Global| Apr 26 2013

Global| Apr 26 2013e-Zone Credit Contracts: Has Monetary Policy Met its Match?

Summary

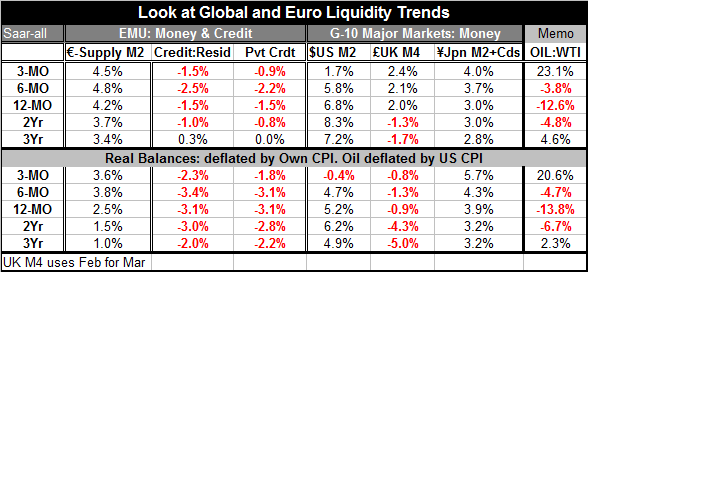

Euro-Zone money supply growth has steadied in the 4% to 5% range, slightly above its pace in the previous couple of years. Real money balances are rising a bit faster too in the range of 2.5% to almost 4%, up from one to one-point [...]

Euro-Zone money supply growth has steadied in the 4% to 5% range, slightly above its pace in the previous couple of years. Real money balances are rising a bit faster too in the range of 2.5% to almost 4%, up from one to one-point five percent growth in earlier years. Still Credit growth is AS WEAK AS EVER and mostly weaker. There is no pick up in nominal credit growth in the Zone, in fact evidence shows it is decelerating faster. In real terms credit growth is about as weak as it been. .

Euro-Zone money supply growth has steadied in the 4% to 5% range, slightly above its pace in the previous couple of years. Real money balances are rising a bit faster too in the range of 2.5% to almost 4%, up from one to one-point five percent growth in earlier years. Still Credit growth is AS WEAK AS EVER and mostly weaker. There is no pick up in nominal credit growth in the Zone, in fact evidence shows it is decelerating faster. In real terms credit growth is about as weak as it been. .

The chart shows the divergence in money and credit growth in the Eurozone. We can see that money supply growth seems to have picked up but then hit a plateau early this year in terms of its rate of growth. Credit growth to the private sector reached a peak in 2011 and has steadily been decelerating. All of the actions by the ECB to provide LTRO loans to banks in the Eurozone have not been able to generate net credit growth in the private sector. Austerity continues to be the law of the land in the Eurozone although the strategy is increasingly coming under some pressure.

Jose Manuel Barroso, a former prime minister Portugal, the President of the European Commission man who in the past applauded austerity even as it was applied to his country, Portugal. But recently Mr Barroso has been suggesting that perhaps austerity has done all that it can do. The black eye received by European Community over its treatment of Cyprus is once again put austerity in the limelight. Italy's public increasingly has endorsed candidates that oppose austerity and some who seek a vote on whether Italy should separate itself from the European monetary union.

The recent upheaval over the error in the book 'This Time It's Different,' is certainly put the strategy of austerity back in the spotlight and in more unfavorable terms.

Around the world stimulative monetary policy has failed to be successful. It has failed to spur credit growth. It has failed to spur domestic demand. The one place that that may be changing is in Japan where although monetary growth has not been stimulated the exchange rate has been pushed down and of course with that demand is affected because a lower exchange rate can increase foreign demand for your product. But that strategy is not available to every country and in fact for that reason it's a dangerous strategy.

In many ways monetary policy seems to have reached its own endgame. It's becoming clearer that what the world has is an excess of supply and insufficient demand. And monetary policy cannot bridge that gap. But in places like the European monetary union where there is no centralized fiscal authority and where member economies are already deeply in debt, the burden falls on the shoulders of the monetary authority. In the United States where Congress can't get out of its own way to make a decision, the burden falls to monetary policy. Japan's monetary policy has produced a result that is particularly successful but unavailable to most countries and probably a remedy that was more needed in Japan than in most places because Japan's exchange rate had become so very overvalued.

The striking disconnect between money and credit in the Eurozone hopefully will alert the authorities that they needed a plan- a NEW plan. However, Angela Merkel in Germany is still pursuing her own reelection. It's unclear whether any EMU members will be cut any slack in this situation. Spain apparently is looking for more leeway in its program. Spain may turn out to be a test case of whether Europe will remain rigid or become more flexible. Italy will be a different sort of test case and Europe is holding its breath over that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief