Global| Dec 31 2020

Global| Dec 31 2020China's Manufacturing PMI Crests at Weak PMI Level

Summary

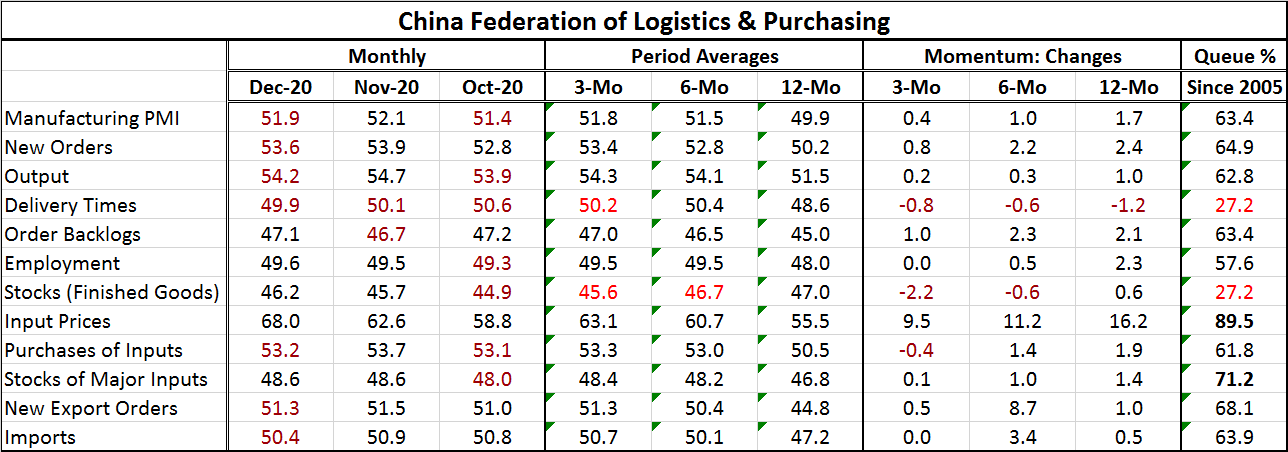

China's manufacturing PMI backtracked slightly in December, falling to 51.9 after reaching 52.1 in November. It is still above its October level. However, at a level below 52, the indicator is signaling a still very modest [...]

China's manufacturing PMI backtracked slightly in December, falling to 51.9 after reaching 52.1 in November. It is still above its October level. However, at a level below 52, the indicator is signaling a still very modest manufacturing sector. But that reading corresponds to a 63rd percentile standing on data back to 2005. That is a testament to how weak China's manufacturing sector has been that an index less than two diffusion points above neutral has a 63rd percentile standing.

China's manufacturing PMI backtracked slightly in December, falling to 51.9 after reaching 52.1 in November. It is still above its October level. However, at a level below 52, the indicator is signaling a still very modest manufacturing sector. But that reading corresponds to a 63rd percentile standing on data back to 2005. That is a testament to how weak China's manufacturing sector has been that an index less than two diffusion points above neutral has a 63rd percentile standing.

Among the eleven components, there were month-to-month declines in six of them. Backing down month-to-month were new orders, output, delivery times, purchase of inputs, new export orders, and imports. China is not stoking up domestic demand as the weakening import gauge tells us. However, in Western economies we see a lot of high values for delivery times indicating some sort of supply chain problems persist. In China, there is no evidence of any supply chain troubles. In fact, the value for delivery times is one of only two components with a queue percentile standing below its historic median.

Output and new order also slipped on the month and export orders slid, acknowledging the weakness in the global economy.

Only two components have readings below their historic medians: delivery times and stocks of finished goods. The two strongest components have standings in their respective seventieth and eightieth percentiles: stocks of major inputs and input prices. Six components have standings in their 60th percentile decile range (60-69).

However, despite all the mediocrity, the broad view is still one of expansion. Over three months, only three of eleven components weakened (delivery times, stocks of finished goods, and purchases of inputs). Employment and imports were flat on that timeline, leaving six components advancing on balance over three months.

Over six months only two components weakened on balance: delivery times and stocks of finished goods.

Over 12 months, only delivery times weakened.

The sequential PMI levels based on averages demonstrate that this same sort of steady progress is apparent in the averaged data as well.

These metrics tell us that since December 2019 and despite a collapse in February as the virus struck China, China's manufacturing is making headway.

China's manufacturing progress is clear and steady and slow, very slow.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief