Global| Jun 25 2009

Global| Jun 25 2009Despite Headlines About New Record Drops, Europe Is Healing

Summary

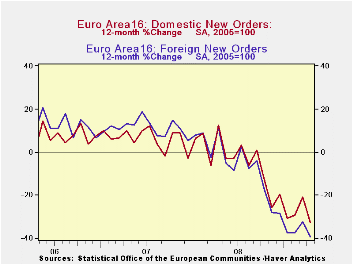

Orders in the Area fell by 32.1% a new Yr/Yr record leading to headlines about how slow the European recovery is going to be. But the pace of decline in orders over three months has been sharply reduced to an annual rate of decline of [...]

Orders in the Area fell by 32.1% a new Yr/Yr record leading to

headlines about how slow the European recovery is going to be. But the

pace of decline in orders over three months has been sharply reduced to

an annual rate of decline of 8.2% compared to 30-plus percent drop over

six months and 12-months. Both foreign-sourced and domestic–sourced

orders have trimmed their respective rates of decline sharply over

three months. The strongly negative Yr/Yr growth rate is mostly due to

legacy weakness over the earlier period.

Country level statistics are encouraging. Germany and France

have cut their respective three month growth rate declines to a pace

that is single digits; the annualized rate of decline is less than a 5%

pace. Italy is still shedding orders at nearly a 30% pace. In the UK a

spike in orders has boosted the three month growth rate to a +53%

annual rate.

Other signs in the Area show improvement as well. Italy,

despite pronounced order weakness, has been showing improved confidence

for both businesses and households. It posted a surprise rise in IP as

well. The EMU-wide PMI indices for MFG and for Services are showing

improvement on the month. On balance their trends are nothing to be

disappointed about, taking into account the extent of the weakness in

the Area which has hit countries somewhat unevenly and where fiscal

responses have been far from uniform as well. For example The

Netherlands today confirmed that its GDP drop in Q1 was the worst in

sixty years. It takes time to come back from that kind of weakness

| E-Area-13 and UK Industrial Orders | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Apr-09 | Mar-09 | Apr-09 | Mar-09 | Apr-09 | Mar-09 | |||

| E-Area Detail | Apr-09 | Mar-09 | Feb-09 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo | |

| MFG Orders | -1.0% | -0.2% | -0.9% | -8.2% | -14.0% | -34.4% | -42.0% | -32.1% | -31.0% | |

| Memo:MFG | ||||||||||

| E-13 Domestic MFG orders | -0.5% | -1.4% | 1.7% | -0.9% | -11.9% | -34.4% | -39.7% | -32.5% | -20.8% | |

| E-13 Foreign MFG orders | -2.1% | -0.6% | 1.5% | -5.1% | -25.8% | -43.5% | -49.2% | -39.5% | -32.3% | |

| Countries: | Apr-09 | Mar-09 | Feb-09 | 3-Mo | 3-Mo | 6-mo | 6-mo | 12-mo | 12-mo | |

| Germany (MFG): | -1.1% | 3.7% | -3.3% | -3.4% | -27.7% | -39.8% | -47.0% | -35.6% | -34.3% | |

| France (Ind): | 0.9% | -7.4% | 6.7% | -1.4% | -13.9% | -18.9% | -34.9% | -30.4% | -24.7% | |

| Italy (Ind): | -3.7% | -2.7% | -2.2% | -29.4% | -30.0% | -36.9% | -40.1% | -31.8% | -29.9% | |

| UK (Engineering Industy): | -8.3% | 7.1% | 13.3% | 53.0% | -56.3% | -28.2% | -45.2% | -27.0% | -11.4% | |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief