Global| Oct 30 2019

Global| Oct 30 2019Deterioration Continues to Sweep Through the Euro Area

Summary

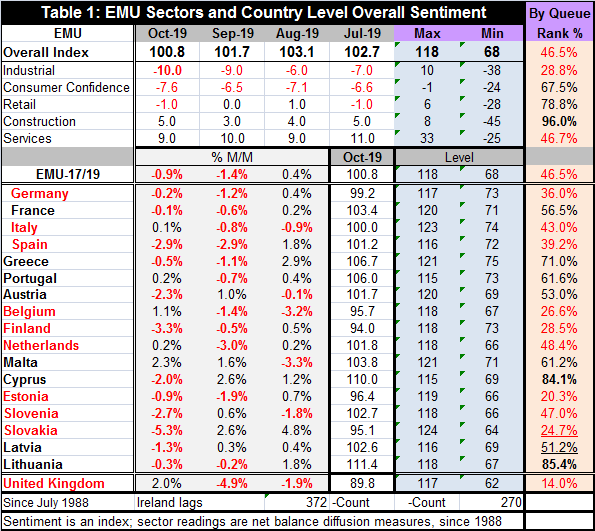

The EMU overall Index fell to 100.8 in October, its weakest level since January 2015, from 101.7 in September. Ireland and Luxembourg have not reported; Table 1 reflects reporting from 17 of 19 EMU members. Of these 19, all but five [...]

The EMU overall Index fell to 100.8 in October, its weakest level since January 2015, from 101.7 in September. Ireland and Luxembourg have not reported; Table 1 reflects reporting from 17 of 19 EMU members. Of these 19, all but five (Italy, Portugal, Belgium, the Netherlands, and Malta) saw their readings drop in October. This is similar to September when all but six of countries in this group saw declines. However, in August only five countries saw declines with the large majority increasing on the month. Only 42% of reporters have higher readings on balance over three months. Over 12 months, all but three countries are weaker; over six months only four are stronger (Slovakia, Malta, Greece, and France); Italy is unchanged.

Country conditions

The percentile standings show the EMU as a whole with a rank standing at 46.5% (this compares to a simple average ranking of the 17 reporters of 49.3%). The weaker number for the EMU weighted reading reflects the fact that the larger countries are weaker than the smaller countries. However, a perusal of the reading shows a substantial divergence and some special stories. For example, Greece has a high ranking substantially because it has been so much weaker when under austerity. Also, among the four largest EMU members, France has the strongest standing and it is the only one in this group with a reading above its median (median occurs at a ranking of 50%; France is at 56.5%).

Among the four largest EMU countries, France and Italy have the highest rank standings and they also are currently in violation of EU budget rules. The EU has challenged France and France has agreed that it will respect the budget deficit constraint for next year. Germany, with the weak reading among the four largest EMU nations, is running a fiscal surplus. Its weak economic performance reflects that.

Only eight countries (identified with black labeling in the table stub) have rank standings above their respective medians. It is easy to assess the euro area as a region that is weakened and that continues to weaken. The result is clear and broad-based.

Sector conditions

Weakness can also be seen in the EMU sector rankings; the overall EMU reading at 46.5% is dragged below its median by weakness in its two key sectors industrial and services. The services sector ranks at its 46.7 percentile while industry has tanked with a very weak 28.8 percentile standing. Consumer confidence has a firmer standing at its 67.5 percentile and retailing is better still at its 78.8 percentile. Only construction is truly strong with a 96th percentile standing. This index is this strong or stronger only 4% of the time. In addition, all sectors weakened month-to-month in October except construction. Over three months there is net weakening in the industrial sector in consumer confidence and for services while construction and retailing are unchanged. Looked at by sector, there appears to be a slightly better case to be made for resiliency. However, the sectors that are the strongest (retailing and construction) are the sectors with the lowest correlation to the headline index. The highest correlation is from services followed by industry followed by consumer confidence.

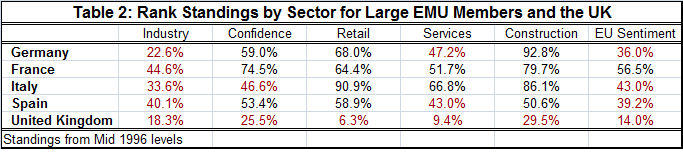

Table 2 digs down into the details a bit more and presents rankings of sectors by country. Those measures rank each sector in each country against its own history expressing the standing as a percentile standing metric. Several things stand out in this table.

• Industry is weak and it well-below its median ranking (50%) for all countries in the table, EMU member or not. Germany, the most trade-dependent member in the EMU, is hit the hardest, but the still-in-EU member, the U.K., is hit even harder as the run up to Brexit is taking a toll.

• Retailing and construction have above median rankings in all EMU member countries.

• Consumer confidence is below its median only in Italy among EMU members.

• Services show a great deal of variation. The sector is weakest in Spain, below its median in Germany just above its median in France and yet quite firm in Italy – which is a contrast with Italy’s consumer confidence standing. This is somewhat curious since the services sector is the main jobs provider and jobs drive confidence.

• The U.K. is facing Brexit; soon (perhaps?) it will no longer be an EU member. It shows below median readings across the board and has the weakest sector ranking in each sector.

• Finally, the EU sentiment gauge at the end shows only France with a ranking above 50%. French sectors outrank German sectors in every case except for construction.

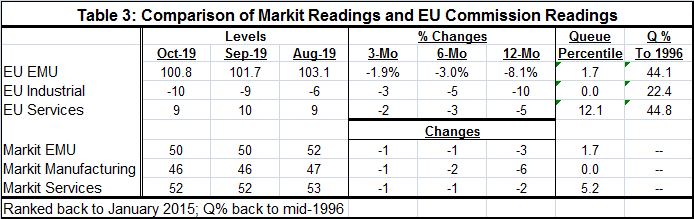

Table 3 looks at the consistency of the EU Commission indexes with respect to the Markit sector surveys. The two surveys seem to be very much on the same page with more recent weakness in Manufacturing than in services. Both show more sector weakness over 12 months than over three months or six months. And even more compelling is the queue rankings for manufacturing and services since January 2015. The industrial and services sectors also are ranked on a longer horizon that shows both are lagging their medians.

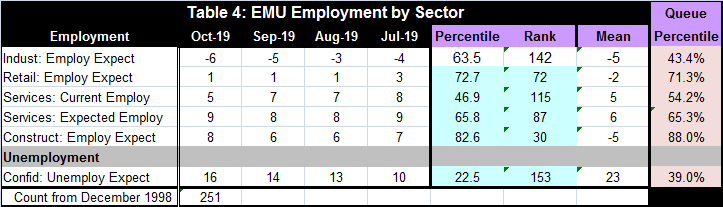

Table 4 excerpts the employment readings from the various sectors where concepts from current conditions to expected conditions to expected unemployment are presented. Not surprisingly, the sector rankings of job market responses show the most strength in construction that has been hands-down the strongest sector. This is followed by a firm signal for retailing. Both of these are for expected conditions. Industrial and services sectors both have below median overall activity readings. But for services, the actual employment assessment is still mildly above its median (54.2) and expected services employment is better still with a 65.3 percentile standing. The industrial sector has below median 43.4 percentile assessment of employment expectations. The survey of unemployment expectations is still relatively low at a 39th percentile standing. But also notice that it has been steadily climbing from July onward. This suggests that there may be more concern about the future than the sector employment indexes reveal.

Table 5 looks at the past nine cycles in the EU indexes since mid-1989. The current cycle is still a work-in progress. But as weak as the indexes seem, this is still only a ‘garden variety’ slowdown. Only the ‘slowings’ of 1998 and of 2002 were milder. 1995 that was a significant slowdown for manufacturing but was not a recession and it saw a 16.4 point drop; this cycle has seen the EMU index drop only by 13.7 points. Of course, this slowdown is not over. Trade impairment is still the order of the day. Inflation is chronically locked below target on a global basis. Brexit is still in train. There is plenty of time for this cycle to get out of control. And while there are still structural problems eating at the local economies, there is no sense that a downturn is imminent. Policy is still punching away at making progress. But in Europe the Maastricht rules keep fiscal policy use at bay while Germany has chosen this time of global slack demand to run a fiscal surplus.

Table 5 looks at the past nine cycles in the EU indexes since mid-1989. The current cycle is still a work-in progress. But as weak as the indexes seem, this is still only a ‘garden variety’ slowdown. Only the ‘slowings’ of 1998 and of 2002 were milder. 1995 that was a significant slowdown for manufacturing but was not a recession and it saw a 16.4 point drop; this cycle has seen the EMU index drop only by 13.7 points. Of course, this slowdown is not over. Trade impairment is still the order of the day. Inflation is chronically locked below target on a global basis. Brexit is still in train. There is plenty of time for this cycle to get out of control. And while there are still structural problems eating at the local economies, there is no sense that a downturn is imminent. Policy is still punching away at making progress. But in Europe the Maastricht rules keep fiscal policy use at bay while Germany has chosen this time of global slack demand to run a fiscal surplus.

Summary

The future is still in flux. While all eyes are on the U.S.-China trade deal, there are still others to come. U.S. negotiations will have to be conducted with the EMU itself. If a trade deal is struck with China and if Brexit can be ‘solved,’ those two things would eliminate a lot of uncertainty which clearly has been dogging this expansion and holding back investment. For the time-being, consumer confidence is still relatively firm, consumers are still spending and jobs are still being created. But the failure of normal inflation to reignite and ongoing downward pressures on worker wages keep a sense of risk in play. Rising (yet still low) unemployment expectations in Europe seem to be keeping an eye on these trends.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief