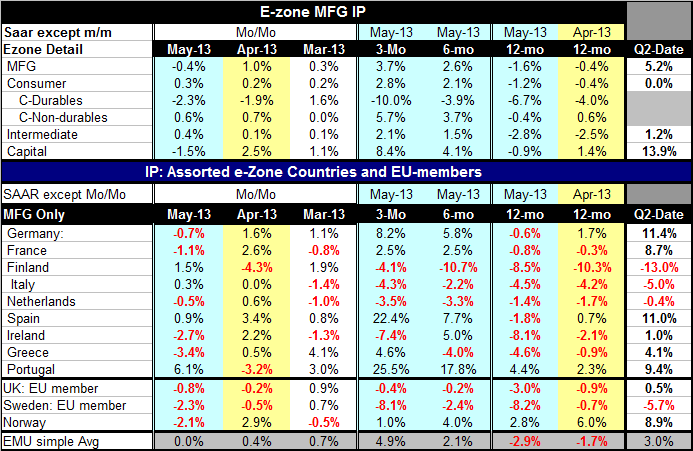

Eurozone manufacturing production in May fell by 0.4% after rising by 1% in April. The output of consumer durables fell sharply, by 2.3%, posting a second drop in a row, a drop of 1.9%. Capital goods output fell by 1.5% in May. That reversed a stronger 2.5% increase in April. Nondurables output rose by 0.6%, rising for the second month in a row. Intermediate goods output accelerated its continuing modest advance rising by 0.4% in May.

Eurozone manufacturing production in May fell by 0.4% after rising by 1% in April. The output of consumer durables fell sharply, by 2.3%, posting a second drop in a row, a drop of 1.9%. Capital goods output fell by 1.5% in May. That reversed a stronger 2.5% increase in April. Nondurables output rose by 0.6%, rising for the second month in a row. Intermediate goods output accelerated its continuing modest advance rising by 0.4% in May.

Despite the setback in May manufacturing output is on an accelerating path. After falling 1.6% over 12 months it is expanding at a 2.6% annual rate over six months and at a 3.7% annual rate over three.

Consumer goods output echoes that trend with a -1.2% drop over 12 months turning to 2.1% gain over six months and a 2.8% gain over three months. This acceleration is despite considerable weakness and accelerating declines from durable goods output which fell 6.7% over 12 months and is falling at a 10% annual rate over three months. To combat that, nondurable goods output is advancing by 5.7% over three months after posting a 3.7% growth rate over six months and after falling by 0.4% over 12 months.

Intermediate goods output has been gradually doing better. After falling by 2.8% over 12 months, it's up at a 1.5% annual rate over six months and at 2.1% annual rate over three months. Capital goods output has shrugged off a 0.9% decline over 12 months to grow at 4.1% pace over six months and 8.4% annual rate over three months.

In the quarter to date, echoing the country level data we've already seen, manufacturing output is up at a 5.2% annual rate in the Eurozone with consumer goods output flat. Intermediate goods output up at a 1.2% annual rate and capital goods output is surging at a 13.9% annual rate.

Production trends in the Eurozone appear to be picking up, but the chart shows how very flat industrial production has been for an extended period of time. The PMI indices from Markit are showing some improvement form weaker levels seen earlier. The indices generally still are indicating weakness in the industrial sector and that weakness is still fairly pervasive throughout the Eurozone.

Finalized data on inflation show some variability within the Zone but it is still well-contained inflation with the HICP over three months growing at just a 1.1% annualized rate compared to 1.6% over 12 months. The ECB has inflation under control and based on data in hand from 9 of the original 11 EMU members, inflation is decelerating year-over-year in about 82% of those countries. However, over the most recent three months compared to six months there has been a pickup in the inflation rate. Inflation is only declining in about one third of these countries.

The ECB which has been trying to stimulate growth in the euro area by walking a tightrope to stay within its mandate, a mandate which is broadly focused on price stability, is beginning to see challenges as international linkages are creating some blowback in European capital markets. The Federal Reserve's perceived move to taper the amount of quantitative easing has had an impact on intermediate and longer-term U.S. Treasury securities yields. Through various international channels higher interest rates in the US are impacting Europe as well, where rates are rising and spreads between two-year and 10 year notes are rising, much to the discontent of the ECB.

The ECB has been trying to use a Federal Reserve-like forward guidance policy and is finding now that it's not very useful in this environment. Markets seem to be a lot more impressed by what US rates are doing now than by a promise from the ECB about what it's going to be doing down the road. The problem with forward guidance has always been a two-fold problem. One is that it's a problem of credibility. Two is that it's a problem of technical competency. That is when central banks use forward guidance the way the Fed and the ECB are doing, we need to have the markets believe that they're going to act the way they say. Moreover, they need to have the markets believe that the main thrust of policy that they describe is the one that they are going to implement.

This is important because forward guidance actually is not a promise. Rather it's a statement about what's likely to happen. Central banks that offer forward guidance right alongside of that guidance admit that if conditions are different from their forecast (guidance) policy will be different.

And that's exactly the problem that is being faced by the ECB right now. As US rates are rising, Europeans are not exactly sure what set of events will be occurring in the future in Europe to accompany the conditions that are expected in United States. It looks as if Europeans are quite reluctant to keep European bond yields low as US bond yields rise. Does that mean that Europeans believe that both the US and Europe will be stronger in the next 6 to 12 months? Do the higher yields on European bonds simply offer some compensation for what's expected to be a weaker euro in the coming months as Europe continues to underperform?

On balance European industrial recovery still seems to be uneven. The region is still beset with a lot of problems and continues to be beholden to the German election schedule before it will be able to take any significant action on any important front. The rising rates in the US have put the ECB in a difficult spot. The ECB has a different mandate from the Fed and has different restrictions on what it can do. Its guidance on QE is not as powerful as the Fed's for that reason. In all likelihood the game is up for the ECB which will now be a spectator as financial markets react to the new policy in the US.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief