Global| Aug 31 2020

Global| Aug 31 2020China's Manufacturing PMI Is Stuck

Summary

Manufacturing in China has improved and in August it is still expanding. But the PMI in August stepped back a tick to 51.0 from July's 51.1. At a mark of 51.0, it is barely indicating expansion at all. And even the three-month average [...]

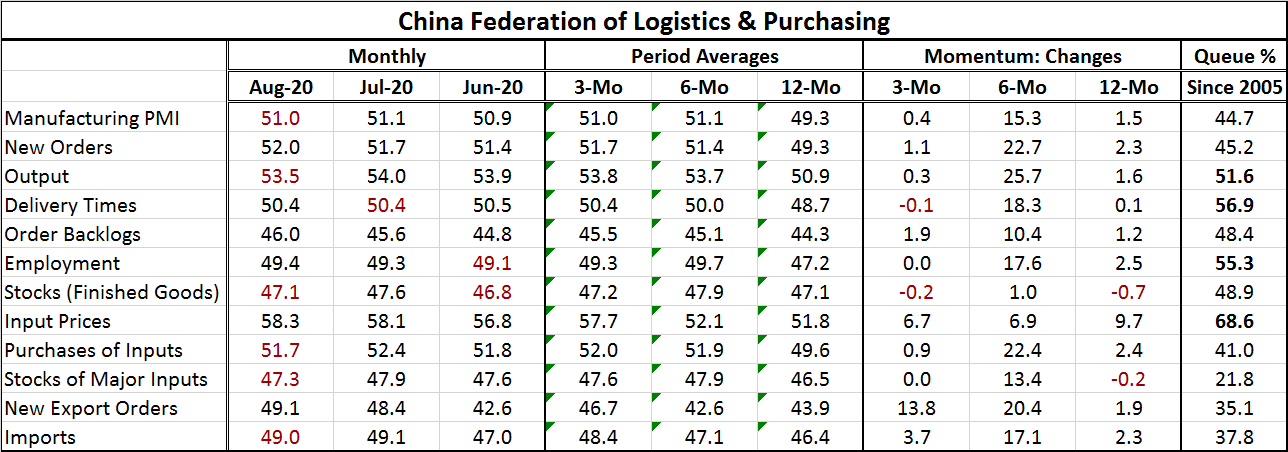

Manufacturing in China has improved and in August it is still expanding. But the PMI in August stepped back a tick to 51.0 from July's 51.1. At a mark of 51.0, it is barely indicating expansion at all. And even the three-month average is lower than the six-month average (51.0 vs. 51.1), but the net change over three months (point to point) is positive, improving by 0.4 diffusion points. These various metrics identify Chinese manufacturing as being in a very flat low growth trajectory. The table also ranks the level of the PMI index on a timeline back to January 2005. On that basis, the PMI has a 44.7 percentile rank, leaving it just short of its median on this timeline (medians occur at a ranking of 50).

Manufacturing in China has improved and in August it is still expanding. But the PMI in August stepped back a tick to 51.0 from July's 51.1. At a mark of 51.0, it is barely indicating expansion at all. And even the three-month average is lower than the six-month average (51.0 vs. 51.1), but the net change over three months (point to point) is positive, improving by 0.4 diffusion points. These various metrics identify Chinese manufacturing as being in a very flat low growth trajectory. The table also ranks the level of the PMI index on a timeline back to January 2005. On that basis, the PMI has a 44.7 percentile rank, leaving it just short of its median on this timeline (medians occur at a ranking of 50).

The manufacturing PMI has 11 components of which only four have rankings (queue standings) above their historic medians. Input prices have the strongest ranking, delivery times have the second highest ranking followed by employment and finally output at a rank standing of 51.6. The above median standing for deliveries may reflect ongoing issues with supply chain management more than any bottleneck effect. Activity has not been strong enough to have generated any true shortages due to scarcity. The problem is -or will be- getting supply chains functioning again.

China registers a very low standing for stocks of major inputs as well as for new export orders. Imports also have a below 40th percentile standing. Obviously, the international channel remains a drag on growth.

In June, five of 11 PMI components have values above 50; in July, the sum stood at the same figure, just five. In August, the count fell to four, but with three components at a diffusion value of 49 (employment, new export orders, and imports), putting them on the brink of growth.

The virus has impacted economic activity globally. Although it started in China, China now seems to be little affected by the disease. It does have several vaccines in the late stages of trials. But even with this progress, China's economy is still not firing on all cylinders. U.S. tariffs are still in place despite China's phase-one trade deal with the U.S. China's relationship with the U.S. has soured in the wake of the spread of the virus. As a result, trade talks between the U.S. and China had broken off, but they are in the process of being restarted. Still, no country is back to business as usual. And in China, the economy is still struggling as global demand recovers but remains a shadow of its former self.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief