Global| Jun 29 2007

Global| Jun 29 2007Chicago PMI Off at 60.32 from 61.7

Summary

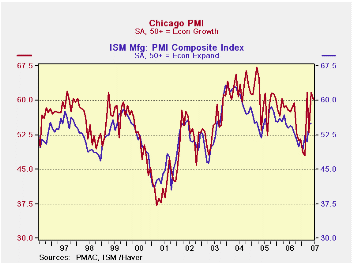

The Chicago PMI is a good guide to the ISM but not infallible; often its strength overshoots the ISM. Still any reasonable reading of the historic relationship leaves you positive on the outlook for the ISM in June. The Chicago index [...]

The Chicago PMI is a good guide to the ISM but not infallible; often its strength overshoots the ISM. Still any reasonable reading of the historic relationship leaves you positive on the outlook for the ISM in June.

The Chicago index keeps to stronger readings than the ISM in general. That explains why the strong Chicago readings are not so elevated when displayed as percentile standings within their historic ranges. The 60.2 headline reading stands in the top 25% of the measure’s range since 1996. It is 6% above its median reading. Indeed, if the ISM for this period is also some 6% above its median it will post a value of 56.3 this month, an increase of more than one point on the month.

Most Chicago survey components are in the upper 25 percent (or so) of their range of values since 1996. Deliveries are an exception as they have been for some time and as they are in many other regional MFG surveys. I take this as a sign that there is still a lot of slack in MFG; it’s a sign that orders can be filled quickly when they rise. Order back logs are only in the top third of their range and that component dropped three points this month in Chicago. Order backlogs and jobs are well correlated so it is not surprising to see the Chicago job component fell very sharply to 52.7 from 57.3, but it still stands well above its April reading of 50.5. Employment trends have become volatile but this month is the first pull-back in a job recovery in the Chicago region that dates back to a low reading in January of this year. The Cincinnati MFG report that was also released today shows an improvement from 27 previously to 30 in June.

On balance, the Chicago report is more upbeat than expected and it points to a strong ISM reading for June. It sides more with the strong reports we have seen in NY and Philadelphia and is NOT part of the weak reading reports such as we have seen in Dallas and Kansas City. The final column in the table below applies ISM-type weights to the Chicago components to recast the headline. On that basis the Chicago index is even stronger at least in its historic range. That tells us that the Chicago components are strong as a group although m/m they fell by a bit more that the ‘headline’ barometer.

| Since 1996 | Index | Orders | Production | Delivery | Inventories | Prices Paid | Employment | Backlogs | Weight |

| Date | 1994 To Date | ||||||||

| Jun.07 | 60.2 | 65.7 | 66.5 | 52.1 | 55.9 | 68.2 | 52.7 | 50.8 | 60.2 |

| May.07 | 61.7 | 71.1 | 69.8 | 45.3 | 52.6 | 70.2 | 57.3 | 53.0 | 62.4 |

| Apr.07 | 52.9 | 56.5 | 62.2 | 43.4 | 43.2 | 64.9 | 50.5 | 48.4 | 53.9 |

| Std Dev | 6.6 | 8.3 | 7.9 | 5.5 | 6.4 | 12.1 | 6.7 | 6.6 | 6.4 |

| Median | 56.6 | 59.6 | 60.8 | 51.7 | 48.4 | 61.2 | 50.6 | 49.4 | 56.3 |

| Mean | 55.0 | 57.9 | 59.1 | 52.2 | 48.3 | 61.6 | 48.6 | 48.7 | 54.4 |

| SD%MN | 12.0 | 14.3 | 13.4 | 10.5 | 13.3 | 19.7 | 13.7 | 13.6 | 11.8 |

| Max | 67.2 | 74.9 | 74.9 | 67.6 | 66.7 | 87.8 | 63.1 | 60.8 | 65.9 |

| Min | 37.2 | 36.5 | 37.8 | 41.0 | 33.3 | 34.8 | 23.6 | 30.2 | 36.6 |

| % MEDIAN | 106% | 110% | 109% | 101% | 116% | 111% | 104% | 103% | 107% |

| Percent-Range | 76.7% | 76.0% | 77.4% | 41.7% | 67.7% | 63.0% | 73.7% | 67.3% | 80.4% |

| %of2stdev | 69.7% | 73.5% | 73.3% | 49.4% | 79.5% | 63.6% | 65.3% | 58.0% | 72.3% |

| % Average | 109% | 113% | 113% | 100% | 116% | 111% | 108% | 104% | 111% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief