Global| Mar 18 2016

Global| Mar 18 2016Drink the German Kool-Aid; Take the German Medicine; German PPI Continues Its Wayward Path Along with the CPI

Summary

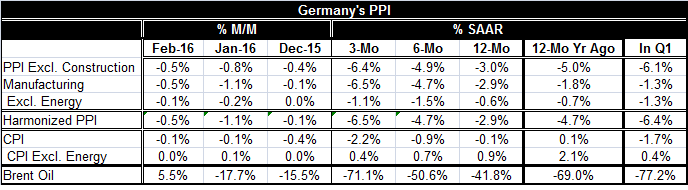

Germany's PPI fell in February and it has been falling with great persistence. There have been 10 month-to-month declines in the PPI in the last 12 months and it has been 13 months since the German PPI has increased month-to-month at [...]

Germany's PPI fell in February and it has been falling with great persistence. There have been 10 month-to-month declines in the PPI in the last 12 months and it has been 13 months since the German PPI has increased month-to-month at all. The uninterrupted string of year-on-year PPI declines extends back to August 2013. The last year-over-year German PPI rise was in March 2013; that's three years ago.

Germany's PPI fell in February and it has been falling with great persistence. There have been 10 month-to-month declines in the PPI in the last 12 months and it has been 13 months since the German PPI has increased month-to-month at all. The uninterrupted string of year-on-year PPI declines extends back to August 2013. The last year-over-year German PPI rise was in March 2013; that's three years ago.

And the German people and the Bundesbank are just fine with this. At the same time, the CPI and EMU-targeted HICP have been weak. And the German people and the Bundesbank have been fine with this too. The undershooting of the overall EMU-wide HICP is also just fine, despite the fact that the ECB targets an inflation rate just below 2%.

Compare and contrast U.S. vs. German monetary policy outcome concerns

In the U.S., St Louis Fed President James Bullard has been concerned that a lengthy stay of inflation below target will harm Fed credibility. In Germany, such concerns are as peculiar as a visitor from an extraterrestrial. To Germans, inflation credibility is keeping inflation at or below the target all the time under almost any circumstance; there is no symmetry around the policy rate target. But to most of the rest of Europe, the target is what matters. In the U.S., again it is Bullard noting that there is evidence that inflation expectations have fallen and concerned that such expectations can make it harder for the central bank to reach its inflation goal. For the record, even in the U.S., Janet Yellen and the `rest of the Fed' have tried to downplay this and have referred to market `forecasts' of inflation embedded in the market rate structures as `inflation compensation' rather than as `inflation expectations.' In Europe, there seems to be no concern about inflation expectations being damaged by what inflation is now doing. Indeed, policy split has developed with the Bundesbank and the other German policymakers having done all they could to slow any out-of-the-ordinary moves that the ECB has tried to boost inflation back toward target. While the Germans lost most of these battles, they managed to slow down ECB moves so that ECB stimulus has been largely ineffective when brought on-stream. In both the U.S. and the U.K. where QE programs were effective, at least for a while, it was quick implementation in the early stages where QE worked best. The ECB did not learn the lesson.

Has money supply or credit revived as the ECB has acted?

Has money supply or credit revived as the ECB has acted?

As the German PPI and CPI remain listless and as the EMU-wide HICP remains woefully under-target, the EMU-wide money and credit performance is lagging despite what have been several rounds of attempted special stimulus. The ECB now claims that negative rates are helpful; however, as you can see, there is nothing there in the data through February, at least not yet. Money and credit both have rolled over rather sharply; successive ECB programs have failed or worse.

Is low German inflation now the enemy because of internal EMU dynamics?

The performance of PPI and CPI/HICP inflation particularly in Germany, the core EMU economy, and the one with the largest weightings for EMU data, certainly overshadows the overall EMU performance for any variable. And the lower that German inflation is, the lower than inflation must stay in other EMU nations lest they lose ground competitively to Germany. When the financial crisis hit, it was the countries that had inflated the most relative to Germany that were hurt most (and they continue to struggle). They were forced into programs of austerity. If you drink the German Kool-Aid, you must also take the German medicine when things go bad. The program is all about tight money, low or lower inflation, and fiscal responsibility at all points of the business cycle. Keynes is dead in Germany.

Fiscal policy in never-never-land

Germany is very serious about enforcing Maastricht budget rules and this is the reason for widespread austerity programs. Until the migrant crisis hit, Germany itself was preparing to run budget surpluses further depressing growth in Germany and bolstering its position of fiscal superiority in the EMU. Under these rules now projected onto the EMU, the monetary tool is blunted. The fiscal tool-case is shuttered.

ECB could do more damage?

Still, the ECB chief economist, Peter Praet, was cheerily telling us today that the ECB could cut rates more. But clearly the Germans remain in opposition. Perhaps the most important thing about a monetary policy move is now missing...that there can be more than one. It is the expectation of a path of change that most powerfully moves markets. The ECB cannot do that. If it even has multiple options, they each will be fought over one by one and played out separately, sequentially, and with minimum impact because of ECB politics (largely German opposition). We can see the impact of the notion of a changed policy path in what just happened with the Fed in the U.S. (March FOMC meeting). The Fed's sidestep took not just a current hike, but prospective rate hikes, off the table with profound economic impact on the markets and on the dollar in particular. This is an option that the ECB simply does not have. It is why monetary policy in Europe is ineffective and impotent. The path is shut.

Nowhere bank please listen!

For those reasons the ECB should stop with this crazy stimulus. Further policy manipulation will only weaken its fiduciary standing and further divide the ECB board. It probably will not help the economy much either since when policies get too extraordinary or fanciful their economic impact often is swamped by the common-man-in-the-street's concern about what is really going on. Raising anxiety is counterproductive. In effect the German's have `won' if you call this winning. And Europe's economy will suffer all the more with few options for revival. While other economists have been gushing over the ECB's last move I see it, as described above, as too fanciful, too little, too late and with too little follow-up to have much impact. Europe is now effectively adrift with no policy rudder even if the ECB takes further steps because they will lead nowhere.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief