Global| Sep 09 2020

Global| Sep 09 2020Dutch IP Continues to Claw-Back Lost Ground As Covid-19 Strikes Again

Summary

Dutch PMI and manufacturing IP are in lock-step Dutch production continued its rebound in July, rising by 1.7% (excluding construction) after a 0.6% gain in June. This two month ‘string’ of increases goes only part way to effect a [...]

Dutch PMI and manufacturing IP are in lock-step

Dutch PMI and manufacturing IP are in lock-step

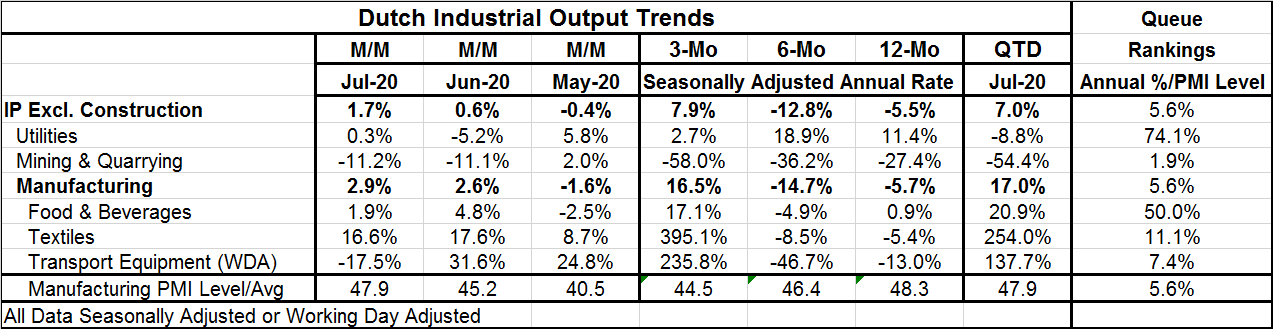

Dutch production continued its rebound in July, rising by 1.7% (excluding construction) after a 0.6% gain in June. This two month ‘string’ of increases goes only part way to effect a recovery from what were four straight months of output declines on the same measure. Output is still some 6.7% lower than its level in January.

Utilities output rose in July after a one-month decline. Mining and quarrying output fell sharply for the second month in a row.

Manufacturing rebounds

Meanwhile, manufacturing output rose briskly for the second month in a row as its July rise of 2.9% exceeded its June gain of 2.6%. Manufacturing output’s two-month run also provides respite from a four-month string of declines from February through May. The two-month rebound helps to mitigate what had been a cumulative drop in IP of 12.6% since January. The current drop in IP since January has been reduced to 6.7% and has been nearly halved.

The path of IP

The virus struck in the early months of the year and policy responses to it caused a large ongoing contraction in economic activity, including a sharp setback to output. As a result of that timing, IP is now recovering, but the sequential growth rates are still muddled with declines over 12 months, a sharp rate of decline over six months and now a strong gain coming out of a deep hole over three months. Mining and quarrying is the exception to this pattern as that sector shows an accelerating drop from 12-months to six-months to three-months.

The quarter ahead

Today’s report is for July, the first month in the quarter. As a result of having back-to-back gains after a smallish drop in the last of a four-month string of declines, output is now ramping up in Q3 at a 7% annualized rate overall and at a more robust 17% annualized rate for manufacturing. All sectors show strong growth rates early in Q3 except mining and quarrying where output is falling at 54.4% annual rate.

The upside after a severe downside

But these strong growth rates are the upside after a severe downside that is testified to by the collection of sector growth rates over 12 months that finds four of six of them still showing substantial declines. Utilities and food & beverages are the two sectors that display 12-month output increases; that is not very surprising as they are sectors of steady demand.

Weak growth in transition to strength

The 12-month growth rates ranked in historic context show a 5.6 percentile standing overall (12-month output growth has been weaker than this only about 5.6% of the time). That is the ranking for overall output as well as for manufacturing output as well as for the manufacturing PMI. Utilities with 11.4% growth over 12 months show a 74.1 percentile standing. Food & beverages, with just under one-percent growth over 12 months, have a 50% queue ranking for that growth rate. Mining and quarrying have the weakest standing at 1.9 percentile while textiles log an 11.1 percentile standing and transportation a 7.4 percentile standing. But those latter two ranking are likely to change a lot in the coming month if they can hold momentum since the quarter-to-date rates of growth are in triple digits!

Covid-19: impact and timing

We see in the Netherlands manufacturing sector a lot of similarities to output trends in other countries as the virus hit most economies more or less at the same way. Infection rates vary and the length of shutdowns varies and certainly the impact of the virus on the various economies has varied, but the timing of the virus strike is among the things all countries have more or less in common. The question now is the period ahead since reinfections have begun to occur and they are affecting countries in very different ways and to different degrees. The Dutch saw a slowing and rather stable incidence of new infections in May and June, but in July that began to rise and it has stayed high in August with continuing outbreaks. However, deaths from Covid-19 have remained low.

Covid-19 vs. growth

In the Netherlands the presence of covid-19 has led to a speeding up of the ban on mink farming because it has been determined that mink can catch covid-19 and pass it on to humans (source). Moreover, Covid-19 cases have just spiked to 1140 (source), the most since April putting the Dutch economy back behind the eight-ball. The increase was not tied to the reopening of primary schools across the country over the past three weeks. However, reinfection whatever the cause, does pose a challenge to the way ahead for the Dutch economy. Once again, we see how it is the virus that keeps flaring up and constricting economic growth rendering economic trends meaningless.

Conversely, after all the criticism, Sweden has faced for its no-lockdown approach we now see this… Sweden carried out a record number of new coronavirus tests last week with only 1.2% coming back positive. The health agency said on Tuesday that this is the lowest rate of infection detected since the pandemic began and it comes at a time when countries across Europe are seeing surges in infections (source). Read here for a discussion of what Sweden has done and why it has worked. Europe appears to be back in the viral soup. The Netherlands is part of that broth. Meanwhile, across the Atlantic in the U.S., different states face different circumstances and with politics in full swing it is hard to get an objective read on what is really going on there.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief