Global| Aug 09 2018

Global| Aug 09 2018Dutch IP Falls in June

Summary

Dutch industrial production declined by 1.1% in June as utilities output fell by 2.2%, mining & quarrying activity plunged by 12%, and manufacturing edged lower by 0.1%. With the quarter’s data completed, the Dutch economy now shows [...]

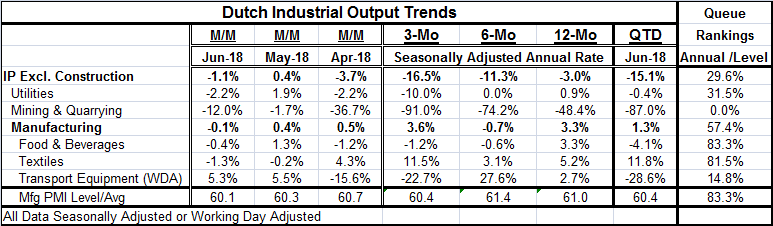

Dutch industrial production declined by 1.1% in June as utilities output fell by 2.2%, mining & quarrying activity plunged by 12%, and manufacturing edged lower by 0.1%.

Dutch industrial production declined by 1.1% in June as utilities output fell by 2.2%, mining & quarrying activity plunged by 12%, and manufacturing edged lower by 0.1%.

With the quarter’s data completed, the Dutch economy now shows IP excluding construction falling at 15.1% annual rate in Q2. Utilities output is lower at a thin -0.4% pace. Mining & quarrying output is contracting at an 87% annualized rate, but manufacturing is making headway with output growing at a 1.3% annualized rate.

The PMI data underscore the fact that despite weakness elsewhere in the industrial portion of the economy, manufacturing is still doing quite well.

Overall IP (excluding construction) has a 29th percentile standing in its queue of 12-month growth rates back to January 2014. The utilities sector has a 31st percentile standing. Mining & quarrying is on its weakest annual growth of that entire period. But manufacturing output with annual growth at 3.3% has a 57.4 percentile standing. Manufacturing shows relative strength in food & beverages as well as textiles with each sector ranking in its 80% decile on the period. But transportation equipment is in a down-phase, logging a very weak 14.8 percentile standing.

The manufacturing PMI values have been steadily above the level of 60 in diffusion terms although there is some weakening in this profile in June as well as over the past three months on average. Still, the diffusion value of ‘60’ generally is a high diffusion reading for a manufacturing series. For the Netherlands, the 60.1 diffusion reading in June has an 83.3 percentile standing among all readings since January 2014.

The Dutch diffusion reading for manufacturing is relatively stronger than the year-on-year manufacturing IP gain as manufacturing has a queue ranking only in its 57th percentile and the PMI standing is in its 83rd percentile. While the chart seems to show that both series have moved together over this period, note that the PMI and the IP-gain series are at more or less the same position on the chart in July whereas historically the manufacturing line has been higher. That is a way to optically observe the relative differences that are captured by the statistics. But note that the absolute placement of the axes is ‘arbitrary’ and only serves to illustrate the common movements in the two series.

The Dutch diffusion reading for manufacturing is relatively stronger than the year-on-year manufacturing IP gain as manufacturing has a queue ranking only in its 57th percentile and the PMI standing is in its 83rd percentile. While the chart seems to show that both series have moved together over this period, note that the PMI and the IP-gain series are at more or less the same position on the chart in July whereas historically the manufacturing line has been higher. That is a way to optically observe the relative differences that are captured by the statistics. But note that the absolute placement of the axes is ‘arbitrary’ and only serves to illustrate the common movements in the two series.

In the Dutch case, it does not seem as though the PMI is a leading barometer of change. The PMI in fact can only explain about 39% of the variance in the year-on-year IP change. And the correlation between the two series when the PMI is used with a lead actually falls. The best PMI-to-IP relationship for the Netherlands is coincident.

In the Dutch case, the PMI does not see to provide that much extra information compared to the manufacturing PMI itself, but for now they are both giving the same signal and the PMI that has a one-month fresher observation shows that weakening continues into July. The theme of weakening data has been persistent throughout various Europe statistics and has begun to appear in Japan as well as in the United States.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief