Global| Jun 24 2009

Global| Jun 24 2009Consumer Confidence Recovers In Italy

Summary

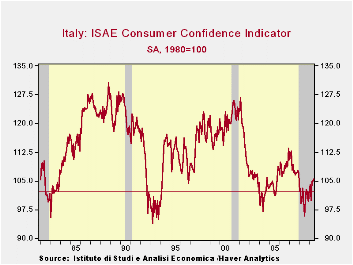

Consumer confidence in Italy has risen firmly in June. Confidence now has risen in five of the past seven months having fallen in only one of those months. The trend to improvement is clear. The overall confidence measure from ISAE is [...]

Consumer confidence in Italy has risen firmly in June.

Confidence now has risen in five of the past seven months having fallen

in only one of those months. The trend to improvement is clear. The

overall confidence measure from ISAE is not in the 35th percentile of

its range- still quiet weak but not so disastrous.

The overall situation in the past 12 months is given a rating

of -68 which sounds terrible. Actually that reading is in the 55th

percentile of its range of historic outcomes and stands above the

average response of -71. For the next 12-months the rating is in the

40th percentile of range and is only slightly below the average

response for that category. It’s a return to sub-normalcy.

The ability to make major purchase right now is at the index

average, but the mid point of its range at the 43.9th range percentile.

For the future the response rate is a super strong 95th percentile

reading.

Despite this improved news, fears of unemployment still rate

high in 66th percentile of their range but even higher when we look at

the ranking percentile. The latter measure tells how many responses are

below the current response: that percentage is 96.2%. In other words,

unemployment fears are worse than this only about FOUR percent of the

time. Still the range reading tells us that there have been times when

the fears were much, much, greater. The ranking percentile says yes,

that maybe so, but there have not been many of those times. We can

compare the ranking and the range percentiles for each response to get

a better fix on what the raw responses man. Cleary the raw responses

taken alone can be very misleading across categories.

As you can tell by surveying these responses and looking at

the percentile ranges or rankings each category has its individual

distribution of responses. Over the past 200-some months the overall

situation reading averages a -71 reading while the ‘overall situation

for the next 12-months’ averages a -9. Go figure. Are 12-monht periods

usually that different? I don’t think so. We use the percentile and

range readings to try to shift though these responses to get a more

accurate assessment of the consumer’s mood.

For now it is apparent that there is an improvement in the

Italian consumer’s mood, and also some paradox. There is still a high

fear of unemployment but apparently the social safety network is good

enough that is not raising a lot of anxiety about the future or even

about the ability to spend on consumer items. That may seem unusual but

after all this is Europe and it’s Italy. Those are simply the facts.

| Italy ISAE Consumer Confidence | |||||||

|---|---|---|---|---|---|---|---|

| Since Jan 1992 Rank | |||||||

| Jun-09 | May-09 | Apr-09 | Mar-09 | Percentile | Rank | percentile | |

| Consumer Confidence | 105.4 | 104.9 | 104.9 | 99.9 | 35.0 | 148 | 28.8% |

| Last 12 months | |||||||

| OVERALL SITUATION | -68 | -73 | -74 | -84 | 63.2 | 93 | 55.3% |

| PRICE TRENDS | -40.5 | -45 | -43 | -45 | 9.3 | 205 | 1.4% |

| Next 12months | |||||||

| OVERALL SITUATION | -8 | -17 | -26 | -35 | 49.2 | 123 | 40.9% |

| PRICE TRENDS | 8.5 | 10 | 9.5 | 7 | 17.3 | 101 | 51.4% |

| UNEMPLOYMENT | 15 | 17 | 21 | 38 | 66.2 | 8 | 96.2% |

| HOUSEHOLD BUDGET | 0 | 5 | 1 | 5 | 15.6 | 200 | 3.8% |

| HOUSEHOLD FIN SITUATION | |||||||

| Last 12 months | -37 | -34 | -37 | -39 | 38.8 | 126 | 39.4% |

| Next12 months | -4 | -5 | -11 | -10 | 63.3 | 117 | 43.8% |

| HOUSEHOLD SAVINGS | |||||||

| Current | 60 | 59 | 60 | 69 | 72.7 | 13 | 93.8% |

| Future | -25 | -29 | -29 | -33 | 51.1 | 145 | 30.3% |

| MAJOR Purchases | |||||||

| Current | -39 | -43 | -41 | -43 | 43.9 | 90 | 56.7% |

| Future | 3 | 1 | 3 | 3 | 95.7 | 3 | 98.6% |

| Total number of months: 208 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief