Global| Jan 29 2002

Global| Jan 29 2002Durable Goods Orders Firm

by:Tom Moeller

|in:Economy in Brief

Summary

Durable goods orders rose a bit more than expected last month, but it was off a November level that was revised sharply lower due to lowered figures in the transportation sector. Excluding transportation, durable orders rose 1.4% [...]

Durable goods orders rose a bit more than expected last month, but it was off a November level that was revised sharply lower due to lowered figures in the transportation sector.

Excluding transportation, durable orders rose 1.4% after rising 0.7% (revised slightly lower) in November.

The sharp improvement in the ISM orders component bodes well for further improvement in durable goods orders. The five-year correlation between this index and the month-to-month change in durable orders ex. transportation is a significant 19%, but it rises to 28% when orders are lagged one month.

Orders for nondefense capital goods rose for the third consecutive month led by the third monthly gain in the computers and electronics category (mostly semiconductors).

Shipments rose slightly, but excluding transportation have yet to show meaningful improvement, down in all but two months of 2001.

| NAICS Classification | Dec | Nov | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Durable Goods Orders | 2.0% | -6.0% | -14.0% | -12.8% | 6.6% | 6.0% |

| Nondefense Capital Goods | 1.3% | 4.0% | -26.7% | -17.0% | 14.4% | 3.5% |

by Tom Moeller January 29, 2002

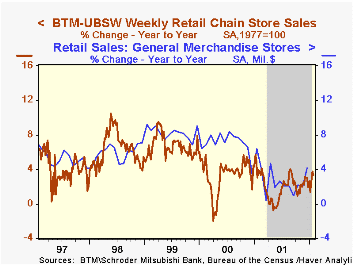

Chain store sales rose 0.2% in the last full week of January. Sales have risen in five of the last six weeks.

For the first four weeks of January sales were up 2.2% versus December.

During the last five years there has been a 26% correlation between the month-to-month percent change in chain store sales and the change in retail sales at general merchandise stores.

| BTM-UBSW (SA, 1977=100) | 1/26/02 | 1/19/02 | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Total Weekly Retail Chain Store Sales | 401.0 | 400.0 | 3.4% | 2.1% | 3.4% | 6.7% |

by Tom Moeller January 29, 2002

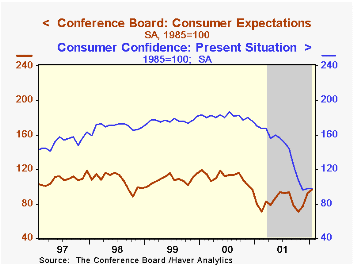

The Conference Board’s Index of Consumer Confidence rose slightly more than expected in January. December's level was revised up.

The rise in the Conference Board measure was in-line with the mid-month University of Michigan reading that consumer sentiment had improved.

The rise in confidence reflected a sharply higher reading for consumer expectations. Confidence regarding the present situation was unchanged. A rise in expectations also powered the Michigan index.

The Conference Board's survey is conducted by a mailed questionnaire to 5,000 households and about 3,500 typically respond.

| Conference Board | Jan '02 | Dec '01 | Y/Y | 2001 | 2000 | 1999 |

|---|---|---|---|---|---|---|

| Consumer Confidence | 97.3 | 94.6 | -15.9% | 106.6 | 139.0 | 135.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief