Global| Feb 19 2010

Global| Feb 19 2010Disturbing Mixed Message From The Markit PMIs In EMU

Summary

The Markit PMIs are sensitive gauges measuring the breadth of the expansion in manufacturing and services industries in the e-Zone. This month the MFG PMI was above its neutral reading of 50 for the fifth month in a row. In each of [...]

The Markit

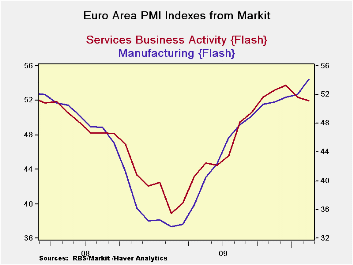

PMIs are sensitive gauges measuring the breadth of the expansion in

manufacturing and services industries in the e-Zone. This month the MFG

PMI was above its neutral reading of 50 for the fifth month in a row.

In each of these five months MFG has accelerated improving its mark

above the neutral 50 readings.

The Markit

PMIs are sensitive gauges measuring the breadth of the expansion in

manufacturing and services industries in the e-Zone. This month the MFG

PMI was above its neutral reading of 50 for the fifth month in a row.

In each of these five months MFG has accelerated improving its mark

above the neutral 50 readings.

Not so for services.

For the services, the index was also above 50 – and for the sixth consecutive month. But the services gauge has now fallen for two months in a row. It is not building momentum, it is losing momentum. The services reading at 51.97 is now the weakest reading for this sector since September 2009 when it first popped above the neutral 50 mark and began to signal growth. Since this sector is the job-creating sector, backtracking in services is very worrisome.

True, the services sector still is expanding. At 51.97 it stands above the neutral mark of 50. But momentum is being lost and the margin above 50 for services is small. The services reading is below its lifetime average of 53.67 so it is far below normal even though the sector it technically still registering growth. Growth does not imply normalcy.

Compare that to the manufacturing index which at 54.13 has been steadily accelerating and stands above its lifetime average reading of 51.12. Manufacturing seems to be pointing the way ahead.

But from other reports we know that one of the problems in the Zone is that it has benefitted from export led growth, and that has favored the manufacturing sector. It’s a problem because the very name suggests that the Zone has not cultivated its own domestic demand. And we see that loud and clear in this report. While some services do get exported, goods are far more likely to be exported than are services. The strength in manufacturing stems from some considerable strength in Euro-Area export orders. Meanwhile, the weakness at home has held back domestic demand. Just today the UK (an EU member not an EMU member) posted a sharp drop in retail sales, although weather seems to have been a prime culprit there. The overriding point for Europe is that it has not cultivated domestic demand; it is living off of demand rebounds elsewhere. And Europe is too big to be carried for long in that fashion by the global economy.

The weakness in its own services sector reasonably leads us to wonder if Europe’s export growth will be enough to sustain it until job growth, the services sector and domestic demand- three highly inter-linked factors - kick into gear.

Suffice it to say that Europe’s report is not reassuring and its growth seems to be as much at risk as at anytime in this nascent expansion period.

| FLASH Readings | ||

|---|---|---|

| Markit PMIs for the Euro-Area | ||

| MFG | Services | |

| Feb-10 | 54.13 | 51.97 |

| Jan-10 | 52.39 | 52.50 |

| Dec-09 | 51.59 | 53.63 |

| Nov-10 | 51.20 | 53.04 |

| Segment Averages | ||

| 3-Mo | 51.73 | 52.67 |

| 6-MO | 50.57 | 52.36 |

| 12-Mo | 44.78 | 48.47 |

| 136-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.55 | 39.24 |

| % Range | 76.4% | 55.1% |

| Range | 26.92 | 23.12 |

| Q3-2007 | 51.12 | 53.67 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief