Global| Oct 14 2009

Global| Oct 14 2009DIHK Survey Points to Continued Improvement in German Economy

Summary

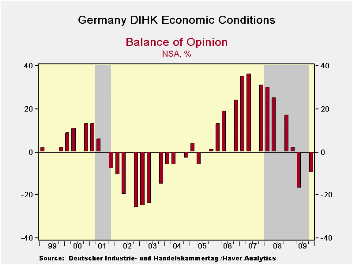

The DIHK survey, a poling of over 25000 firms by the German chambers of industry and commerce, is not conducted in Q3. So the fourth quarter’s -10 reading compares to the -17 reading from Q2. It is a net balance of opinion diffusion [...]

The DIHK survey, a poling of over 25000 firms by the German

chambers of industry and commerce, is not conducted in Q3. So the

fourth quarter’s -10 reading compares to the -17 reading from Q2. It is

a net balance of opinion diffusion index. A strong improvement in

existing conditions is indicated, but declines persist. DIHK itself

pointed to the role in temporary government stimulus in boosting the

survey and muted its optimism with expectations for more modest

improvements in the index for the quarter ahead

The index has climbed up from the 14th percentile of its range

in 2009-Q2 to stand in the 25th percentile in Q4. Business expectations

are sharply higher at a raw reading of zero up from -27 in Q2. The

range standing for that reading is up to a respectable 58th percent of

the range from a low 13th percentile in Q2. Export expectations are up

even more strongly to a raw reading of +7 from a Q2 reading of -37,

pushing the percentile standing up to its 55th percentile from 1.3% in

2009 Q2. These sorts of progressions are in line with much of the data

that have been reported that have showed foreign orders to be picking

up, although some recent German export figures were more disappointing;

that slowdown is not corroborated here.

As to investment, the Q2 percentile standing was the worst in

the history of the survey, a history that extends back to Q4 1991. The

improved standing to a still-weak 27th percentile on a raw reading of

-17 nonetheless is sharply up from -30 in Q2. Still we can see that

investment demands are lagging. Hiring intentions occupy a sort of

middle ground at a raw reading of -15; conditions are much improved

from Q2’s reading at -25. Still more cutting is indicated. The

percentile standing has been boosted to its 38th percentile, but that

is still weak. Clearly much more improvement will bee needed to stoke

job growth and just to keep the prospect of more cuts at bay.

| DIHK-Balance of Economic Opinion | ||||||||

|---|---|---|---|---|---|---|---|---|

| Net Balance Readings | Change | Range Q4'91 | Percentile | |||||

| Q4-09 | Q2-09 | Q1-09 | Yr Ago | 2-Yr | 3-Yr | Q4-09 | Q2-09 | |

| Economic Conditions | -10 | -17 | 2 | -27 | -41 | -34 | 25.8 | 14.5 |

| Business Expectations | 0 | -27 | -35 | 7 | -15 | -10 | 58.3 | 13.3 |

| Export Expectations | 7 | -34 | -35 | -6 | -30 | -27 | 55.3 | 1.3 |

| Investment Intentions | -17 | -30 | -23 | -15 | -31 | -23 | 27.7 | 0.0 |

| Hiring Intentions | -15 | -25 | -20 | -13 | -24 | -15 | 38.3 | 17.0 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief