Global| Jan 30 2007

Global| Jan 30 2007Consumer Confidence Rose Slightly, Highest Since 2002

by:Tom Moeller

|in:Economy in Brief

Summary

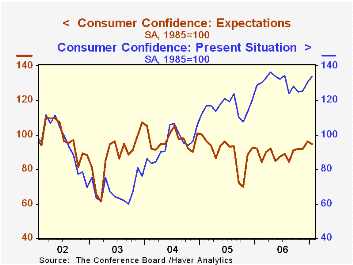

Consumer confidence increased a modest 0.3% in January, according to the Conference Board Survey, following an upwardly revised 4.5% December gain. The increase was to the highest level since March 2002. The reading of present [...]

Consumer confidence increased a modest 0.3% in January, according to the Conference Board Survey, following an upwardly revised 4.5% December gain. The increase was to the highest level since March 2002.

The reading of present conditions rose a firmer 2.6% after the 4.1% December increase as the percentage of respondents who viewed business conditions as good rose to 28.1%, the highest since last May. The percentage who viewed jobs as plentiful also rose to 29.9%, the highest since 2001.

Expectations, however, reversed nearly half of the December gain with a 1.9% decline. Expectations about future income fell the hardest, offset by an uptick in expected employment conditions.

The expected inflation rate in twelve months ticked lower to 4.7%, that was versus expectations during all of last year for a 5.1% rate of inflation in twelve months.Monetary Policy Inertia and Recent Fed Actions from the Federal Reserve Bank of San Francisco can be found here.

| Conference Board (SA, 1985=100) |

January | December | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Consumer Confidence Index | 110.3 | 110.0 | 3.3% | 105.9 | 100.3 | 96.1 |

| Present Conditions | 133.9 | 130.5 | 4.0% | 130. | 116.1 | 94.9 |

| Expectations | 94.5 | 96.3 | 2.6% | 89.7 | 89.7 | 96.9 |

by Tom Moeller January 30, 2007

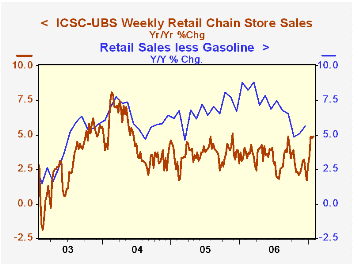

The ICSC-UBS retail chain-store sales index is constructed using the same-store sales (stores open for one year) reported by 78 stores of seven retailers: Dayton Hudson, Federated, Kmart, May, J.C. Penney, Sears and Wal-Mart.

The leading indicator of chain store sales from ICSC-UBS also gave back all of the gains during the prior two weeks with a 1.1% decline and for the month is 0.4% below December.Access to Credit is the latest International Economic Trends from the Federal Reserve Bank of St. Louis and it is available here.

| ICSC-UBS (SA, 1977=100) | 1/27/07 | 1/20/06 | Y/Y | 2006 | 2005 | 2004 |

|---|---|---|---|---|---|---|

| Total Weekly Chain Store Sales | 476.4 | 480.9 | 4.9% | 3.3% | 3.6% | 4.7% |

by Louise Curley January 30, 2007

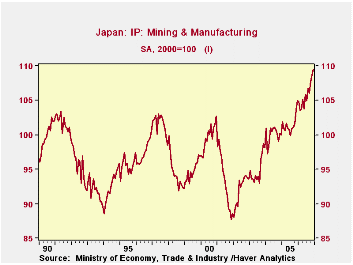

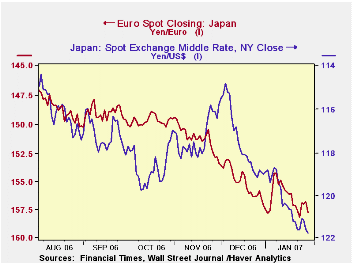

The economic news out of Japan is ambiguous. Production and exports are strong, employment, retail sales and family living expenditures are weak. The yen has depreciated sharply in recent weeks against the euro and the dollar. The yen is, currently, at its lowest point against the Euro since the introduction of the Euro in 1999.

Japanese industrial production made a new record in December, 2006 at 109.5 (2000=100), exceeding previous peak levels reached in 1991, 1997 and 2000 as can be seen in the first chart.

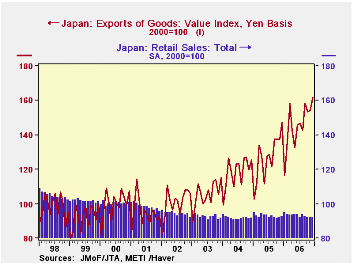

The strength in the production sector has not come from domestic consumer demand but, rather, from export demand. The second chart compares the index of retail trade and the value index of exports, both with a base of (2000=100). The index of retail sales was 92.0 in December, down from 92.2 in November and from 92,7 in December, 2005, while the value index of exports was 161.79 up 5.0% from November and 9.84% from December, 2005. Expenditures

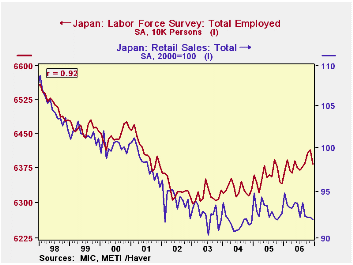

Part of the sluggishness in retail trade is due to the relatively slow growth in employment. The third chart compares retail sales with total employment. There is a good correlation between the two series--.92. Although employment in December was 0.7% above the year ago figure it was 0.5% below November, 2006. Moreover, the unemployment rate rose by one percentage point to 4.1% in December.

Depreciations of the yen against the Euro and the U.S. dollar have stimulated the demand for exports. The very rapid depreciation of the yen in recent weeks is shown in the fourth chart.

| Dec 06 | Nov 06 | Dec 05 | M/M % | Y/Y% | 2006 | 2005 | 2004 | |

|---|---|---|---|---|---|---|---|---|

| Industrial Production (2000=100) | 109.5 | 108.7 | 104.9 | 0.74 | 4.39 | 105.9 | 101.6 | 100.0 |

| Exports | 161.7 | 154.0 | 147.21 | 5.00 | 9.84 | 145.70 | 127.10 | 118.42 |

| Retail Trade | 92.0 | 92.2 | 92.7 | -0.22 | -0.76 | 93.1 | 93.0 | 91.7 |

| Family Living Expenditures | 92.8 | 93.8 | 94.0 | -1.01 | -1.31 | 93.0 | 94.8 | 95.6 |

| Employment (millions) | 63.83 | 64.15 | 63.41 | -0.50 | 0.66 | 63.83 | 63.57 | 63.29 |

| Unemployment Rate (%) | 4.1 | 4.0 | 4.4 | 0.1 | -0.3 | 4.1 | 4.4 | 4.7 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief