Global| Dec 31 2019

Global| Dec 31 2019China's Manufacturing Claws Its Way to Meager Gains and the Road Ahead

Summary

All the indicators for China's manufacturing sector remain listless in December. For those of you driven by literalism, China's manufacturing sector has ‘grown' in each of the past two months as its manufacturing PMI stands above 50 [...]

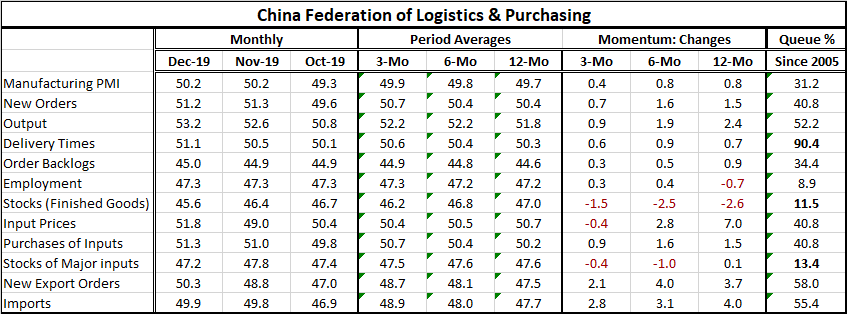

All the indicators for China's manufacturing sector remain listless in December. For those of you driven by literalism, China's manufacturing sector has ‘grown' in each of the past two months as its manufacturing PMI stands above 50 for two months running at 50.2 in each case. It is thin gruel for expansion. I prefer to note that the sector remains flat. Six of eleven of the China PMI component readings are above 50 in December. However, the eleven components' diffusion average is below 50 at 49.4, and only four are above 50 in November (with November's components averaging 49.0). Over three months six months and 12 months, the PMI headline averages below 50 and the eleven components average 48.9 for three months, 48.7 over six months and 48.6 over 12 months. And the percentile standings evaluated since 2005 have standings below 50 for all but four components (the component average standing is 40.6% compared to the headline standing which is 31.2%; for standings the value ‘50' denotes the diffusion index's median value).

All the indicators for China's manufacturing sector remain listless in December. For those of you driven by literalism, China's manufacturing sector has ‘grown' in each of the past two months as its manufacturing PMI stands above 50 for two months running at 50.2 in each case. It is thin gruel for expansion. I prefer to note that the sector remains flat. Six of eleven of the China PMI component readings are above 50 in December. However, the eleven components' diffusion average is below 50 at 49.4, and only four are above 50 in November (with November's components averaging 49.0). Over three months six months and 12 months, the PMI headline averages below 50 and the eleven components average 48.9 for three months, 48.7 over six months and 48.6 over 12 months. And the percentile standings evaluated since 2005 have standings below 50 for all but four components (the component average standing is 40.6% compared to the headline standing which is 31.2%; for standings the value ‘50' denotes the diffusion index's median value).

Despite this clear weakness, over each of these time segments the PMI average is improving and the average change of the eleven components is also a net gain over each period. So while China's manufacturing sector is really giving off flat-lining signals, when it comes to growth there is still some sign of very slow-moving improvement as well.

Still, China's manufacturing sector has been weak for a long time. Since 2013 it has not once been as high at 52.5. Since 2013, the PMI headline has averaged 50.6 with its eleven components averaging 49.5. China has been in a long period of very flat output or with increases of the most marginal sort. I do not consider this a period of output expansion just because the PMI technically averaged above 50. Nor do I see November or December as watersheds of any sort. They are simply more of the same- weak flat listless results.

Anticipation...

There is a great deal of anticipation that the U.S.-China Phase-One deal will lift the pall over international trade, stimulate more trade and raise economic activity in general. Maybe… But that word ‘maybe' is unique. It is the only one I know that equally implies its opposite as well. There is a very thin line of difference if any between ‘maybe' and ‘maybe not.' And that is where we stand with the China-U.S. trade deal that is still not formally signed. Once the deal is inked, very few tariffs go away. The deal does seem to usher in a new phase of cooperation but let's not overdo that; there is no ‘new era of cooperation.' Phase-one is only the limited thing it is because the important Phase-two negotiations have remained so sticky. Trump-Lighthizer are determined not to give in too much until they get more of the real meat they want on the bones of an agreement. So I am much more in the ‘maybe as maybe not' camp that in the ‘maybe as probably-better' camp.

Time will tell. Meanwhile, the U.S. and China have all sort of other conflicts. Hong Kong's protestors have gone on much longer than I ever imagined they would and according to a recent poll have rather widespread support. China has been out trying to extend the olive branch to Taiwan and Macau as if to reassure them after this fiasco in Hong Kong. I can't imagine either of these places have been swayed much by such overtures given what has actually transpired in Hong Kong.

The year ahead

We look to the year-ahead with some hope because of the completion of the U.S.–China phase-one trade deal but in fact I think that is an exaggerated hope. The U.S. will have other trade deals especially negotiations with the EU. Brexit also ought to be wound up but even clarifying what it is may leave the global economy with some drag because of ‘what it will be.'

Got recession?

IHS Markit has dropped its assessment on the probability of recession as PMI gauges have stopped falling and bottomed out (for now?), but they are still at very weak readings. There is little source of real stimulus and a lot of emphasis is being placed on the role of removing uncertainty by completing trade deals although in truth a lot of uncertainty is not going to be removed.

Hard habits to break

Odd things continue such as the report at the end of the year of dollar reserves being so high. This indicates buying and holding of dollars (which acts to make the dollar stronger than it would be under free market conditions). Not only does that impede the U.S. ability to export but it goes against what appears to be stated desires by some to use the dollar less. The U.S. has been so effective in imposing its sanctions and has been so willing to use its power of sanctions so broadly that a number of European nations have been looking to an alternative to the current payments systems that clear so much through New York subjecting many what would otherwise be unrelated transactions to U.S. jurisdiction. Will 2020 be the year when a clear alternative to this payments system emerges? Europe has been taking about it. And separately so have Russia China and others with more conflict with the U.S.

The challenge ahead

Will the Western nations and countries of the G7, G10 and G20 come to see that they do have a lot more in common and need to truly work together and to harmonize fair rules or will they see the U.S. action to have its own interests and to have others stand more on their own two feet as hostile to the post war order of things? It is not just trade and technology and global warming that are defining a new world order. The last decade was a decade of enormous shifting and development. The winners of the last decade want to keep the same rules in effect; the losers want to re-set the rules. Meanwhile, there are climate issues that beg to be addressed in a world where externalities matter and yet they are not addressed formally. And dealing with climate also affects competitiveness which is another of those issues that has been put on the table at the end of decade. Can you have free trade, fair competition and still restrict environmental damage? This will be the decade that tests that set of ideas.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief