Global| Mar 29 2021

Global| Mar 29 2021Consumer Confidence Backtracks in Finland

Summary

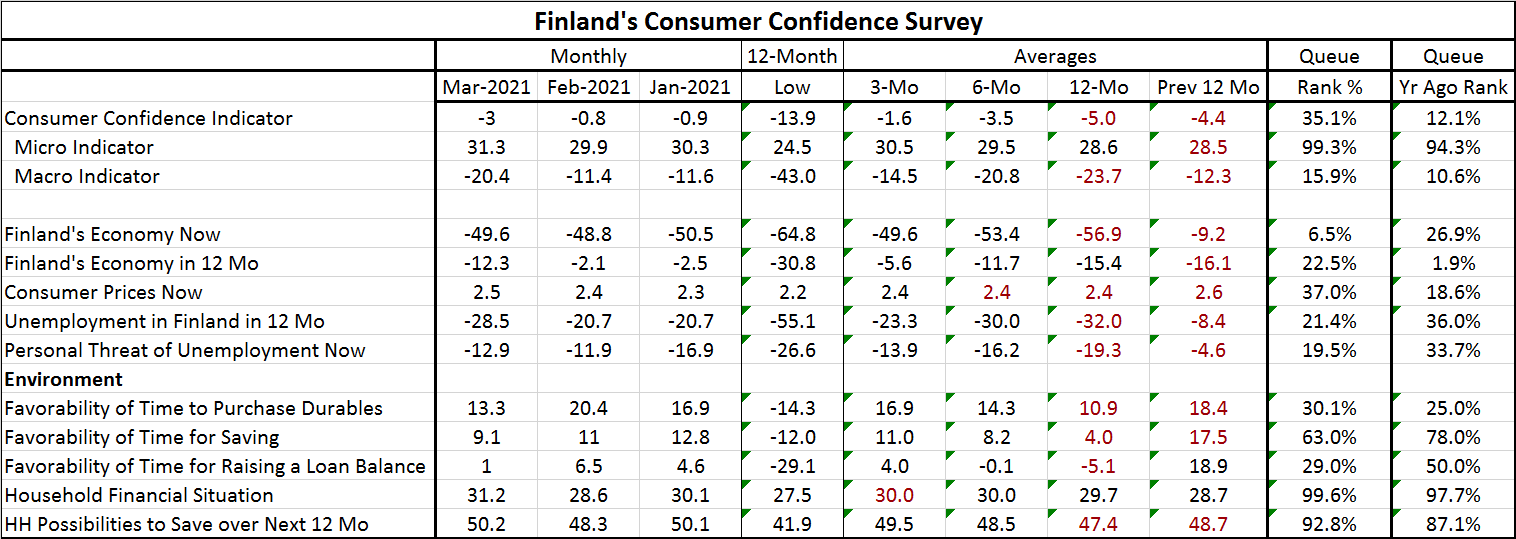

Consumer confidence in Finland stepped back in March, dropping to a reading of -3 from -0.8 in February. The March reading has a 35.1 percentile standing among data back to 1998 but shows a substantial improvement from one year ago [...]

Consumer confidence in Finland stepped back in March, dropping to a reading of -3 from -0.8 in February. The March reading has a 35.1 percentile standing among data back to 1998 but shows a substantial improvement from one year ago when the ranking for the March 2020 reading was in its 12.1 percentile.

Consumer confidence in Finland stepped back in March, dropping to a reading of -3 from -0.8 in February. The March reading has a 35.1 percentile standing among data back to 1998 but shows a substantial improvement from one year ago when the ranking for the March 2020 reading was in its 12.1 percentile.

The micro indicator in the survey drawn from individual experiences shows a pick-up on the month to 31.3 in March from 29.9 in February. The macro indicator assessment of overall conditions, however, took a large step back in March to -20.4 from -11.4 in February. The micro indicator has a 99.3 percentile standing, a very strong position, while the macro indicator has a 15.9 percentile standing, quite a weak value. Both readings improve their respective rankings compared to one year ago.

The direct assessments of the economy are not so upbeat at all. Finland's economy 'now' assessment slips to a rating of -49.6 in March from -48.8 in February achieving a 6.5 percentile standing- the weakest standing in the table this month. However, the economy assessed 12-months-ahead slips to a worsened -12.3 in March from -2.1 in February; this brings it to a 22.5 percentile queue standing, not as weak as for the 'economy now' but not a prize result to be sure.

The inflation rate is only ticking higher and remains low at a ranking below its median (37.0%). The Unemployment assessment in 12 months fell to -28.5 in March from -20.7, an improved result. Unemployment has only a 21.4 percentile standing; that is a weak ranking for a bad event and therefore good news. The personal threat of unemployment also weakened on the month and has a slightly lower standing.

The assessment of the economic environment was mixed in March with the current purchase and savings environments slipping along with assessment for the time being right to take out a loan. But the household financial situation is deemed better as is the possibility to save in the period ahead is improved. The financial situation and the prospects for savings in the future are especially strong assessment in March with queue rankings well into their respective top ten percentiles. The ratings for the time to purchase durable goods or to take out or expand a loan are both in the lower third of their respective queues of data.

If we look at trends or progressions, the changes in the 12-month to six-month to three-month averages show widespread improvement in train there are no deteriorations among the components on those timeline comparisons. However, seven categories (including the headline) in March are weaker than their respective three-month averages. But one of those is unemployment related. Eliminating that one cuts the total number worsening to 6 and makes 5 of 12 component readings weaker. Add back in the headline, and that raises the grand total showing deterioration to six. Five components are decaying in a bad way in the current month compared to the three-month average. What has worsened on this short timeline comparison? The overall confidence metric, the macro indicator, expectations for the economy in 12 months, the favorability of the time to purchase durable goods, or to save, or to take out a loan, all have sunk below their respective three-month averages. And we can raise the count to 7 bad events since the personal threat of unemployment rose slightly one-month to three-months. That's six of 12 component categories showing either deterioration or temporary retrograde motion on the month plus the index itself eroding. We would have to say that the jury is out on the subject of near-term momentum for confidence in Finland.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief