Global| Nov 07 2016

Global| Nov 07 2016Cross Currents for German Orders and Elsewhere

Summary

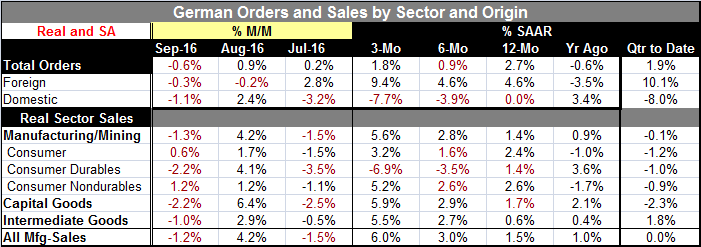

Weakness in September German new orders fell across the board in September. Overall orders fell month-to-month by 0.6% as foreign orders fell by 0.3% and domestic orders fell by 1.1%. Year-over-year trends (see table and chart) show [...]

Weakness in September

Weakness in September

German new orders fell across the board in September. Overall orders fell month-to-month by 0.6% as foreign orders fell by 0.3% and domestic orders fell by 1.1%. Year-over-year trends (see table and chart) show that foreign orders have been gaining pace recently while domestic orders have been weak and are weakening. Foreign orders are accelerating over 12 months to six months to three months as domestic orders are decelerating on the same horizons.

Overall pattern/trend unclear

As a result of opposite patterns for domestic and foreign orders, the German overall order pattern is without clear trend.

Sales momentum better than orders

German real sector sales are accelerating with consumer durables, capital goods and intermediate goods sales patterns all showing steady acceleration. Nondurable goods sales have been unstable and recently have been weaker, decelerating and falling.

Current quarter mixed

In the quarter-to-date (just completed Q3), overall orders are up at a 1.9% pace while real sector sales are weak across the board and are falling.

Euro area orders down

German new orders from within the euro area were down 4.5% on the month, while new orders from other countries increased by 2.5% compared to August 2016. Also in September the manufacturers of intermediate goods saw new orders rise by 0.5% compared with one month ago. The manufacturers of capital goods showed decreases of 1.6% on the previous month. For consumer goods, there was an increase in new orders of 0.5%.

Related news

Taiwan reported improved export results for October as it saw a rebound with exports rising by 9.4% year-on-year after falling in the previous month. Conditions in Asia are still touch and go. The revival in Taiwan exports does dovetail with German order news which showed some strength in trade (orders) outside of the euro area in September. That's still thin gruel for good news.

Retail trends: depressing dillies

Also on the day Germany reported a fall in retail sales that was the largest drop in two years. The euro area also reported a September retail sales drop but one of only 0.2%. Still, euro area sales are clearly decelerating from 12-month to six-month to three-month with year-over-year sales up by only 1.1% and with the three-month pace of sales falling at a 0.4% annualized rate. Most early reporting countries (EMU: Germany, Portugal, Austria; EU: U.K., Denmark & Sweden) show retail sales falling in September among the early reports showing an increases in retail sales is Denmark where sales edged up by 0.3% after being flat in August. Elsewhere sales fell.

Wrap up

On balance, the German orders data, the context from world trade, the global PMI data and the recent EU/EMU retail sales patterns show ongoing erratic trends that tend to the weak side. There has been some firming in the recent global PMI reports. There is still firm investor confidence as the Sentix indicator of investor confidence reported today showed a rise to 13.1 in October from 8.5 in September. Investors are not throwing in the towel by any means. Economic performance is still marginal, but it is staying in the plus column. There are few pessimistic enough to call for a recession. But the political landscape has been treacherous, too. There was the unexpected U.K. Brexit vote. Italy has an important referendum on tap and national elections among divisive candidates will be decided in the United Sates on Tuesday of this week. However, on the bright side, the Canadian-EU CETA trade deal has resolved the conflict in Belgium that held it back and Spain has reached a more stable political arrangement in recent weeks. But new turbulence in Hong Kong this weekend over the state and confidence of its separate governance is a reminder that it is both global economics and politics that offer a threat of instability. Monetary policy is still being leaned upon steadily, but perhaps the ramping up of that dependence has seen its end of days. Monetary policy may just have done all it can do apart from keeping markets liquid; in the U.S., policy is preparing to do less. While more speak of fiscal policy, it is not clear where or how it might be pressed into action if at all. Nor is it completely clear how developing political trends might affect policy.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief