Global| Sep 04 2019

Global| Sep 04 2019Composite PMIs Remain Low But Firm in August

Summary

Globally, composite PMIs in August generally firmed a bit while manufacturing remained weak and mixed month-to-month with a small tilt to improvement. Viewed on data over the last four and two-thirds years, manufacturing in the seven [...]

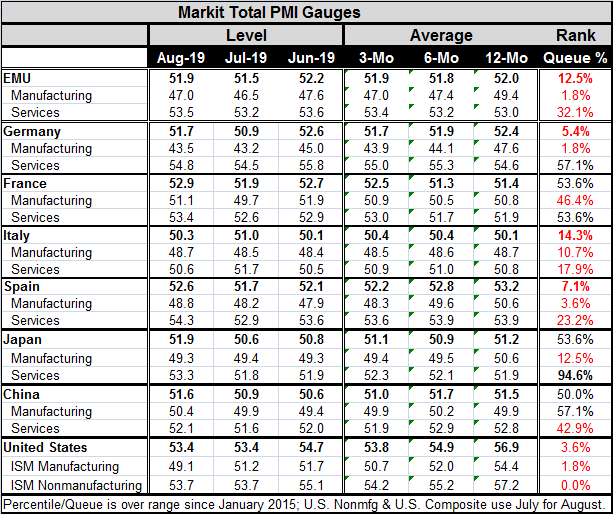

Globally, composite PMIs in August generally firmed a bit while manufacturing remained weak and mixed month-to-month with a small tilt to improvement. Viewed on data over the last four and two-thirds years, manufacturing in the seven countries in the table (including U.S.) plus the EMU averages a 17.0 percentile standing. On the same period, services readings average a 45.9 percentile standing, excluding the U.S. where service sector data are missing). Both manufacturing and services have rankings that leave them below their respective medians over the last four and two-thirds years. Manufacturing is consistently and chronically the weaker sector by queue standing except in China. In France, the manufacturing and service sector standings are 'relatively close but still separated by nearly 11 ranking percentile points with manufacturing weaker.

Globally, composite PMIs in August generally firmed a bit while manufacturing remained weak and mixed month-to-month with a small tilt to improvement. Viewed on data over the last four and two-thirds years, manufacturing in the seven countries in the table (including U.S.) plus the EMU averages a 17.0 percentile standing. On the same period, services readings average a 45.9 percentile standing, excluding the U.S. where service sector data are missing). Both manufacturing and services have rankings that leave them below their respective medians over the last four and two-thirds years. Manufacturing is consistently and chronically the weaker sector by queue standing except in China. In France, the manufacturing and service sector standings are 'relatively close but still separated by nearly 11 ranking percentile points with manufacturing weaker.

If we look at the averages for the composite PMI measures, we find a tendency for some stability. In the EMU, at least the three-month average is no longer below the six-month average. That is also true for France and Italy (also EMU members) as well as Japan. But for Spain and China, deterioration in the composite PMI level has continued despite some bump up on the month.

France is the only country/region in the table in which the manufacturing three-month average has broken a string of ongoing deterioration from the 12-month average to the six-month average to the three-month average. This is even though on the month all manufacturing gauges improved month-to-month except Italy.

The services sector is mixed on the month. It improved for the three-month average in the EMU, France, and Japan. Germany, Italy, Spain, and China show ongoing deterioration for services in terms of their three-month to six-month comparison. This is despite the fact that services improved month-to-month everywhere except in Italy.

Trends and momentum are somewhat mixed in August but only in a 'small' sense. The larger trend is still lower, sharply lower for manufacturing. However, there is evidence that the pace of deterioration has slowed and reason for hope that deterioration may have bottomed. For example, for four of the seven countries/regions in the table (excluding the U.S.), the August value of the composite PMI exceeds its 12-month average. For manufacturing, three of eight (here we include the U.S. because the ISM value for manufacturing has been released) show an August manufacturing PMI value above the respective 12-month average. Those three countries are France, Italy (unchanged, actually), and China. The U.S. shows the largest deterioration on this metric. As for services, five of seven countries/regions show improvement on comparing the current monthly services reading to the 12-month average. These are the EMU, Germany, France, Spain, and Japan. Italy and China are exceptions, still wearing lower and U.S. data are not yet available.

Still, the PMI metric remains weak with six of eight manufacturing metrics showing contraction (values below 50). France and China (China barely) are exceptions. The services sector is still growing everywhere. While manufacturing is struggling as you would expect with the trade war front and center, the consumer has been propping up growth. But the consumer needs to be monitored. In the U.S. the University of Michigan consumer sentiment series weakened sharply at the end of August. In the EMU, retail sales just posted their sharpest drop in seven months. Adversity is battering the global economy. We should not 'take it for granted' that the services sector will weather the storm and prop up manufacturing. The data to date are somewhat encouraging on that score, but nothing is yet decided and central banks are still trying to pick their way through the data and trying to decide what their role should be. We hope that we have seen the worst of the trade war, but that is always hard to tell. The U.S. and China are still planning to talk. Brexit in some form is still in motion in Europe, but the U.K. side is in true disarray. There are more surprises lurking out there. We can only hope that some of them will be positive surprises.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief