Global| Apr 27 2009

Global| Apr 27 2009Consumer Confidence Improves Sharply In Italy

Summary

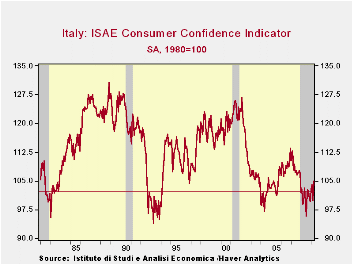

The consumer confidence reading for Italy has been weak in this cycle but not quite as weak as it was in the previous two downturns in the early 1980s and early 1990s. Despite the bad press this business cycle keeps getting, in Italy [...]

The consumer confidence reading for Italy has been weak in

this cycle but not quite as weak as it was in the previous two

downturns in the early 1980s and early 1990s. Despite the bad press

this business cycle keeps getting, in Italy consumers have not

generally gotten as despondent as in the past two cycles nor have they

stayed as depressed for as long. That is probably against public

perceptions of this recession. Indeed, when I looked at these results I

double checked the spread sheet to see if I’d entered the dates

correctly – and I had. I was (I am!) surprised.

The chart on Italy’s consumer disposition is demonstrating a

clear uptrend, albeit in an oscillating fashion. This month’s reading

is the highest it has been Since December 2007. Moreover the 5.1 point

jump m/m is the fifth largest month-to-month jump in the index since

early 1992. The level of the index is still low but the jump is large.

The rise in the index is notable – especially given the size

of the rise - since Italian unemployment is expected to rise further

and consumer conditions are importantly a reflection of labor market

conditions. In Germany, too, the GfK index of consumer sentiment which

is a survey that projects readings for May shows consumer confidence

unchanged even though last week the leading German research institutes

came out with harsher assessments for the German economy for 2009. For

some reason- and Italian consumers are not alone in this – consumer

confidence is firming in the face of news that is in many ways

worsening.

The devil is in the details -- Italian consumers assess their

own mood with an index value of 104.9 which stands in the 33rd

percentile of its range of values back to January of 1992. The index is

weaker than this level only 27% of the time. So while these are low

readings they are not among the worst ever. The overall situation for

the past 12-months is evaluated as in the 58th percentile of its range,

ranking 121st out of 208 observations leaving it in the bottom 41st

percentile of its range. These statistics give the raw readings more

meaning by putting them in the context of the range of values and in

the context of rankings (frequency). We use ‘the percentile of the

range of value’ instead of ‘percent of mean’ since these components can

move in both positive and negative ranges: ‘percent of mean’ is just

not meaningful. Being in the 58th percentile means that although the

reading is above the mid point of its range it is still a moderate

reading: In fact it appears as an even lower reading in this case since

60% of the time the assessment is better than this. In this way we can

use percentage of range and ranking data to close in on what the

current reading really means

Over the next 12 months the reading for the overall situation

is, however, lower residing in the 20th percentile of its range and

being lower only 16% of the time. By this reading we see that

conditions have not been good and they are expected to get worse.

Still, in the last two recessions these metrics were even worse.

Unemployment for the next 12-months remains very bad, in the 75th

percentile of its range but with the fifth worst reading overall- a

ranking that puts it in the top 3% all time. That is to say that

unemployment fears have been worse than this only 3% of the time.

The household financial situation is in the 38th percentile

for the last 12 months and is expected to be in the 49th percentile of

range for the next 12-months. While 49th percentile is a ‘mid range’

reading that is misleading since the actual reading is lower than that

level only about 17 percent of the time. Apparently the range is wide

and skewed.

Perhaps the real reason Italian consumer sentiment is not so

bad is that Italians remain optimistic about the future, despite their

adverse sentiment. When they assess if it it’s the right time to make a

major purchase they put the current situation in the 40Th percentile of

its range. But when they assess the future they put it in the 95th

percentile of the range. So Italian consumers seem to admit that the

current situation is bad and may get worse in the period ahead. Yet

they remain optimistic that there will be a better time to buy things

in the coming months by a wide margin. Consumer optimism on the time to

make major purchases stands in marked contrast to assessments of the

overall situation for the next 12months as well as to fears of

unemployment and pressures on the household budget. We might be

encouraged to dismiss some of this optimism except we see it arising in

Germany as well. It’s a trend to watch for elsewhere.

| Italy ISAE Consumer Confidence | |||||||

|---|---|---|---|---|---|---|---|

| Since Jan 1992 Rank | |||||||

| Apr-09 | Mar-09 | Feb-09 | Jan-09 | Percentile | Rank | percentile | |

| Consumer Confidence | 104.9 | 99.8 | 104 | 102.6 | 33.4 | 151 | 27.4% |

| Last 12 months | |||||||

| OVERALL SITUATION | -74 | -84 | -78 | -75 | 58.4 | 121 | 41.8% |

| PRICE TRENDS | -43 | -45 | -38.5 | -33.5 | 4.1 | 207 | 0.5% |

| Next 12months | |||||||

| OVERALL SITUATION | -26 | -35 | -26 | -22 | 20.6 | 174 | 16.3% |

| PRICE TRENDS | 9.5 | 7 | 7.5 | 8.5 | 19.4 | 96 | 53.8% |

| UNEMPLOYMENT | 21 | 38 | 28 | 20 | 75.0 | 5 | 97.6% |

| HOUSEHOLD BUDGET | 1 | 5 | 8 | 4 | 17.0 | 198 | 4.8% |

| HOUSEHOLD FIN SITUATION | |||||||

| Last 12 months | -37 | -39 | -35 | -36 | 38.8 | 127 | 38.9% |

| Next12 months | -11 | -10 | -10 | -10 | 49.0 | 172 | 17.3% |

| HOUSEHOLD SAVINGS | |||||||

| Current | 60 | 69 | 66 | 59 | 72.7 | 13 | 93.8% |

| Future | -29 | -33 | -29 | -38 | 40.4 | 159 | 23.6% |

| MAJOR Purchases | |||||||

| Current | -41 | -43 | -39 | -42 | 40.4 | 99 | 52.4% |

| Future | 3 | 3 | 7 | 6 | 95.7 | 3 | 98.6% |

| Total number of months: 208 | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief