Global| Dec 12 2008

Global| Dec 12 2008Decline is 'Everywhere' !

Summary

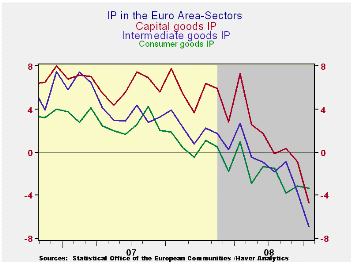

The contribution to growth from IP is weakening sharply. The decline in IP, one that is an inflation-adjusted reading, is at a -13.5% rate in Q4. Consumer goods output is the strong sector, oddly enough, falling at a -3.8% pace early [...]

The contribution to growth from IP is weakening sharply. The

decline in IP, one that is an inflation-adjusted reading, is at a

-13.5% rate in Q4. Consumer goods output is the strong sector, oddly

enough, falling at a -3.8% pace early in Q4. Intermediate goods output

is falling at a 19% annual rate in the quarter. Capital goods output is

falling at a 15% annual rate in Q4. The fourth quarter is cropping up

to be extremely weak.

The sequential growth rates from 12-mo to 6-Mos to 3Mos also

show that the annual rate of decline in output is generally getting

worse or staying near its worst growth rates across industries.

The results for the key large countries mirror the overall

findings. Spain whose numbers are simply more volatile that the rest,

shows the smallest quarter to date decline. I suspect that will change

as more numbers roll in. Spain is not doing well. Germany, France and

Italy each show a larger Yr/Yr decline in IP than the EMU-wide average

for the current quarter. For Yr/Yr growth in IP France, Italy and Spain

are worse than the EMU-wide average for MFG output.

The sting of decline is sharp in EMU and it has hit very hard

in the last two months IP has been in sporadic decline in EMU as it had

fallen (m/m) five times in 2007. But through October in 2008 IP already

has fallen in seven of ten months. Moreover the declines in Sept and

Oct have been severe and, of course, back to back. Output has dropped

in five of the past six months. The outlook for the final two months is

for the figures to stay bad or to get worse. No wonder the EU finally

got around to approving a stimulus plan worth about 1.5% of GDP as the

IMF suggested. There is no VAT cut as Germany’s Merkel has been opposed

to that. But the EU may review further stimulus options later.

| E-zone MFG IP | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | Mo/Mo | Oct 08 |

Sep 08 |

Oct 08 |

Sep 08 |

Oct 08 |

Sep 08 |

|||

| Ezone Detail | Oct 08 |

Sep 08 |

Aug 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-4 |

| MFG | -1.3% | -1.9% | 0.7% | -9.8% | -6.0% | -9.0% | -5.7% | -5.1% | -2.7% | -13.5% |

| Consumer | 0.0% | -0.7% | -0.5% | -4.8% | -4.8% | -5.3% | -3.5% | -3.3% | -3.1% | -3.8% |

| C-Durables | -1.4% | -2.5% | 0.8% | -11.4% | -10.0% | -13.2% | -7.1% | -8.1% | -6.5% | |

| C-Non-durables | 0.3% | -0.8% | -0.4% | -3.5% | -5.0% | -3.7% | -3.7% | -2.4% | -2.9% | |

| Intermediate | -2.0% | -3.0% | 1.2% | -13.9% | -8.4% | -11.8% | -7.2% | -6.9% | -3.7% | -19.3% |

| Capital | -2.0% | -1.9% | 1.3% | -9.9% | -4.2% | -11.0% | -3.3% | -4.7% | -0.9% | -15.6% |

| Main E-zone Countries and UK IP in MFG | ||||||||||

| Mo/Mo | Oct 08 |

Sep 08 |

Oct 08 |

Sep 08 |

Oct 08 |

Sep 08 |

||||

| MFG Only | Oct 08 |

Sep 08 |

Aug 08 |

3Mo | 3Mo | 6mo | 6mo | 12mo | 12mo | Q-2 Date |

| Germany: | -2.2% | -3.6% | 3.3% | -9.8% | -8.5% | -11.0% | -6.6% | -3.9% | -1.8% | -19.2% |

| France:IPx Construct'n |

-2.7% | -0.8% | -0.5% | -14.7% | 0.0% | -12.3% | -4.9% | -7.2% | -2.3% | -18.3% |

| Italy | -1.1% | -2.9% | 0.1% | -14.6% | -15.2% | -12.9% | -9.8% | -6.8% | -6.5% | -16.7% |

| Spain | 0.3% | 2.8% | -10.1% | -26.1% | 15.3% | -29.4% | 14.1% | -11.2% | -4.7% | -8.7% |

| UK | -1.3% | -1.0% | -0.6% | -10.8% | -7.2% | -8.3% | -6.2% | -4.9% | -3.2% | -12.1% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.