Global| Sep 27 2007

Global| Sep 27 2007Despite Q2 Spurt Trend in the U.S. is Slowing

Summary

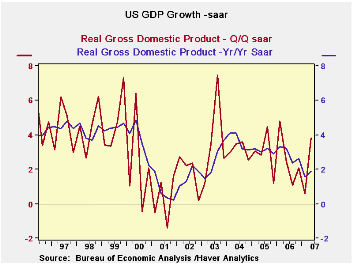

GDP’s growth in Q3 was revised down marginally in the final estimate to 3.8% from 4% previously. Growth was chipped away in a number of sectors including structures and exports while imports were revised higher. Imports drain growth [...]

GDP’s growth in Q3 was revised down marginally in the final estimate to 3.8% from 4% previously. Growth was chipped away in a number of sectors including structures and exports while imports were revised higher. Imports drain growth form the economy. GDP’s sojourn above trend in the current quarter was not on fundamental growth. Inventories rose instead of falling. The trade gap was sharply smaller instead of progressively wider. Consumption, the mainstay of GDP, shrank sharply, yet despite that business investment was stronger as GDP’s smaller sectors pushed growth above trend – especially inventories and trade. But consumer spending is two-thirds –or more– of GDP and the economy will not be able to carry strong growth on weak consumer spending. The growth spurt in Q2 was an anomaly - but so was the extreme weakness in Q1.

As the Fed looks at GDP it too is in a quandary. To make forward-looking policy you must be able to see ahead. Right now the trend in productivity is not heartening. Consumer spending has been weak and still looks soft. Vehicle sales show no life and other consumer spending generally has been soft. The August job report showed job creation turn negative. Looking ahead the Fed can’t be sure what happens next. Modest growth is the best guess but risks, mostly to the downside, are in play.

Housing’s slump is now thought to be a longer lived phenomenon than before. But layoff contagion has not hit hard – yet. Jobless claims fell to below the 300K leaving the Sept 22 week with a very strong labor market reading. So even late in Q3 the job market does not seem to have softened judging from jobless claims and despite the drop in employment In August.

On data like this it may be that the Fed is DONE cutting rates. The Fed said its…‘action is intended to help forestall some of the adverse effects on the broader economy that might otherwise arise from the disruptions in financial markets and to promote moderate growth over time.’ The Fed seems to have achieved that goal now. It is not trying to prompt strong growth, just to forestall weak growth. I would judge it to be ‘content’ with the economic results we have seen to date and would expect it to do nothing more...depending on incoming data, of course.

Q1

Q2

Q3

Q4

Q1

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief