Global| May 01 2018

Global| May 01 2018China’s Manufacturing PMI Hovers, Showing Positive Growth

Summary

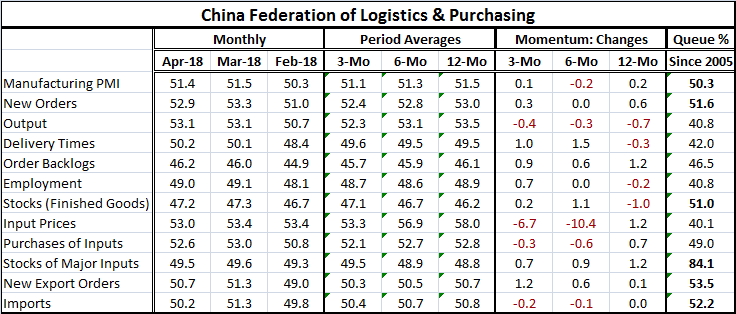

China manufacturing PMI is only slightly weaker in April compared to March and holds most of the March gain over February. Still, the PMI is only moderately valued standing in the 50th percentile of its historic range of values – [...]

China manufacturing PMI is only slightly weaker in April compared to March and holds most of the March gain over February. Still, the PMI is only moderately valued standing in the 50th percentile of its historic range of values – right on top of its historic median with weak diffusion reading.

China manufacturing PMI is only slightly weaker in April compared to March and holds most of the March gain over February. Still, the PMI is only moderately valued standing in the 50th percentile of its historic range of values – right on top of its historic median with weak diffusion reading.

The sequence of momentum changes shows that output displays a pattern of ongoing declines in its diffusion gauge. Contrarily, order backlogs are rising, stocks are rising and new export orders continue to advance. All this as overall orders show a marginally expanding path.

Still, of the 11 PMI categories, only five of them have standings above 50, their respective medians. The highest PMI standing, unfortunately, is for inventories of major inputs. The next two highest standings are for export and import orders. The final component with a standing above its median is for finished stocks.

Inventories are out ahead of output and order trends. That generally is not a good sign. But while output is fading, possibly because inventories are bloated, orders are still advancing.

In diffusion terms, both output and orders are increasing as both series have values above 50. But the output gain is well behind its usual thrust – that is what the queue standing tells us. And delivery times are speeding up, reinforcing the notion of growing slack rather that encroaching tightness. Employment diffusion also shows an erosion which is a problem since job growth is one of the main objectives for China’s growth overall.

While finished goods stocks have a queue standing above 50, the diffusion reading shows us that stock levels are eroding. Similarly, stocks of major inputs have a very high queue standing and also show erosion, but a very slow and diminishing erosion.

China’s manufacturing sector is still tied in a knot. The signs of recovery are not yet present. The sector is barely creating growth and world trade tensions hang over its head. Asia has lagged the West in the expansion cycle and that continues to be true. There are a number of economic, global trade and geopolitical loose ends. All of this clouds the future.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief