Global| Jul 15 2015

Global| Jul 15 2015Dutch Exports Sag As Imports Gain Purchase

Summary

The Netherlands is another case of an EMU country where the trade picture belies the weakness in the euro exchange rate. While exports and imports do not respond wholly to the same set of variables, they are both affected by the [...]

The Netherlands is another case of an EMU country where the trade picture belies the weakness in the euro exchange rate. While exports and imports do not respond wholly to the same set of variables, they are both affected by the exchange rate. With the euro having fallen so much, we would have expected to have seen strong Dutch exports and weaker Dutch imports. The weak euro should improve competitiveness in the Netherlands and cause exports to surge and imports to slow. But that is not what we are observing. Other factors are trumping the euro exchange rate effect.

The Netherlands is another case of an EMU country where the trade picture belies the weakness in the euro exchange rate. While exports and imports do not respond wholly to the same set of variables, they are both affected by the exchange rate. With the euro having fallen so much, we would have expected to have seen strong Dutch exports and weaker Dutch imports. The weak euro should improve competitiveness in the Netherlands and cause exports to surge and imports to slow. But that is not what we are observing. Other factors are trumping the euro exchange rate effect.

Of course, one of the big factors countermanding the expected trends is the importance of oil to the Dutch economy and the weak global oil price. But none of that explains the strength in Dutch imports or in foods imports or machinery imports.

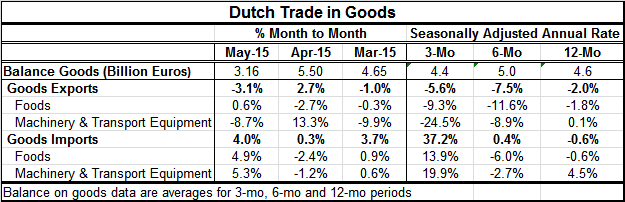

The export and import patterns in the chart help to explain these things. They show how weak energy prices hit both exports and imports early in the year. Now these flows are coming back on stream with imports reviving faster after falling faster and exports lagging, but no longer worsening their pace at least on the year-over-year data. Unfortunately, the patterns within the last 12 months do indicate some further deterioration of export momentum. And oil prices, of course, are still weak and possibly weakening further on global markets in the wake of a proposed nuclear deal with Iran that could free up some additional oil to world markets.

The Netherlands is an important port country for shipments out of Europe. It benefits generally from a pick-up in European trade. The oil sector is also very important to the Netherlands. And of course, as an EMU member, the events in Greece are a substantial concern to the Dutch whose finance minister has been playing a key role in the negotiations. The Dutch economy is just another example of an economy in the EMU that is still struggling although making its way with growth as it tries to avoid the many shocks in the global economy.

Events in Greece are still fluid. The Greek PM is still trying to round up support for the package he negotiated although he makes no bones about the fact that the deal was forced upon him. That makes him a rather poor salesman of the product. On the other side, Europe is having a hard time deciding where to get its bridge loan funds that it has promised Greece.

This whole Greek negotiating process has really become a circus. There is no telling what happens next. None of this is good for the business environment in Europe, and the Dutch economy, like others, is simply caught in the rip tides of events. The chaos is undercutting the euro and improving the euro area's competiveness elsewhere in the world. As you can see for the Netherlands, however, that has not carried the day for growth. Much of EMU member countries' foreign trade is occurring within the single currency area where a weaker euro exchange rate has no impact. But the chaos caused by the negotiations with Greece has had an impact and it has not been positive.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief